- Chile: BCCh cuts policy rate by 25bps to 5.75% with a very cautious bias

- Colombia: BanRep Survey shows lower inflation expectations and steady 50bps June rate cut call; Economic activity exceeded expectations in April due to volatile components

CHILE: BCCH CUTS POLICY RATE BY 25BPS TO 5.75% WITH A VERY CAUTIOUS BIAS

- Rate cuts would not be resumed until October or December, and highly conditional on inflation data.

Yesterday, the Central Bank of Chile (BCCh) cut its policy rate by 25bps, to 5.75%. In our view, the idiosyncratic supply shocks in opposite directions and the Fed's new normalization scenario made it advisable to anticipate a 25bps cut at this meeting, with subsequent tactical pauses that allow evaluating the effects of the second round of increases in electricity rates, the exchange rate pass-through of the recent appreciation of the Chilean peso and the new scenario for Fed cuts. We do not expect cuts before the October meeting, where they would not be guaranteed.

We consider that the BCCh evaluated three options for this meeting: keep the rate at 6%, cut 25 bps, or cut 50 bps—but ruling out the 50-bps cut given the latest inflation information. Likewise, we consider that they ruled out maintaining the rate because it would have surprised expectations and would have given too much importance to a supply shock whose intensity in the second-round effects is still uncertain. In fact, reaffirming our view of evaluating these policy options, one of the Board members voted in favor of a 50bps cut, probably arguing for the validity of the base case of the March IPoM (monetary policy report, with new one out today at 9ET).

The external scenario is evaluated with high degrees of uncertainty and mixed and incipient signs of inflationary convergence. The Board highlights the upward adjustment in the Federal Funds Rate outlook, which went from three cuts for this year to just one. With this, the policy rate in the US would be in a range between 5.00% and 5.25% by December 2024, which will be part of the baseline scenario of the June IPoM. It should be remembered that this was part of the risks on the rate corridor presented in the March IPoM and that it was represented through an intermediate scenario, at the upper part of the corridor.

The bias of the statement seems very cautious and more aggressive/hawkish than expected by markets. In our view, it seems appropriate to see a policy rate between 5.25% and 5.50% in December 2024, and we also expect an upward adjustment in the annual inflation projection for 2024 and 2025. The Central Bank will expect to see the inflationary effects of increases in electricity fares and the exchange rate pass-through before continuing to cut the rate, especially after the rate is at a level much more appropriate for the cyclical position of the economy.

—Aníbal Alarcón

COLOMBIA: BANREP SURVEY SHOWS LOWER INFLATION EXPECTATIONS AND STEADY 50BPS JUNE RATE CUT CALL

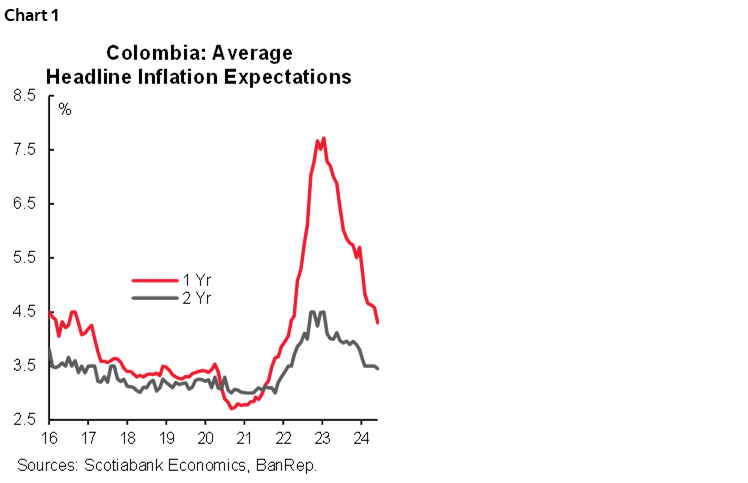

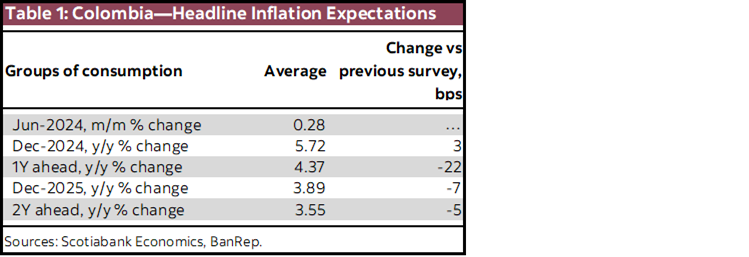

The Central Bank (BanRep) released the economist’s expectation survey for June. Inflation expectations in the medium-term decreased, which is positive news for the central bank. For Dec-2024 and Dec-2025, expectations are at 5.72% and 3.89%, respectively. The inflation expectation for the one-year mark is at 4.37%, decreasing by 22bps and, while the two-year horizon (June 2026) decreased by 5bps to 3.55%. Regarding short-term inflation expectations for June, the expectation is at 0.28% m/m, which could take annual inflation to 7.14% from the current 7.16%. Scotiabank Colpatria’s projection is 0.32% m/m, and 7.18% y/y (chart 1). In June, we expect to see some pressures in leisure-related prices, while food inflation is expected to be slightly below the previous month’s inflation. Rent fees and utility fees will increase moderately. We don’t expect any extraordinary movement in prices in June. However, we have to be vigilant if the government decides to increase toll fees in the coming weeks.

