- Peru: Infrastructure investment to grow for third consecutive year in 2024

It’s a deeply uneventful start to the week with no top tier data hitting the screens until Wednesday’s global PMIs and only the BoJ’s decision overnight Tuesday in the interim. In the absence of triggers, markets are showing only slight directional biases. It’s a busy G10 week ahead, with the BoC and ECB also deciding on policy and the US releasing GDP and PCE data. In Latam, we’ll have the first inflation data of the year in Brazil and Mexico, both for the first half of January, as well as Mexican economic activity.

The risk mood looks in decent shape as US equity futures tick higher and European bourses post solid gains—in contrast to steadily beaten China/HK equities. USTs are twist flattening, continuing the post-Europe trend on Friday; EGBs and gilts are in better shape, catching up to late-week US moves and catching a bid in local hours that is also helping US debt. The USD is mixed in narrow ranges; the MXN is flat, holding in the low-17s where its Friday rally left it. Crude oil is little changed, while iron ore and copper suffer losses in tandem with the weak China backdrop.

The Latam session presents Colombian imports data and the release of Mexico’s Citibanamex survey of economists. Colombian data could give us a read of internal demand dynamics that remain weak, while the Citi survey may only be worthwhile if the recent reassessment of Fed cut expectations has influenced Banxico projections; in the latest results, the median expected a year-end Banxico rate of 9.25%.

On Friday, the BCRP stated that Peru’s fiscal deficit totaled 2.8% of GDP in 2023. This represents a 0.4ppts overshoot of the 2.4% ceiling set for the year (though slightly better than we expected at the start of the year). The current year has a 2.0% target that also looks somewhat at risk. In related news, Prime Minister Otarola said late last night that the government does not have the funds to assist Petroperu, which had requested USD2bn in support to accelerate its financial recovery. The head of the Council of Minister noted that they are prioritizing El Niño preparations so no funds are available for the oil company, but said that they will reschedule the company’s debts to the MinFin with a reorganization of Petroperu’s directors in about three to four weeks.

—Juan Manuel Herrera

PERU: INFRASTRUCTURE INVESTMENT TO GROW FOR THIRD CONSECUTIVE YEAR IN 2024

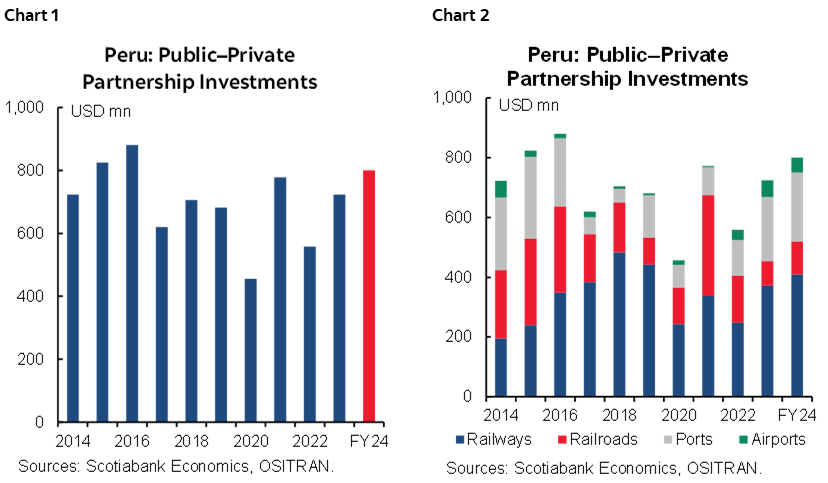

Investment in transportation projects in Peru grew by 33% in 2023, according to Peru’s Transportation Infrastructure Supervisor, Ositran. This level of growth exceeded our expectations. Investment in transportation was US$723 million in 2023, versus US$558 million in 2022, albeit lower than the amount invested in 2021 (see charts 1 and 2).

Investment growth in 2023 was led by the Lima Metro Line 2 project, at US$372 million, or 50% more than in 2022. This was the highest annual investment since the project began. Metro Line 2 began operating five stations of stage 1A and is currently making progress with different stations of stage 1B. Two tunnel boring machines are operating, which will increase the speed of the project’s development. At the end of 2023, the project recorded an advance of 52%. The total committed investment in the project is US$5 billion.

Furthermore, investment in ports amounted to US$214 million, which was 80% higher than in 2022. The increase in port investment included the expansion of the New South Zone Container Terminal (South Pier) with US$154 million, and the expansion of the North Multipurpose Terminal with US$27 million (North Pier), both in Callao.

For 2024, we expect investment in tendered transportation infrastructure to be approximately US$800 million, led by Lima Metro Line 2 which should represent close to half of this amount. Other projects for 2024 include the expansions of the South Pier project—work started in mid-2023- and North Pier—they will start stage 3A during 2024. Finally, the expansion of the Jorge Chavez International Airport in Lima will also help boost investment. The project is to build a second passenger terminal, which would be completed in 2025.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.