- Peru: BCRP to continue rate cut cycle with inflation in target range and a weak El Niño

- Colombia: Consumer expectations improved in December

- Mexico: In October, gross fixed investment rose, led by construction; Private consumption improved on imported goods

Global markets are waiting for US CPI at 8.30ET and today we don’t even have a flood of supply to keep desks busy. There was a decent risk-on feel to markets in Asia hours that was checked somewhat in early-European trading, but its benefits remain at writing to have global curves bull flattening, equity cash and futures in the green, a broadly weaker USD (though coming back from its worst intraday levels), and commodities generally bid.

The MXN is weakening through the 17 pesos level again while holding in a very narrow 16.95–17.02 range since Tuesday afternoon as it tracks the worst performance of all major currencies so far this week, falling 0.8% in a week that has UST-sensitive FX on the backfoot (see JPY also underperforming). Unsurprisingly, local investment data published yesterday (see below) had little impact on the MXN that continues to be driven by external developments. Today, industrial production data out at 7ET (a small m/m increase is expected) should also be mostly inconsequential for domestic assets.

Brazil’s inflation figures for December at 7ET are the main data release in the Latam region today, and the BCRP’s decision at 18ET is the highlight (see below). Economists expect a slight slowdown of headline inflation to 4.55% from 4.68% in November and a 0.5% m/m print that owes to seasonal increases in food prices and a jump in airfares after 0.2% m/m in November. Core price trends remain the focus, with the m/m pace of inflation in the trimmed basket sitting between 0.30% and 0.37% over the past four months.

Yesterday, the BCB’s Guillen said that the bank is comfortable with guidance for the next two meetings (50bps cuts) while highlighting that inflation expectations are not centred on target. The BCB’s 2025 target is 3% +/-1.5% but the central bank survey shows economists expecting a 3.5% pace of inflation in 2025 (same target and 3.9% forecast for 2024).

—Juan Manuel Herrera

PERU: BCRP TO CONTINUE RATE CUT CYCLE WITH INFLATION IN TARGET RANGE AND A WEAK EL NIÑO

We expect the BCRP to continue its interest rate cutting cycle at its meeting this afternoon. It would be the fifth consecutive cut of 25bps, taking its key rate to 6.50% as is also expected by the Bloomberg consensus.

The first readings for January inflation suggest that headline inflation would return to the target range (between 1% and 3%). This is much earlier than expected—according to the BCRP, this milestone would be reached in April—owing to the weakening of the intensity of El Niño, according to the most recent readings.

Food prices are reversing the supply shocks of previous months. The weakness of the economy also puts downward pressure on inflation, which would be reflected in core inflation falling within the target range, for the second consecutive month in January (after printing at 2.9% in December). Given these conditions, our forecasts for inflation are under review.

Twelve-month inflation expectations fell from 3.15% to 2.83% in the latest BCRP survey, returning to the target range after 29 months outside of it. With this, if the reference rate is cut by 25bps today, the real interest rate would still rise from 3.6% to 3.7%—remaining well above the neutral level of 2%.

—Mario Guerrero

COLOMBIA: CONSUMER EXPECTATIONS IMPROVED IN DECEMBER

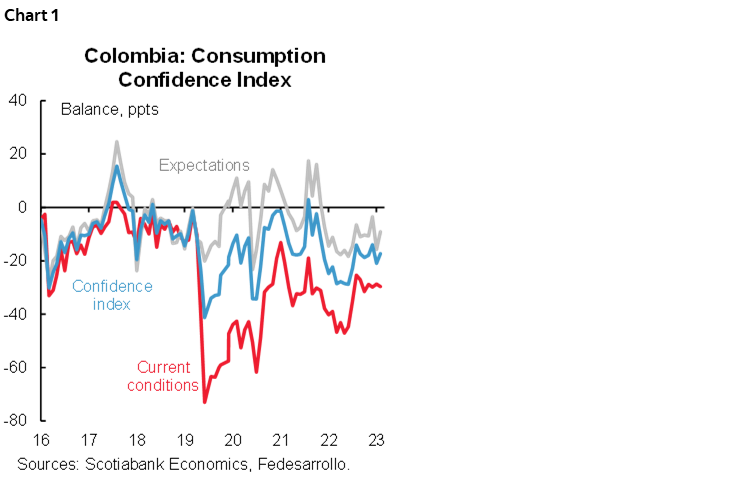

The Consumer Confidence Index (CCI) stood at -17.3% in December 2023, 3.6 pps higher than in November (-20.9%). The improvement of the indicator is explained by a 6.6 pps increase in the Consumer Expectations Index, which reversed the negative performance of November. On the other hand, the Economic Conditions Index showed a slight deterioration of 0.9 pps, standing at -29.6% (chart 1).