For the monetary policy rate, market consensus projects a 50bps cut at the June 28th meeting, which is the same expectation that Scotiabank Colpatria has. For the year-end, economist consensus expectation stayed at 8.50%, while Scotiabank Colpatria’s expectation remains at 8.25%. The terminal rate could be estimated at 5.50% by Scotiabank Colpatria, which is the same expectation as the economist consensus. However, according to market consensus, the terminal rate will be achieved in March-2026, while Scotiabank Colpatria Economics expects this convergence to take place in mid-2025.

It is worth noting that BanRep remains cautious, however in the last couple of months some macro data has been supportive of continuing the easing cycle. Inflation was broadly aligned with expectations, while medium-term inflation expectations continued decreasing, economic activity data is still showing weakness, and the current account deficit reflects a significant weak picture for domestic demand and investments. Additionally, the fiscal perspectives are apparently clear and the sentiment on international markets has improved. Our base case is for a 50bps rate cut in June, however, we think that if the context remains supportive for rate cuts, the central bank will have space to speed up the easing cycle cutting by 75bps in July and for the rest of meetings in the year.

Key points from the survey:

- Short-term inflation expectations. For June, the consensus is 0.28% m/m, which implies an annual inflation rate of 7.14% y/y (down from 7.16% in May). The maximum expectation is 0.40%, and the minimum is 0.08%. Scotiabank Economics forecast is 0.32% m/m and 7.18% y/y. It is worth noting that since June, BanRep’s survey has asked for further details about inflation expectations, and this month we identified the economists’ consensus has a moderate expectation for food prices, which stands at 0.17% m/m, while regulated prices are expected to increase by 0.36% m/m, a more moderate variation versus the previous month.

- Medium-term inflation expectations improved. Inflation expectations for December 2024 increased by 3bps to 5.72% y/y (table 1). However, the headline inflation expectations for the one-year horizon were 4.37% y/y (-22bps). The two-year inflation expectation decreased by 5bps to 3.55% y/y.

- Policy rate. The median expectation points to a 50bps rate cut at both June and July meetings, while the rest of the meetings during 2024 point to a 75bps rate cut in each one (September, October, and December). With previous expectations, economists’ consensus points to an 8.50% level for Dec-2024 and 5.75% for Dec-2025. Scotiabank Colpatria’s projection is similar, since for Dec-2024 we expect 8.25% for Dec-2024 and 5.50% for Dec-2025 (chart 2).

- FX. The projections for the USDCOP exchange rate for the end of 2024 averaged 4051 pesos (49 pesos above previous survey). For December 2025, respondents, on average, expect the exchange rate at USDCOP 4045 pesos (previous 4036 pesos).

—Jackeline Piraján

ECONOMIC ACTIVITY EXCEEDED EXPECTATIONS IN APRIL DUE TO VOLATILE COMPONENTS

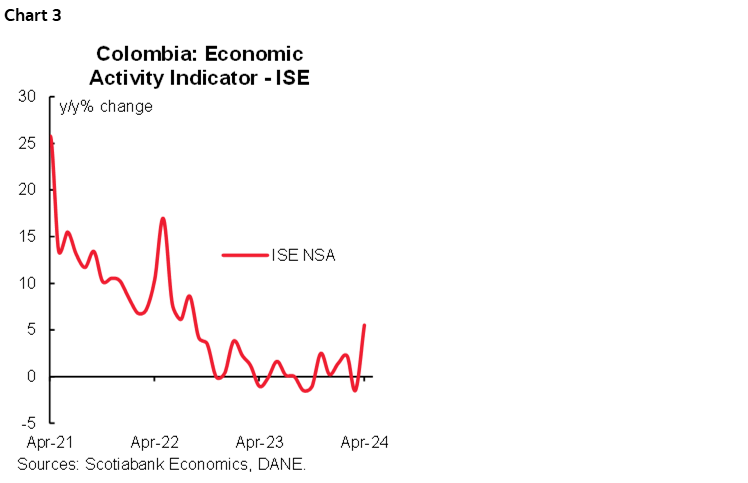

On Tuesday, June 18th, DANE published April’s Economic Activity Indicator (ISE) data. The indicator showed an annual growth of 5.5%, far exceeding the market expectation (2.5% y/y). The results showed that eight of the nine activities had positive annual variations, with the agricultural sector and public activities adding the most to the general result. In inter-monthly terms, the result interrupted the negative trend of the last two months after standing at 2.0% m/m (chart 3), showing the most significant growth in public activities (7.4% m/m).

