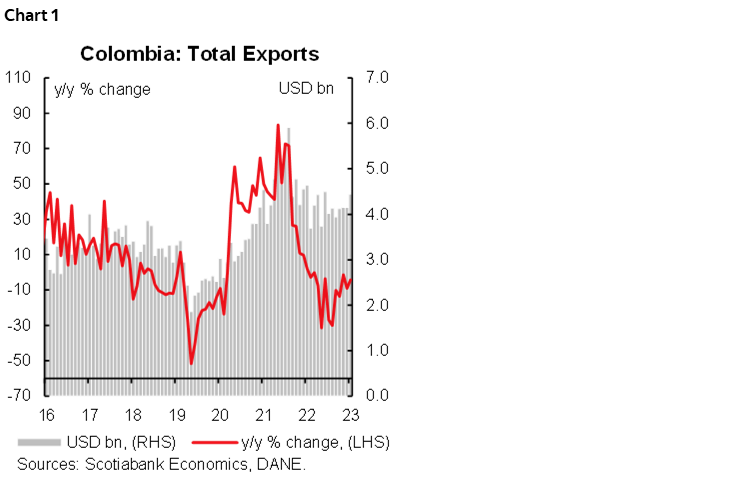

- Colombia: Exports rebounded in December, while the 2023 balance was in contractionary territory

Markets are in a so-so mood as more risk-positive moves during the Asia session are unwound in European trading ahead of a quiet data day in the Americas. The overnight highlight was the RBA’s relatively hawkish rate decision that left the door open to more tightening if needed.

Major currencies are mixed in +/-0.2% ranges versus the USD with the MXN little changed around 17.10, US equity futures are around an intraday low to sit flat on the day, and curves are steepening (bull in the US, bear in Germany). Key commodities are mixed (steady copper and oil, iron ore weaker) with no lasting support from China optimism. It was another day, another round of Chinese public funds adding to their holdings of ETFs alongside wishy-washy support pledges by officials that triggered 3.5–4.0% gains in the main HK and mainland indices.

Mexican markets reopen today to a quiet session where only the release of the bi-weekly Citibanamex survey of economists is on tap. Elsewhere in the region, only the BCB’s meeting minutes stood out in today’s calendar, though at quick glance it seems that no discussion took place on when to switch to a lower pace of rate cuts; officials unanimously (and as expected) agreed on half-point cuts expected in coming meetings. Local markets have but to wait for tomorrow’s Colombian CPI, followed by Wednesday’s Mexican, Chilean, and Brazilian CPI, and BCRP and Banxico decisions.

Mexico’s AMLO presented yesterday his well-expected package of constitutional reforms that include pension, electoral, Supreme Court, minimum wage, and energy reforms, among others. With the president’s allies in Congress falling short of the two-thirds required for constitutional amendments, it is highly unlikely that these will succeed, but their discussion and eventual rejection will likely be used to rally support for his party ahead of this year’s elections.

In Peru, on the heels of last week’s downgrade of Petroperu, Fitch said yesterday that structurally higher fiscal deficits place the sovereign’s rating at risk—despite its projection of a narrowing of the country’s deficit in 2024. Still, Fitch notes that the government’s deficit projections of 2% and 1.5% of GDP in 2024 and 2025, respectively, are based on optimistic growth projections (3.0% in 2024 compares to our forecast of 2.7%, and Fitch’s 2.1%). We’ll keep an eye on comments by officials on the fiscal trajectory and Petroperu’s finances with Fitch highlighting that “the possibility of greater support for Petroperu” is among risks to the country’s fiscal standing. Note that, on Saturday, the government changed the ownership mix of the company from 60% energy and mines ministry and 40% finance ministry to the inverse, which means the finmin is now the majority holder.

—Juan Manuel Herrera

COLOMBIA: EXPORTS REBOUNDED IN DECEMBER, WHILE THE 2023 BALANCE WAS IN CONTRACTIONARY TERRITORY

The National Statistics Institute (DANE) published export data on Monday, February 5th. Monthly exports in December 2023 amounted to USD 4.44 billion FOB, with a decline of 4.2% y/y (chart 1) compared to December 2022. However, the rate of decline slowed compared to the November data. At the margin, there was a recovery, in fact, total exports grew 7.1% compared to the previous month, showing an improvement in levels compared to the stagnation of the last two months.

