- Colombia: BanRep board expects to accelerate the easing cycle if current sources of uncertainty dissipate

- Peru: BCRP goes for a sixth rate cut

It was narrow rangebound trading across the key asset classes in Asia hours, with markets broadly ignoring Moody’s—somewhat expected—downgrade of NYCB to junk (which triggered a 17% drop in after-hours trading). Yesterday’s slide in the bank’s shares, which dragged the broad regional banks complex lower, helped US yields fall to around their opening levels on Monday. The past hour has seen a bit more activity in rates markets, with US, UK, and Eurozone debt weakening across the curve by a few bps, while US equity futures slip a touch and the USD trades mixed. Crude oil is up about 0.5%, but copper and iron ore are little changed.

The G10 calendar only has second-tier data on tap, US and Canadian international trade and the EIA’s oil report, but a flood of Fed speakers this afternoon (Kugler, Collins, Barkin, Bowman) and the BoC’s summary of deliberations (discount minutes). Overnight, New Zealand’s employment report beat expectations across all lines, with jobs growth, wages, and the unemployment rate all coming in better than expected. Comments this morning by the BoE’s Breeden and the ECB’s Schnabel were along party lines, counselling caution on lowering policy rates too soon.

At 18ET, we get Colombian CPI data for January that us, and the economist median, expect will show a ~0.8–1.0ppts decline in year-on-year headline inflation as well as the first single-digits core inflation reading since late-2022. Our team in Colombia projects that inflation fell from 9.28% in December to 8.17% last month in headline terms (Bloomberg median: 8.37%) and from 10.33% to 9.47% in core terms (median: 9.69%). The steep deceleration from December owes to favourable base effects in food, merchandises, and indexed prices that will be evident over the balance of Q1, which we expect will end with a 6.6% y/y inflation pace in March. The rapid drop in inflation in today’s data and February figures out on March 7 should prompt a larger cut by BanRep at its March 22 meeting.

Over the course of the morning, Chile publishes January international trade and December wages data, and Brazil releases December retail sales and fiscal balances and also January international trade. These data should have limited influence on local markets that are better off waiting for the release of January CPI in both countries, accompanied by Mexican prices data. Note that yesterday’s Citibanamex survey results showed that analysts still expect Banxico to start cutting rates next month, by 25bps, but the median now thinks that the overnight rate will end the year at 9.50%, 25bps higher.

—Juan Manuel Herrera

COLOMBIA: BANREP BOARD EXPECTS TO ACCELERATE THE EASING CYCLE IF CURRENT SOURCES OF UNCERTAINTY DISSIPATE

The central bank released the minutes for January’s monetary policy meeting on Monday, February 5th. BanRep’s board agreed that there are conditions to continue reducing the repo rate, especially amid the headline inflation reduction and the economic activity deceleration that reflects a weaker labour market performance. However, the split vote in which five board members voted for a 25bps rate cut and two members for a 50bps cut is explained by the uncertainty around the medium term for headline inflation, especially in the core services inflation. The minority group, who voted for a 50bps cut, showed a higher concern about economic activity and employment. The majority group also said that they would speed up the easing cycle if the source of uncertainty dissipated.

That said, in Scotiabank Colpatria Economics, we think that CPI inflation in January and February and the GDP to be released on February 15th will be key data for the central bank to decide to go for a higher rate cut in the March 29th meeting. Our base case scenario is that inflation will go down significantly in the forthcoming months, which could open the possibility of seeing a rate cut between 50 or 75bps in the March and April meetings. For now, we affirm our expectation of the monetary policy rate closing at 7% in 2024.

Further details about BanRep’s minutes:

- The minutes reflect that there is consensus about continuing with the easing cycle; however, in January, the debate about the size of the rate cut relied on the assessment of inflation and economic growth risk. Regarding inflation, the majority group (5 members who voted for a 25bps cut) is concerned about indexation effects that could arise after the increase in the minimum wage, which was higher than their projection. On the other hand, they highlighted that the risk of speeding up the easing cycle is losing credibility in the commitment to the inflation target. They said that if uncertainty dissipates, they could consider going for stronger cuts in forthcoming sessions.

