- Colombia: BanRep Survey: economists expect BanRep to cut policy rate by 50bps in January; Manufacturing and retail sales showed mixed results in November, with a slight improvement, at the margin

Risk sentiment is a bit less negative today, with gains across most currencies versus the USD, cash and equity futures rising slightly, rates markets correcting losses, and commodities mixed to stronger. Still, the overnight moves look mostly corrective rather than a reflection of improving sentiment as Middle East risks grow and China growth negativity prevails, while most G10 central bankers stick to a hawkish tone ahead of their late-Jan/early-Feb decisions. The G10 day ahead has US housing starts and building permits and the ECB’s meeting minutes as the highlight alongside more Fedspeak.

US 2yr yields are down 5bps on the day, well shy of undoing the 14bps rise yesterday (its largest one-day jump since June) on a slashing of cut bets amid strong data and hawkish comments from policymakers. US equity futures are flat in industrials to stronger in tech, WTI oil is 0.5/6% higher, iron ore recoups losses with a 3% rally, and copper is little changed. The USD is down marginally against most major currencies.

The MXN is extending its gains that began Wednesday morning and is now trading just a touch better than where it closed on Tuesday, around the 17.15 level thanks to a 0.2% rise on the day thanks to the broad USD-negative mood. Yesterday, President AMLO unveiled his plans to finance his full salary pension reform plan by increasing public contributions rather than increasing employee or employer contributions; this would be achieved by ’republican austerity’ and eliminating autonomous bodies like the country’s energy regulatory commission. The Pres will present on the 5th of February a set of reform proposals, including pension, electoral, and judicial.

Peru’s central bank chief Velarde spoke in Davos yesterday, but he didn’t give too much away and it still looks like the 25bps cutting pace will continue. He spoke on the political uncertainty in the country and the need for changes to constitutional rules, while highlighting that in contrast to political turbulence economic stability has been maintained over the past eight years. He is, at writing, speaking at a Davos panel titled “What Next for Monetary Policy?” alongside other current and past central bank governors.

Today’s Latam highlight is the release of Colombian November economic activity data at 11ET, where the median expects a 1.2% y/y rise in output after a 0.4% drop in October; our team in Bogota projects a much better 2.5% y/y result. Today’s data follow a mixed set of results in industrial and retail sales figures released yesterday (see below) that nevertheless support our above-consensus forecast for economic activity. Despite better growth in November, us and the median economist (see below) expect BanRep to reduce its policy rate by 50bps at its late-January decision.