The result of the Consumer Confidence Index reflected an improvement in consumer expectations. Compared to the previous month, the indicator showed a strong recovery from -20.9% to -17.3%, largely explained by the Consumer Expectations Index (CEI) which in recent months has become the main driver of overall movement. In December, the IEC stood at -9.1% versus -15.7% in the previous month, an improvement in household economic expectations on a 12-month frontier was the main driver, behaviour that may be influenced by an improvement in overall economic conditions such as lower consumer inflation and expectations about interest rate cuts.

Although December is usually a costly month given the festivities, 2023 showed atypical behaviour, as food, clothing and durable goods stores maintained some discounts during the month, as evidenced in the inflation results which closed the year at 9.28% YoY. The better performance of inflation influenced households’ perception of their current economic conditions compared to a year ago. This behaviour is expected to continue throughout the year, due to the expected further inflation convergence, that will allow Banco de la República to continue the easing cycle with more certainty, easing households’ financial burdens and reducing borrowing costs. Even so, the timing and magnitude of interest rate cuts will continue to depend on the behaviour of inflation (chart 2).

Looking at the November details:

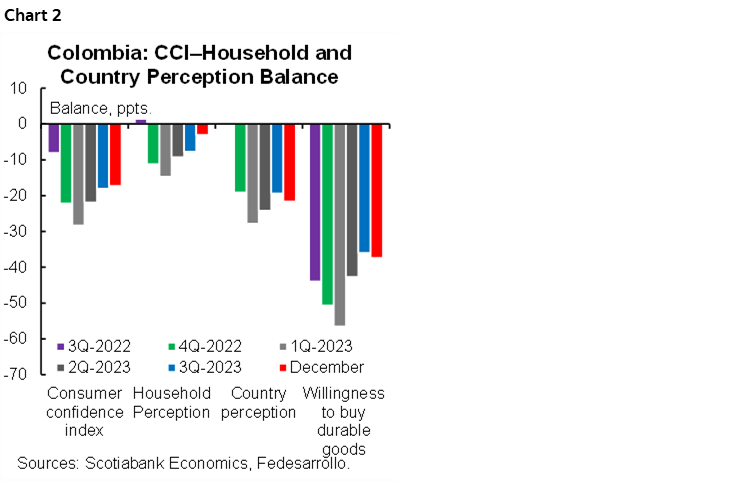

- The Economic Conditions Index stood at -29.6%, falling 0.9 pps from the previous month. Consumers’ perception of current economic conditions showed an improvement of 6.4 pps, contributing positively to the CEI. Meanwhile, it offset the 8.3 pps deterioration in the willingness to buy durable goods, likewise, the willingness to buy housing also declined by 9.3 pps. Meanwhile, the willingness to buy vehicles increased by 2.8 pps.

- The expectations index stood at -9.1%, an increase of 6.62 pps from November. Households’ expectations about their economic situation in a 12-month horizon showed an improvement of 8.7 pps, resuming the positive behaviour of October. Likewise, the expectation about the country’s economy on a 12-month horizon improved from -35% in November to -28.2% in December.

- By socio-economic level, the middle-income group recorded the best performance. Confidence in the middle-income group increased by 8.1 pps to -16.1%, followed by the high-income group which recorded an increase of 6.7 pps to -43.9%. Meanwhile, the low-income group decreased by 0.7 pps to -15.3%.

- The Consumer Confidence Index improved in all the cities analyzed. Barranquilla was the city to register the best balance, with an increase of 11.7 pps to -4.4%, followed by the city of Bucaramanga with an increase of 3.5 pps.