- In the case of the minority group (two members who voted for a 50bps cut), the main concern was around economic activity, pointing to a significant weakening in consumption and investment. That said, they consider the 25bps cut insufficient and imply maintaining a contractive real rate, which could impact the economic activity recovery.

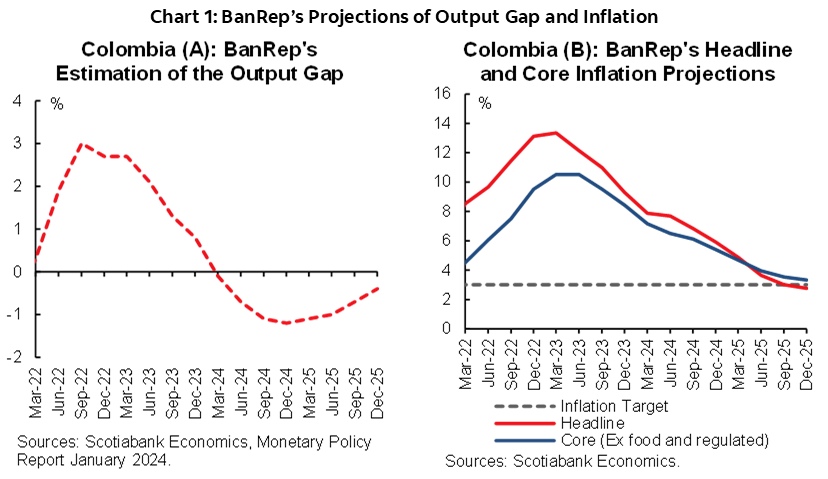

- In addition to the minutes, the Central Bank staff released the Monetary Policy Report on Friday, February 2nd. In the report, the economic staff said that inflation remains well above the 3% target and the expected headline inflation for the year-end at 5.90%, while they project the economic activity will continue weakening in 2024, expanding by 0.8%, before resuming an acceleration path in 2025 with an expected expansion of 3.5%. That said, BanRep’s macro scenario involves having a rate path above the median expected by economists’ consensus, which currently points to a year-end rate between 8% and 8.5% (chart 1, panel B). The path suggested by BanRep’s staff is compatible with inflation achieving the 3% target in around 18 months, however, it could imply further economic activity deceleration, as they assumed Colombia’s output gap will be negative in forthcoming quarters (chart 1, panel A.).

- The key word in both BanRep’s publications is uncertainty, particularly around indexation effects. In that regard, we think the two forthcoming CPI readings are critical to increase the confidence in BanRep to pursue a faster easing cycle. The impact of climate events such as the “El Niño” weather phenomenon is difficult to anticipate. Still, in any case, if there is some impact, it probably won’t affect the H1-2024 inflation. Our base case scenario shouldn’t prevent BanRep from speeding up the easing cycle on forthcoming meetings.

- Real rates matter more: in the Monetary Policy Report, staff calculation points to a neutral rate of 2.4% in 2024 and 2025; having said that, we think the central bank will try to maintain the real monetary policy rate slightly above the neutral rate, but if inflation eases faster, the nominal policy rate will decrease faster. Again, the critical piece of information is how fast inflation decreases.

—Sergio Olarte & Jackeline Piraján

PERU: BCRP GOES FOR A SIXTH RATE CUT

We expect the BCRP to continue its interest rate cut cycle for the sixth time at its meeting this Thursday, February 8th, by 25bps, to 6.25%, a level expected by the entire market consensus, according to a Bloomberg survey.

The first readings for inflation in February suggest that inflation would be close to the historical average (0.30%), meaning inflation would remain close to the upper limit of the target range (3%). February inflation would be higher than the practically zero variation in January (0.02%), due to seasonal factors and the impact of a higher FX rate and higher local fuel prices.

Food prices are reversing the supply shocks of previous months. The weakness of the economy would keep core inflation within the target range for the third consecutive month.

Twelve-month inflation expectations fell from 2.83% to 2.64% in the latest survey, within the target range for the second consecutive month. Despite this, if the rate was cut by an additional 25bps this Thursday, the real interest rate would go from 3.7% to 3.6%, still well above the neutral level of 2%.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.