—Juan Manuel Herrera

COLOMBIA: BANREP SURVEY: ECONOMISTS EXPECT BANREP TO CUT POLICY RATE BY 50BPS IN JANUARY

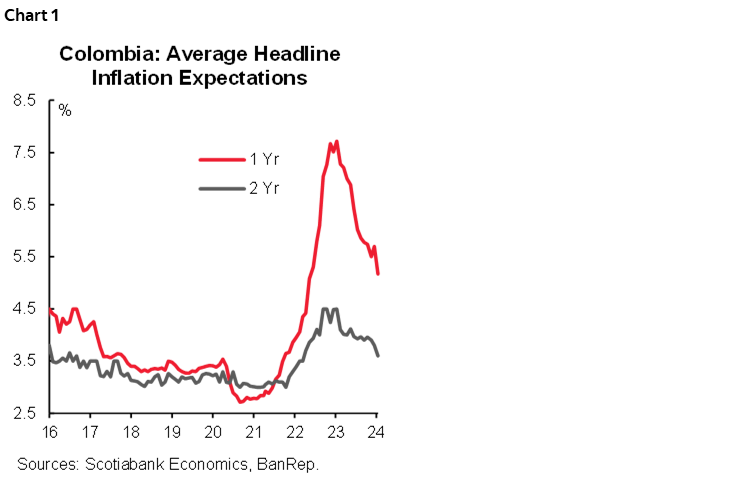

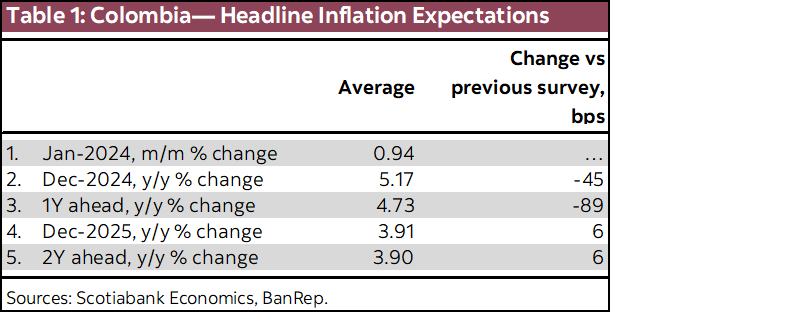

Late on Tuesday, January 16th, the central bank (BanRep) released the economist’s expectation survey for January. Inflation expectations fell in the 1y horizon, while now economist consensus forecasts a 50 bps rate cut on January 31st, which is the same expectation we have at Scotiabank Colpatria. For Dec-2024, inflation expectations fell by 45 bps to 5.17%, still above BanRep’s target range of 2% to 4%. For Dec-2025, inflation is expected to be 3.91% y/y, within the target range. That said, by the end of 2024, economist consensus expects the monetary policy rate to be 8.25%, above our expectation of 7%.

In the short-term, the inflation expectation for January stood at 0.94% m/m, which could take the annual inflation to ~8.4% y/y from the current 9.28%. Scotiabank Colpatria’s projection is 0.76% m/m, which will reflect moderated food and utilities inflation, the last increase in gasoline prices, and indexation effects that will be lower compared with the observed in 2023. That said, our projection involves an annual headline inflation reduction to 8.17%.

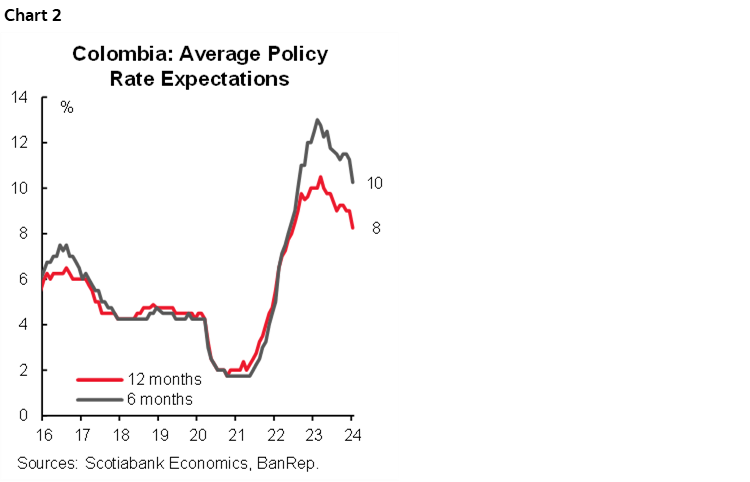

All in all, economist consensus affirms the expectations that the easing cycle should continue; in that sense, we noticed the consensus is pointing to a 50 bps rate cut in the January, March, April, and June meetings, and a possibility to accelerate the pace in July’s meeting with a 75 bps rate cut. Either way, the terminal point is similar to the previous survey’s 8.25%. At Scotiabank Colpatria, we expect a 50 bps cut and potential acceleration in the easing cycle in March and April to close the year with a 7% rate. We think that the main discussion for the central bank in the forthcoming meeting will be around, inflation expectations reduction and the economic activity deceleration since now consensus projects a 1% GDP expansion for 2023 and 1.46% growth for 2024, weaker than October’s survey of 1.22 and 1.77%, respectively (chart 1).

Key points from the survey:

- Short-term inflation expectation. For January, the consensus is 0.93% m/m, which implies an annual inflation rate of 8.40% y/y (down from 9.28% in December). The maximum expectation is 1.35%, and the minimum is 0.51%. Scotiabank Economics forecast is 0.76% m/m and 8.17% y/y. In January, the government decided to increase gasoline prices for the last time but also increased toll fees by 13.12% to catch up with the increase that was avoided in 2023. Scotiabank Colpatria’s deviation vs consensus is apparently in the ex-food inflation since consensus projects 0.96% m/m and our projection is 0.82% m/m, which implies that the main difference could be around the assessments of indexation effects and regulated prices due to the El Niño phenomenon effects in energy fees.

- Medium-term inflation showed an encouraging picture. Inflation expectations for December 2024 decreased by 45 bps to 5.17% y/y (table 1). The headline inflation expectations for the one-year horizon were at 4.73% y/y, while the two-year outlook was relatively stable at 3.90% y/y, within the central bank target range.

- Policy rate. The median expectation points to a 50 bps rate cut in January’s meeting. It is worth noting that the expected monetary policy path, on average, was unchanged. For Dec-2024, the monetary policy rate is expected to be 8.25%, while for the end of 2025, it is expected to be 5.50%. Scotiabank Colpatria’s projection is 7% for Dec-2024 and 5.5% for Dec-2025 (chart 2).

