- Chile: Unemployment rate fell to 8.5% in the quarter ending in December

- Colombia: Monetary Policy Preview—the debate about the speed of the easing cycle begins

- Mexico: GDP slowed in Q4-23 according to flash estimates, averaging a 3.1% advance for the year

- Peru: Inflation could return to target range earlier than expected

Equity futures are in the red after some disappointing tech giant earnings yesterday, with the negative mood spreading to FX markets where the USD is broadly stronger ahead of key US data (ADP, ECI) and the US Treasury’s quarterly refunding announcement, followed by the Fed’s policy decision at 14ET. Overnight, Australian Q4 CPI missed expectations, Chinese official PMIs were roughly on-consensus (still weak), and the BoJ’s January meeting summary firmed up Q2 rate hike expectations.

Global rates rallied at the European open on a French CPI miss, adding to UST strength yesterday evening. EGBs are bull flattening while USTs are bull steepening, but off best levels after German state-level inflation strength offset some of the earlier gains. Oil is down about 1%, while copper is flat and iron ore is off 2.5% on negative China sentiment. Despite the risk-off mood, the MXN is up 0.1% as the only key major up vs the USD today, erasing its losses (and then some) on yesterday’s Q4 GDP miss (see below). Month-end flows may see some erratic behaviour in global markets today.

BanRep (13ET), the BCCh (16ET), and the BCB (16.30ET) all have policy announcements today (see Latam Weekly). Briefly, we expect respective cuts of 50bps, 100bps, and 50bps, in line with the median submission to Bloomberg. For the BCB, a 50bps cut is certain and guidance will likely continue to point to more 50bps cuts ahead. Note, however, that about two-fifths of those polled anticipate only a 25bps cut in Colombia and our economists believe there is a slight chance that BCCh considers a 125bps reduction. The CLP’s 5.5%+ depreciation in the year-to-date is an important external risk that officials will probably prefer to avoid worsening. A collection of Chilean data out at 7ET (December retail sales, industrial production, commercial activity) may influence the bank’s decision or guidance; economic activity figures are out tomorrow.

—Juan Manuel Herrera

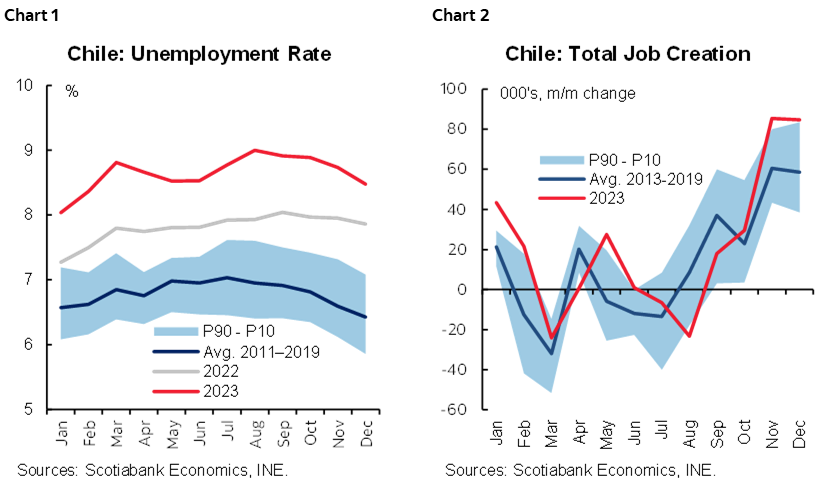

CHILE: UNEMPLOYMENT RATE FELL TO 8.5% IN THE QUARTER ENDING IN DECEMBER

- Strong job creation, although with sectors still lagging behind.

On Tuesday, January 30th, the statistical agency (INE) published the unemployment rate for the quarter ending in December, which fell to 8.5% (chart 1), surprising the market positively by coming in below consensus expectations (8.7%), although closer to our forecast of 8.6%. The fall in the unemployment rate is explained by the creation of 85k jobs (chart 2), which exceeded the growth of the labour force (+64k). In seasonally adjusted terms, the figures are somewhat more moderate, with a slight drop in the unemployment rate from 9.0% to 8.9% thanks to the creation of only 21k jobs.

Total job creation was strong for the second consecutive quarter. Once again 85k jobs were created, highlighting the creation of private salaried employment (+82k) and new jobs in sectors such as commerce (+39k) and healthcare activities (+17k). Unlike the previous quarter, where we highlighted the lights and shadows of the positive employment record, December saw strong formal job creation (+55k), being the highest since March 2022.

