- Colombia: S&P lowered Colombia’s credit rating outlook from ‘stable’ to ‘negative’, highlighting a need for better quality economic growth; Economic activity rebounded in November with growth in y/y and m/m terms

S&P LOWERED COLOMBIA’S CREDIT RATING OUTLOOK FROM ‘STABLE’ TO ‘NEGATIVE’ HIGHLIGHTING A NEED FOR BETTER QUALITY ECONOMIC GROWTH

S&P maintained Colombia’s BB+ rating for Foreign Currency Debt; however, it reduced the country’s outlook to ‘negative’ from ‘stable’. The main concern for S&P is that the slowdown in economic activity reflects not only a deceleration in household demand but also weak private investment activity which poses a risk for medium-term GDP growth perspectives.

Key points about S&P decision:

- S&P’s action was unexpected and, in our opinion, could bring some volatility in domestic markets. However, we don’t expect a negative episode comparable to the one observed in 2021 when Colombia lost the investment grade by two credit agencies. In fact, according to our models, the USDCOP already involves a risk premium of around 250 pesos due to the fact that Colombia is no longer an investment-grade country. That said, we don’t expect the currency to start a new depreciation path, but it could probably fluctuate around 4000 pesos in the medium-term. On the FI side, we think that the main driver for rates continues to be the expected easing cycle from the central bank.

- S&P mentions that “the negative outlook indicates that (they) could lower the rating over the next two years if economic growth is below expectations, indicating less economic resilience and contribution to fiscal slippage or higher vulnerabilities.” In that sense, we think today’s action is a warning signal from S&P to the government, signaling that Colombia needs policies that contribute to pursuing higher investment activity, which we call growth quality. Ultimately, a better growth quality will contribute to achieving stable and higher fiscal income.

- It is worth mentioning that up to Q3-2023, investment activity in Colombia was 15% below pre-pandemic levels, and it was especially reflected in construction-related activities. For 2024, a context of lower interest rates, lower inflation, and new regional administrations could contribute to generating a better environment for investments. On the other side, the government must implement the budget in investment programs to contribute to better growth quality.

- On the positive side, S&P continued highlighting Colombia’s robust institutions—a stable democracy, political institutions that preserve predictable economic policies, and an independent central bank. In our opinion, those characteristics are valuable assets that confirm the tradition of Colombia of paying its debt.

Current Credit Ratings Profile:

- Moody’s foreign issuer rating: Baa2 (investment grade), outlook stable

- Fitch long-term foreign currency debt rating: BB+, one level below investment grade, outlook stable.

Overall, we think today’s S&P reduction in the outlook is calling attention to pursue better policies to increase investment in Colombia’s economy. At Scotiabank Economics, we think that economic conditions in 2024 will improve, inflation is expected to decelerate, interest rates could go down and despite the economic recovery takes time, we think that improved conditions could permit the start of a healthier economic cycle. Either way, it is critical for the government to implement the investment budget and promote a suitable environment for private investments. At Scotiabank Colpatria, we projected a 1.1% GDP growth in 2023 and a 1.8% expansion in 2024.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

COLOMBIA: ECONOMIC ACTIVITY REBOUNDED IN NOVEMBER WITH GROWTH IN Y/Y AND M/M TERMS

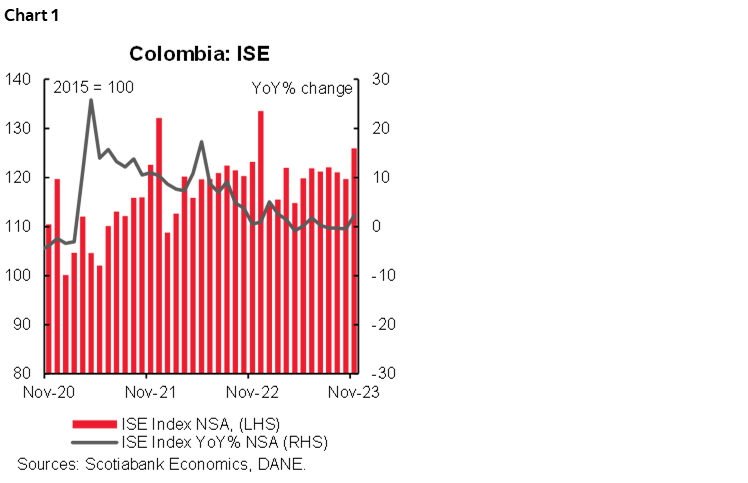

On Thursday, January 18th, DANE published the latest data for the economic activity indicator (ISE) for November 2023. The indicator showed a rebound of 2.3% y/y (chart 1), interrupting three months in a row of contraction. This result was in line with our expectations (2.4% y/y). The rebound also was observed in the monthly variation, as seasonally adjusted growth was 0.9% m/m, after -1.1% m/m in the previous month.

