- Peru: November GDP growth of 0.3% was encouraging yet unconvincing at the same time

Markets again have a risk-off feeling to them, but on relatively limited or mixed drivers. Trump smashed the opposition in the Iowa caucus, but that shouldn’t be a surprise despite doing better than expected. Middle East/Red Sea risks continue to grow, and central bankers are starting to highlight how this is a risk to recently encouraging inflation data due to supply chain disruptions. Chinese authorities are reportedly readying USD140bn in ultra-long special bond issuance in the second half of the year for stimulus purposes, but these headlines came and went for markets.

The UST curve opened cheaper and then cheapened further in early-Asia and then in early-Europe to have US yields about 6bps higher across the curve with no clear bias, opposed to stronger steepening gilts and EGBs. US equity futures are off about 0.5%, roughly matching the losses in cash FTSE but worse than ESX’s 0.3% drop. Crude oil is mixed to stronger, especially in Brent, while copper is up 0.8% and iron ore gains 1.5%.

The USD is having a very strong day where the gains picked up some more over the past hour to have the greenback 0.5% or more stronger against all major currencies. The broad Bloomberg dollar index is now at its strongest since mid-December which was right around when US yields took another dive on the Fed’s dovishly-perceived hold.

The MXN is among the worst performers on the day as it tracks a 0.9% drop, weighed by the weakness in high-beta FX on risk-off sentiment but also the rise in US yields. A Pemex board member calling for some of the company’s debt to become public may not be helping either. The MXN has been here before since the start of the year, through the 17 pesos mark, to then manage gains as buying pressure emerges above the figure; let’s see if that holds again today though the broad dollar backdrop is not encouraging.

There’s not much to follow in Latam today. Data-wise, Brazilian services volume figures for November are the only release, with economists expecting a 0.4% m/m rise after a 0.6% contraction in October. BanRep’s economists survey results due for publication today may show a greater share of economists favouring a larger cut at the bank’s rate decision on the 31st; we expect a 50bps reduction. Colombia’s Pres Petro and Fin Min Bonilla speak in Davos today. Canadian CPI and central bank speakers are the G10 highlight.

—Juan Manuel Herrera

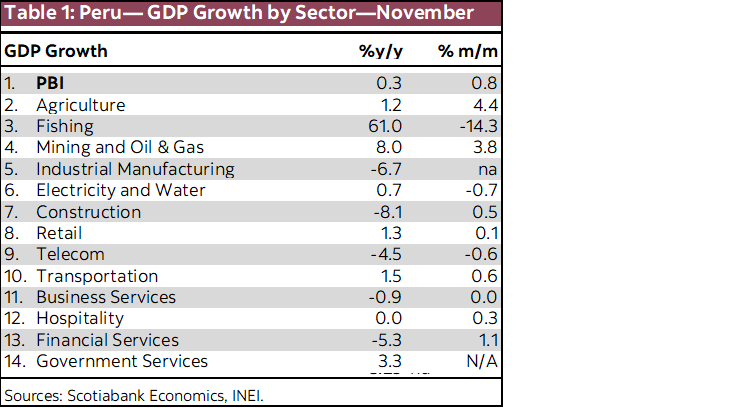

PERU: NOVEMBER GDP GROWTH OF 0.3% WAS ENCOURAGING YET UNCONVINCING AT THE SAME TIME

GDP rose 0.3% y/y in November. Yes, that’s right, growth was positive. This hasn’t happened since April and, although recent data had suggested November growth would be mildly positive, this was not evident until then.

Ironically, the sectors that led in growth included sectors that had been severely affected by severe weather earlier in the year, namely fishing, up 61% y/y (versus -11.4 YTD) and agriculture, which rose 1.2% y/y in November (-3.6% YTD). Mining also contributed, rising 10.6% y/y (8.0% in conjunction with oil & gas), although this was similar to its performance throughout the year.

The fact that GDP growth was up 0.8% in month-on-month terms was also encouraging, although one cannot call this a trend reversal until sectors linked to domestic demand begin to participate. Which is still not happening. In fact, the downside to November’s numbers was the persistent decline in sectors linked to domestic demand. Industrial manufacturing no longer declined the 8%–9% of previous months, but the improvement has yet to be significant. The decline in construction GDP growth was also persistently high, and just a hair lower than previous months.

In short, growth in November relied nearly exclusively on resource sectors, while those sectors most linked to domestic demand continued weak. Until this changes, GDP growth will continue to be weak. Although, base comparisons will begin to help starting quite early in 2024.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.