At the sector level, commerce showed a performance above that observed seasonally. The sector contributed with the creation of 39k jobs, most of them salaried jobs in the private sector, which partially offset the negative performance of the construction sector and industry in December, both of which showed job losses. Although agriculture also stood out in terms of job creation, this was not very different from the historical average of job creation for the month. On the negative side, public administration was the sector that destroyed the most jobs, which is in line with zero public salaried job creation.

Our assessment of this record is positive, although we view it with caution. Administrative records through October (pension funds contributors) continue to show year-on-year employment declines, while some economic sectors continue to lag in their employment level, mainly construction. While records at the margin (November and December) anticipate strong job creation for the rolling quarter ended January, our view is that the labour market recovery is still incipient, and its sustainable recovery will have to come hand in hand with a better investment performance in 2024.

—Aníbal Alarcón

COLOMBIA: MONETARY POLICY PREVIEW—THE DEBATE ABOUT THE SPEED OF THE EASING CYCLE BEGINS

Today, BanRep will hold its first monetary policy meeting of 2024. In December, the central bank decided to reduce the monetary policy rate by 25bps to 13% in a split vote, with five members voting for the cut and two voting for stability. The majority expressed concerns about the significant economic deceleration recorded in Q3-23, as by this time, the economy contracted 0.3% y/y. Additionally, according to Governor Villar’s assessment, the positive output gap vanished by Q3-23. In January, the board will have enough arguments, especially on inflation, to speed up the easing cycle; economist surveys, the market, and Scotiabank Colpatria expect a 50bps rate cut to 12.50%. However, similar to the one observed in December, the decision could be in a split vote.

Inflation in December 2023 stood at 9.28%, well below BanRep’s staff projection of 9.8%; on the other side, the minimum wage increase was set at 12%; both indicators contribute to having lower indexation effects in 2024 compared with the observation in 2023 when prices were set given past inflation of 13.12% and a minimum wage increase of 16%. Finally, economic activity data continues to show that Colombia is transitioning through the bottom of the economic cycle. All of the above elements, support an expectation for a rate cut.

The speed will be the main question in January’s debate. In that regard, we think the board will turn the conversation towards the real monetary policy rate. Let’s define this real monetary policy rate as an average between the nominal monetary policy rate deflated by current inflation (ex-post real rate) and 1Y-inflation-expectations (ex-ante real rate). The current real rate is 3.4% ex-post and 7.1% ex-ante (average 5.3%), vs a neutral level around 2.4% (according to BanRep’s estimation). As there is a consensus that indexation effects and high statistical base effects will allow annual inflation to go down significantly in the first quarter of the year, the nominal rate should follow the inflation decrease to avoid significant spikes in the real rate in a context in which the economy has a neutral output gap. However, there are still several uncertainties around regulated prices and the “El Niño” phenomenon effects in prices, which make a higher rate cut less probable in this stage.

According to the former arguments, a rate cut of 50bps looks like the more feasible scenario. For this meeting, the central bank’s staff will provide a new quarterly monetary policy report, which will update the risk assessment around macro projections and could help the board decide to speed up the easing cycle. Despite the uncertainty, the impact of the “El Niño” weather phenomenon is still high, we think it won’t prevent the central bank from continuing the easing cycle at the beginning of the year as statistical base effects from indexation weigh more. BanRep’s staff assessment of the timing of inflation deceleration will also be key to affirming our expectation of a potential 100bps rate cut in March. Scotiabank Colpatria projects the monetary policy rate will close at 7% in 2024, while for now, economist consensus is between 100 and 150bps higher.

Other key points for today’s decision:

- The Fed’s decision will be around 30 minutes after BanRep’s meeting. However, we think that financial conditions have improved, and BanRep can implement a cut without suffering significant adverse shocks in financial variables such as the exchange rate.

- In February, BanRep won’t decide on monetary policy. That said, January’s meeting move could compensate somewhat for the expected waiting time the board will take in February.

- Staff projections: keep an eye on output gap estimations and the expected inflation deceleration in H1-2024. Both indicators could confirm or discard whether the central bank’s staff favours (or not) speeding up the easing cycle.

- Division should prevail. We see a low chance of a board member voting for stability; that said, speed will be the key point of debate.