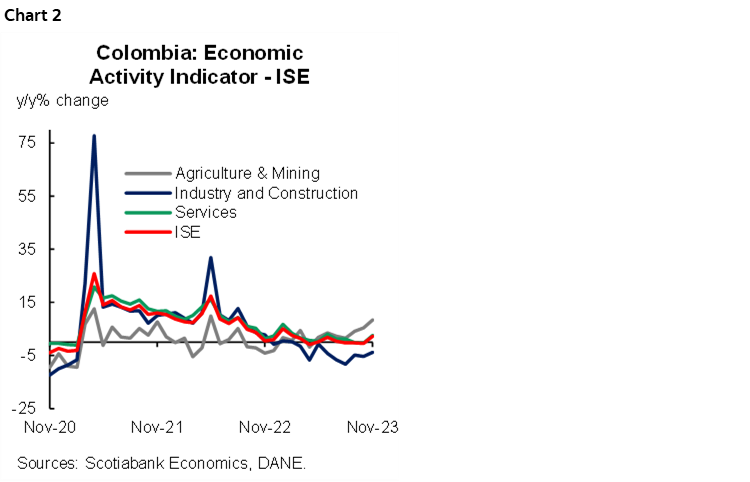

On a yearly basis, November showed a positive balance for primary activities, which grew by 8.4% y/y, followed by tertiary activities (services), which expanded by 2.6% y/y in November. Within the tertiary sector, public administration, arts and entertainment together with financial services, insurance, and public utilities drove growth in this sector. Nevertheless, trade, transport, and accommodation were the sub-sectors that registered a negative variation, although with a slight improvement compared to the record for the last 6 months.

In seasonally adjusted terms, all three sectors registered an improvement versus October’s results, with the primary sector registering the highest growth in November at 2.5% m/m, followed by the secondary and tertiary sectors, which posted monthly expansions of 1.6% m/m and 0% m/m, respectively, in the penultimate month of 2023.

The Colombian economy is expected to expand by 1.1% in the whole of 2023. However, November’s results are pointing out that the economic cycle is probably bottoming. In Scotiabank Colpatria, we project the economic growth will improve in Q4-2023 and will continue recovering at a moderate pace during H1-2024. Either way, we think domestic demand has adjusted to more sustainable levels, but investment is still a concern. During 2024, it will be relevant to observe if the economy responds to the lower exchange rate, lower inflation, and the expectation of potentially lower interest rates. Construction and manufacturing are sectors to keep an eye on.

The slowdown in economic activity in 2023 has allowed inflation to decelerate rapidly to 9.28% by the end of 2023. This has allowed BanRep to initiate the easing cycle with a 25 bps cut to 13% in December. With inflation expected to decelerate further to 4.4%, BanRep is also expected to accelerate the easing cycle, reaching 7% in December of this year. Current data also support the discussion of a possible 50 bps rate cut to 12.50% at the January BanRep meeting, which is our baseline scenario.

Highlights:

- Primary activities (agriculture and mining) grew at an annual rate of 8.4% y/y (chart 2) and 2.5% m/m seasonally adjusted. In agriculture, the moderation in producer prices continues to increase food production, partly due to the appreciation of the exchange rate and its relationship with the level and statistical base. In the mining sector, oil and coal production has contributed to the improved performance of the sector.

- Secondary activities (manufacturing and construction) ended nine consecutive months in negative territory, registering a contraction of 3.9% y/y; however, this is the smallest decline recorded for this indicator in the last 6 months. In seasonally adjusted terms, there was a slight rebound of 1.6% m/m in November from the -2.4% m/m recorded in October.

- According to data published by DANE on Wednesday, January 17th, real manufacturing production contracted by 6.4% y/y in November 2023, completing nine consecutive months of annual contraction. Nevertheless, there was a slight rebound at the margin from the previous month, as the manufacturing sector rebounded to -0.2% m/m in November from -0.9% m/m in October. This decline, combined with the low dynamism of the construction sector, has led to a slowdown in secondary activities on an annual basis.

- As for the tertiary sector (which includes activities related to trade and services), an annual growth of 2.6% was recorded in November. This result was due to growth in public administration, arts, and entertainment (+6.9% y/y), financial and insurance services (+4.2% y/y), and public services (+3.5% y/y). On the other hand, trade, transport, and accommodation were the subsector that registered a negative variation in November, contracting by 2.3% y/y, although with a slight improvement compared to the record of the last 6 months. In seasonally adjusted terms, an annual variation of 0% was recorded, with the subsectors of public administration, education and entertainment (-0.5% m/m), professional activities (-0.2% m/m) and financial and insurance services (+0.8% m/m) driving the tertiary sector in comparison with October, offsetting the decline in the subsectors of trade, transport and accommodation (-2.6% m/m) and information and communication (-0.4% m/m).

—Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.