This result was again due to a 5.9% y/y decline in exports of fuels and extractive industries (contributing -3.2 pp to the total variation), whose value amounted to USD 2.38 billion FOB. This decrease was mainly due to the fall in exports of coal, coke, and briquettes (-28.1% y/y), which negatively contributed -12.6 pp to the variation of the group. Similarly, in December 2023, exports of the manufacturing group amounted to USD 839.8 million FOB (-2.5% y/y), due to a fall in exports of manufactured articles, classified mainly by material (-22.7% y/y) and miscellaneous manufactured articles (-9.0% y/y), which together contributed negatively with -9.0 pp to the variation of the group. The “other sectors” group contracted in December 2023 (-0.3% y/y), which was mainly explained by the fall in the other chapters of the group, excluding non-monetary gold, which contributed -1.3 pp to the variation of the group.

Among agricultural exports, food and beverages fell by 2.7% y/y and had a negative contribution of -0.5 pp (USD 910.3 million FOB). This decline is explained by a fall in exports of unroasted coffee in December (-12.8% y/y) and other cane or beet sugar (-42.3% y/y), which together contributed 6.4 negative pp to the group’s variation.

In terms of participation, in December 2023, the reference month, exports of fuels and products of the extractive industries participated with 53.6% of the total FOB value of exports; likewise, manufacturing with 18.9%, agriculture, food, and beverages with 20.5% and other sectors with 7.1%.

The full year of 2023 showed that Colombian exports amounted to USD 49.54 billion FOB, showing a decrease of 12.9% y/y, compared to 2022. This result was mainly due to a decrease in exports of the group of fuels and products of the extractive industries for a value of USD 25.91 billion FOB, a decrease of 18.6% and a negative contribution of -10.4 pp to the total variation.

While external financial conditions have shown signs of improvement, in an environment of global inflation with a declining trend and a smaller slowdown in the world economic activity than projected in 2023, it is expected that Colombia’s terms of trade will decline in 2024 due to lower dollar prices of exported products, especially the average international quotation of some export commodities, such as oil, coal, and coffee. This would be partially offset by the decline in dollar prices of intermediate goods imported by the country.

Key Highlights:

- Traditional exports (related to coffee, oil, and mining) declined in value but recovered in volume. To date, traditional exports totaled USD 2.6 billion FOB, a decline of -8.9% y/y, in contrast to the 9.6 million tons exported, whose growth was 15.3% y/y. For its part, in the whole of 2023, traditional exports reached USD 28.2 billion (-24.4%) and 93.4 million metric tons (0.6%).

- Among the components of traditional exports, oil and its derivatives increased by 10.5% y/y in December (USD 1.46 billion FOB) and a decrease of -16.6% in the period from January to December 2023 (USD 15.61 billion). Coal exports fell 28.1% y/y in December (USD 813.1 million), followed by coffee exports, which fell 12.7% y/y (USD 294.08 million). For the cumulative year, coal and coffee exports closed with declines of -25.4% (USD 9.16 billion) and -29.5% (USD 2.79 billion), respectively.

- In terms of volume, external sales of oil and its derivatives increased by 8.3% y/y in December (3.08 million tons) and by 4.1% y/y in 2023 (32.39 million tons). As for coal exports, they recorded an expansion of 19.1% y/y (6.47 million tons) in December, while coffee exports abroad were 13% y/y in December (~67 thousand tons). As for the exports of these items in the accumulated year, they recorded falls of -1.1% for coal (60.29 million tons) and -7.8% (~576 thousand tons).

- Finally, in terms of value, the external sales of ferronickel reached around USD 33.54 million, a decrease of 49.5% compared to December 2022. However, in the whole of 2023, the decrease was 29.8% (USD 637.34 million) compared to the same period of 2022. In terms of volume, there was a decrease of 25.3% y/y (10.27 thousand metric tons) compared to December 2022, while the balance accumulated between Jan–Dec 2023 exceeded 146 thousand metric tons and marked a growth of 1.7% compared to 2022.

- On the other hand, non-traditional exports reached USD 1.84 billion in December 2023, recording a growth of 3.2% y/y (chart 2) compared to December 2022. Moreover, in the period from January to December 2023, non-traditional exports reached USD 17.78 billion (-0.9% y/y vs. 2022).

—Sergio Olarte & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.