—Sergio Olarte & Daniela Silva

MEXICO: IN OCTOBER, GROSS FIXED INVESTMENT ROSE, LED BY CONSTRUCTION

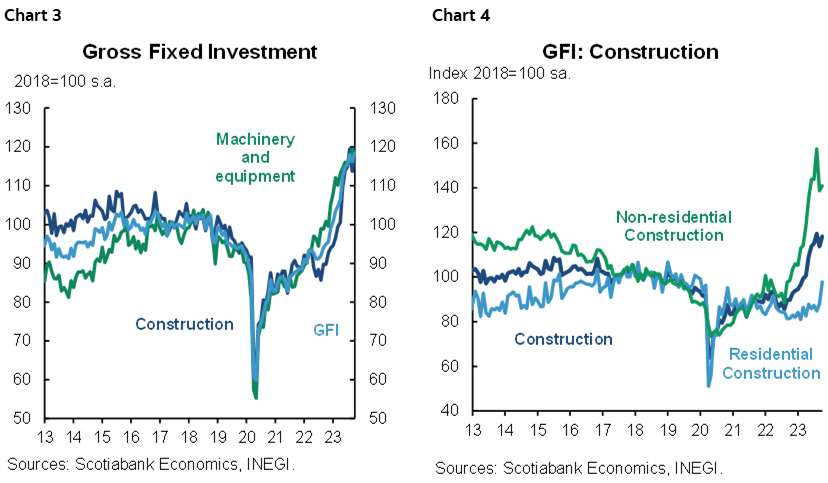

During October, gross fixed investment accelerated on an annual basis, going from 21.9% to 25.5% y/y n.s.a. Machinery and equipment rose 19.3% (18.8% previously), see chart 3, as the domestic subcomponent slowed down to 14.1% (21.5% previously), and the imported subcomponent rose 22.9% (17.1% previously). Construction soared 31.6% (24.8% previously), non-residential construction stood at 41.0% y/y (39.0% previously) and residential construction edged up to 20.9% (8.5% previously), see chart 4. In the seasonally adjusted monthly comparison, GFI rebounded 1.9% (-1.5% previously), as machinery and equipment fell -0.6% (2.7% previously), and construction rose 4.0% (-4.9% previously). In a cumulative basis from January to October, the index has increased 20.4% YTD.

Private machinery and equipment hold double-digit increases for the last fifteen months, this time it rose 20.2% y/y (19.6% previously), possibly owing to the renewal of depreciated equipment, in contrast to the public component, which have shown weak increases, this time 0.8% y/y (0.9% previously).

Regarding construction, the private sector has had ten consecutive months of increases, this time at 32.9% y/y (23.9% previously). On the other hand, public construction has shown positive percentage changes for seventeen months, despite it decelerating this time to 26.5% y/y (28.5% previously). We expect public construction to slow as government infrastructure projects are completed, however, private construction could remain with advances if nearshoring expectations materialize in 2024.

PRIVATE CONSUMPTION IMPROVED ON IMPORTED GOODS

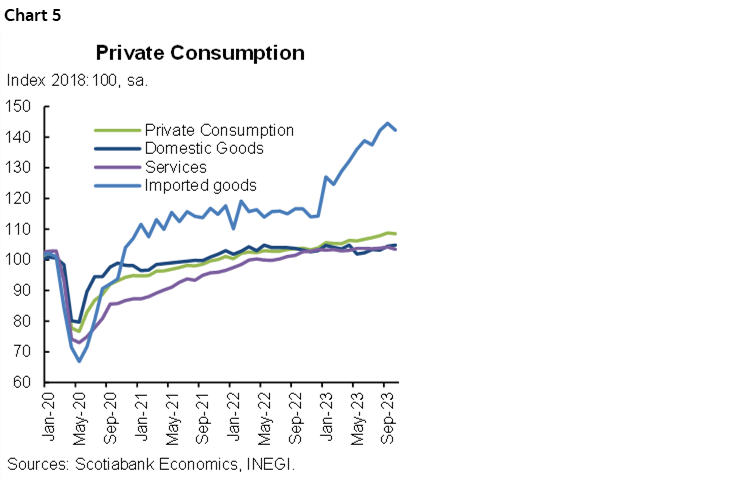

In October, private consumption soared to 5.2% y/y from 4.5% n.s.a. in real terms. The greatest advance came from imported goods (chart 5), which accelerated from 20.8% to 27.4%, in line with the appreciation of the USDMXN, closing 2023 with an advance of 13.0%. In the domestic component, services continued with a moderating trend, going from 2.8% to 0.5%. In contrast, domestic goods increased from 0.0% to 2.3%. In detail, durable goods accelerated to 17.7%, despite restrictive rates, followed by an 8.2% advance in semi-durable goods, and a -0.8% drop in non-durable goods, adding up to eight months of declines.

On a monthly seasonally adjusted basis, private consumption dropped -0.3% m/m (0.8% previously), as services declined -0.7%, and imported goods fell -1.6%, even though domestic goods rose 0.4%.

Going forward, we consider that private consumption will maintain an accelerated pace until at least the first half of 2024, supported by the strong increase in public spending, the strength of remittances, as well as a solid labour market, with considerable increases in real wages.

—Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.