—Sergio Olarte & Jackeline Piraján

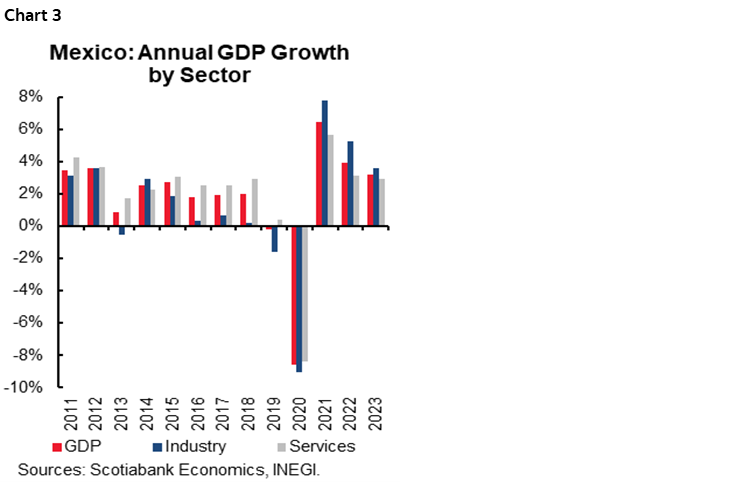

MEXICO: GDP SLOWED IN Q4-23 ACCORDING TO FLASH ESTIMATES, AVERAGING A 3.1% ADVANCE FOR THE YEAR

The GDP flash estimate for 2023 Q4 resulted in a quarterly slowdown to 0.1% q/q sa, from 1.1% previously and 0.4% consensus. By sectors, services cooled to 0.1% (vs. 0.9% previously), while industry remained unchanged (0.0%, vs. 1.3% previously) and primary activities fell -1.1% (2.6% previously). On an annual basis, GDP slowed to 2.4%, below the 3.4% consensus and 3.3% previously. By sectors, industry decelerated to 3.1% y/y (4.3% previously), services fell to 2.1% (2.7% previously), and the primary sector held a lower pace, in line with the previous sectors, at 2.1% (5.7% previously) (chart 3). With these data, GDP averaged a 3.1% growth in 2023, below the 3.4% consensus in the last Banxico Survey, although well above the 1.0% expected by analysts at the beginning of that same year.

The GDP monthly proxy (IGAE) for November, published the previous week, detailed that the slower progress in the economy came from a monthly decline in manufacturing, in line with a slowdown in manufacturing exports, except for automotive exports. Additionally, construction shows signs of deceleration, after observing quite vigorous increases since the end of 2022, mainly owing to public sector projects. On the services side, monthly indicators point to a moderation in retail trade at the end of the year, in contrast to a greater annual increase in wholesale trade; both on track to average an annual advance of more than 4.0% by 2023. Considering this flash estimate of GDP, this would imply an annual advance close to 0.5% in December 2023.

Despite a slower-than-expected pace, growth expectations for next year remain strong. We believe that the dynamism of the following year will be led by domestic demand. On the one hand, the increase in public spending will give a strong boost to economic activity during the first half of the year. Also, consumption could remain with a strong pace thanks to a robust labour market (with unemployment rates below historical averages) and the advances in real wages, as well as the positive trend in remittances. On the other hand, we consider that investment could maintain a favourable, although moderate, pace, after the increases observed thanks to the boom in construction. However, with a positive outlook thanks to expectations around nearshoring, although facing a high degree of uncertainty, especially derived from the political and electoral environment in Mexico and in the United States.

—Brian Pérez & Miguel Saldaña

PERU: INFLATION COULD RETURN TO THE TARGET RANGE EARLIER THAN EXPECTED

We expect January inflation to be close to -0.10% m/m in our latest update, below the average of the last 20 years (+0.23%), continuing the downtrend in inflation, from 3.2% y/y to 2.9% y/y, which reflects the possibility of returning to the target range (between 1% and 3%) sooner than anticipated by the BCRP. Core inflation would remain within the target range, going from 2.9% y/y to 2.8% y/y. Although inflation under control could lead us to think about a scenario of more rapid declines in interest rates, we believe that the BCRP will maintain a cautious attitude, considering that inflation will continue to ramp up near the upper limit of the target range in February and March, and because we see it less inclined to expand liquidity significantly, necessary to increase the speed of rate decline.

January inflation would reflect the more favourable weather conditions, given the weak signals of El Niño. It also reflects low oil prices during the first half of January. However, since the second half of January, greater effects have been observed from the conflict in the Middle East on oil, freight, and container prices, which would put upward pressure on February inflation. Our forecast of 2.4% for the year-end considers a weak El Niño scenario and an average oil price of US$80 per barrel.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.