- FX. The projections for the USDCOP exchange rate for the end of 2024 averaged 3934 pesos (70 pesos below previous survey). For December 2025, respondents, on average, expect the peso to settle at USDCOP 3984 pesos.

—Sergio Olarte & Jackeline Piraján

MANUFACTURING AND RETAIL SALES SHOWED MIXED RESULTS IN NOVEMBER, WITH A SLIGHT IMPROVEMENT IN THE MARGIN

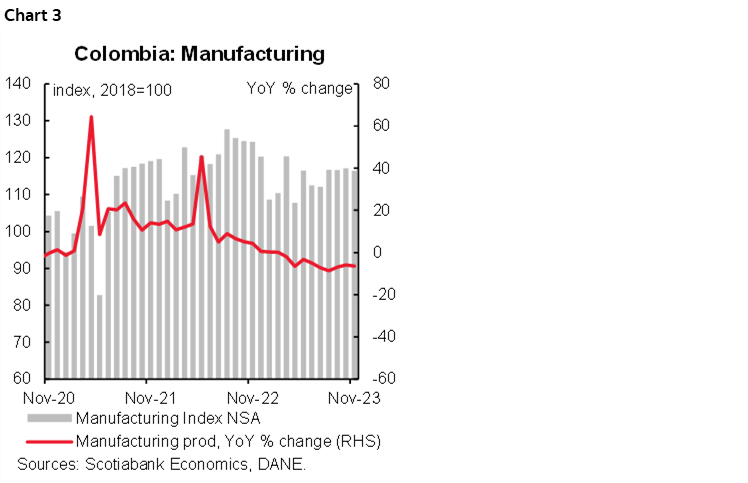

On Wednesday, January 17th, the National Statistics Institute (DANE) published the manufacturing and retail sales data for November 2023. Real manufacturing production recorded a contraction of 6.4% y/y in November 2023, below market expectations and our forecasts (-5.5% y/y). As for real retail sales, they contracted by 3.4% y/y in November, surprising the market to the upside, which expected a decline of 6.1% y/y, showing an improvement since the contraction was lower compared with previous numbers. It was the ninth consecutive month of annual contraction in manufacturing and the tenth consecutive month of contraction in retail sales. At the margin, however, both indicators showed a slight rebound from the previous month, as retail trade expanded by 2.3% m/m (vs. -1.3% m/m in October) while manufacturing contracted by 0.2% m/m in November from a contraction of 0.9% m/m in October.

On the manufacturing side, transport equipment was the sub-sector that contributed negatively to the November results. In the commerce space, we saw an improvement at the margin, which is compatible with some signals from sentiment surveys. In November, Fenalco’s sentiment survey revealed that commerce associations reported a recovery in sales of durable and semi-durable goods, such as household appliances, furniture, and vehicles, something that occurred in the context of significant discount campaigns (Black Friday and Cyber Monday) and the November Auto Show in Bogotá, which generated a total of 18,497 registrations in that month, a growth of 33.8% m/m compared to October. We also attribute this behaviour to the COP appreciation since atypically, stores maintained discount campaigns not only during November but also during the holiday celebration in December 2023.

December’s data could yield a mixed result. This forecast is based on the last publication of Fenalco in December, which suggested that for about 80% of the interviewed entrepreneurs, sales were similar or decreased (45% said they were similar and 35% reported a decrease) compared to the end of 2022. On the other hand, 20% of the respondents managed to increase the physical quantities sold compared to December 2022.

While the Colombian economy is in an orderly adjustment process, the decline in investment and the lower demand for durable and semi-durable goods have favoured the reduction in the closure of the current account deficit gap. The economy is expected to maintain weak momentum in the coming quarters, with annual growth rates below 2% in 2023 and 2024, as domestic demand adjusts to more sustainable levels. The investment part of the economy is the most uncertain part due to higher costs, high interest rates, and lower domestic demand.

Having said that, the deceleration in the dynamics of economic activity has allowed inflation to decelerate at a faster pace to 9.28% by the end of 2023, allowing BanRep to start the easing cycle with a 25-bps cut to 13% in December. As we expect inflation to decelerate further to 4.4%, we also expect BanRep to accelerate the easing cycle, reaching 7% in December this year. Today’s data also contributes to the discussion of a potential 50 bps rate cut to 12.50% in January’s BanRep meeting, which is our base case scenario.

Highlights:

Manufacturing Production:

- Manufacturing production contracted 6.4% y/y in November 2023 (chart 3), below market expectations (-6.1% y/y) and completing nine consecutive months of declines in 2023. On a seasonally adjusted basis, manufacturing contracted at a slower pace, from -0.9% m/m in October to -0.2% m/m in November.