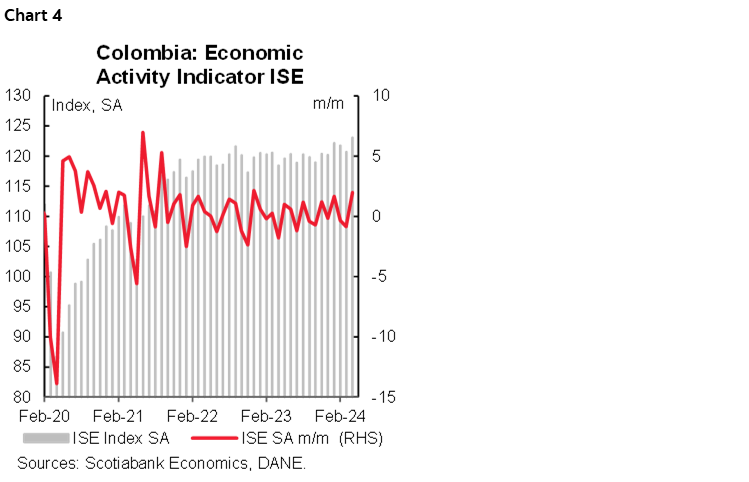

Economic activity showed the greatest expansion since August 2022 (chart 4), with the primary sector showing the best performance with a growth of 10.2% y/y, the largest expansion of the year; however, the result may be due to a favourable statistical base effect due to reduced primary activity in 2023. The category that groups activities related to the public sector and entertainment was the second with the best performance, rebounding with 13% y/y. This positive behaviour has been maintained throughout the year.

Economic activity seems to be gaining momentum, although it is still too early to say that the positive trend can be maintained throughout the year. Once again, the better-than-expected performance is explained mainly by agriculture and public activities, sectors that have brought volatility instead of a sustainable trend. Labour-intensive sectors such as industry and construction showed better performance, breaking the negative trend they had kept for over a year. Meanwhile, consumption remains repressed, reflected in commerce activity that is not gaining strength.

The data does not alter our expectation that the Banco de la República will implement a 50bps interest rate cut at its next meeting on June 28th. This anticipation is further supported by the data, which could provide some reassurance to continue with the cautious stance, focusing the message on the fight against inflation.

Key Highlights:

- The agricultural sector surprised with a growth of 10.2% y/y. In the first two months of the year, the primary sector showed a positive dynamic, interrupted in March. However, in April, it regained momentum, even though no major contribution was anticipated given an El Niño phenomenon that was expected to affect the sector’s behaviour.

- Secondary activities would show a recovery in manufacturing production. The result confirmed the industry’s good dynamics, with growth in secondary activities of 2.8% y/y and 1.7% m/m.

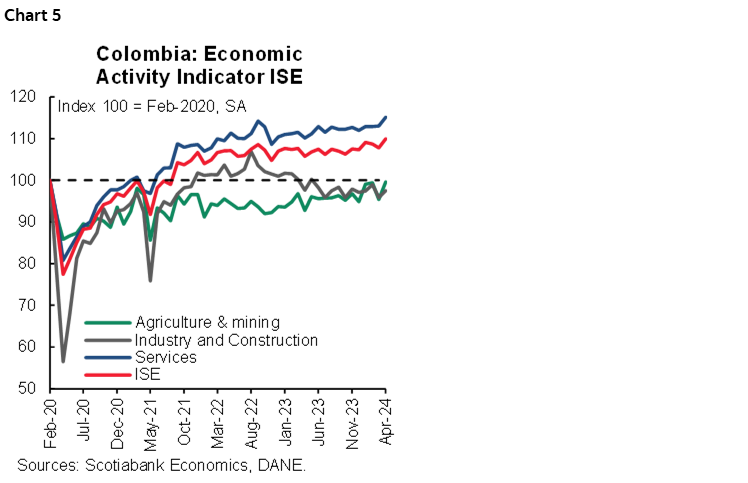

- Tertiary activities maintain a positive dynamic. In April, the indicator for this item grew 5.1% y/y, posting an expansion not seen since September 2023. The increased operation in the energy sector, the significant growth in activities related to the public sector, the positive growth in financial activities, and the slight growth in the commerce sector all contribute to a confident outlook on the economy’s performance (chart 5).

—Jackeline Piraján & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.