- Out of the 39 industrial activities covered by the survey, a total of 32 recorded negative annual variations in their real output, subtracting 8.3 pp from the total annual variation, and 7 subsectors with positive variations added a total of 2.0 pp to the total variation.

- The largest annual contractions were in the transport equipment (-69.1% y/y and a contribution of -1.1 pp), clothing (-14.0% y/y and a contribution of -0.6 pp), other food products (-8.1% y/y and a contribution of -0.5 pp) groups. These activities accounted for -2.8 pp of the total annual variation in manufacturing production.

- On the other hand, other important industries recorded annual decreases, particularly those related to consumer durables and semi-durables, such as paper and paper products (-10.1% y/y and -0.4 pp contribution), textiles (-18.4% y/y and -0.4 pp contribution), furniture, mattresses and beds (-12.0% y/y and -0.1 pp contribution) and footwear (-10.4% y/y and -0.1 pp contribution).

- In contrast, the best-performing activities were coking, refining and blending of petroleum products (+19% y/y and 1.0 pp contribution), beverages (+3.1% y/y and 0.4 pp contribution), soap and detergents, cleaning and polishing preparations (+4.4% y/y and 0.2 pp contribution), other manufacturing (+12.3% y/y and 0.2 pp contribution) and machinery and equipment (5.8% y/y and 0.1 pp contribution).

Retail Sales:

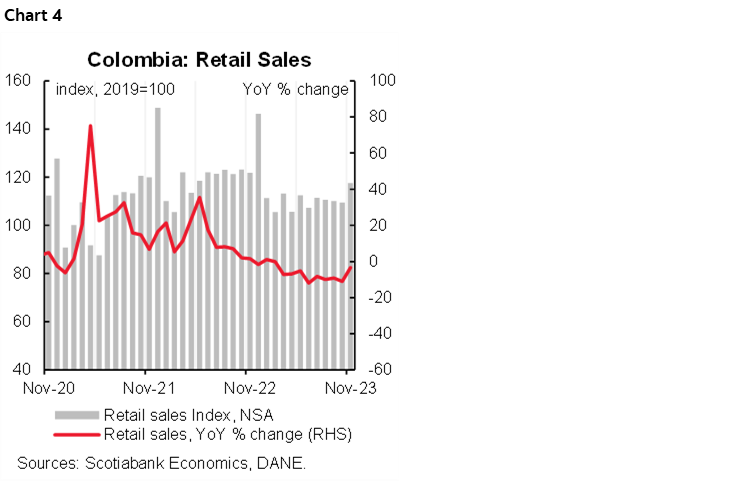

- Retail sales contracted by 3.4% y/y on November 2023 (chart 4), beating market expectations (-6.1% y/y) but ending 10 months in negative territory. In seasonally adjusted terms, retail sales excluding freight vehicles and public transport rebounded from the previous month, rising 2.3% m/m (vs -1.3% m/m in October).

- Out of the 19 product lines, 14 reported negative annual variations in real turnover, while 5 product lines reported an increase in turnover.

- On an annual basis, the performance of retail sales in November 2023 was influenced by declines in sales of other motor vehicles and motorcycles (-12.8% y/y and -1.1 pp), spare parts, and auto parts (-8.2% y/y and -0.6 pp) and hardware items (-13.2% y/y and -0.6 pp), household cars and motorcycles (-28.3% y/y and -2.7 pp) and, in total, these three product groups contributed to a -2.3 pp decline in total retail sales.

- In contrast, the largest positive contributions came from household cars and motorcycles (+2.3% y/y and +0.2 pp), household appliances and furniture (+6.8% y/y and 0.2 pp), which together contributed 0.4 pp to the overall change.

Services and Hotels:

- In November, fifteen of the eighteen service subsectors recorded positive y/y changes in total nominal income. The best-performing subsectors were health services (+17.9% y/y), restaurants and bars (+15.7% y/y), and computer service activities (+15.6% y/y). On the other hand, the sub-sectors that registered declines were news agency activities (-5.6% y/y), call centers (-11.2% y/y), and supporting activities for warehousing and transportation (-13.1% y/y).

- In the hotel sector, revenues fell by 3.6% y/y in real terms in November. In addition, hotel occupancy reached 56.9% in November, the highest level in 2023 and more than 6 pp above the pre-pandemic average.

- The still positive performance in services sectors makes us affirm our expectation of a 2.4% y/y expansion in the economic activity in November.

—Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.