- Chile: Encouraging, but not confirmed, labour market recovery

Slightly hotter-than-expected Spanish, French, and German regional inflation prints have rates markets sharply weaker in European dealing, with moves looking somewhat stretched at writing as the selloff stalls. Strong UK credit data and hawkish comments by a BoJ official are also adding upward pressure on yields. USTs, EGBs, and gilts are all bear flattening as global markets await the release of the German CPI aggregate at 8ET, followed by Canadian GDP and US PCE data at 8.30ET, with month-end flows also set to play a role.

The risk mood is a touch negative today, as SPX futures lose a bit of ground while holding in the weekly range alongside flat SX5E and FTSE. The commodities backdrop is mixed as crude oil is unchanged while copper and iron ore record small increases. In the FX space the USD is confined to +/-0.2% ranges against most majors, with the JPY the clear exception, rallying 0.5% thanks to hawkish comments; the MXN is a touch firmer.

Yesterday’s Banxico quarterly report did not surprise on the forecasts front with slightly lower 2024 GDP and formal jobs growth forecasts, and only Dep Gov Heath seemed somewhat against a start to rate cuts in March saying the balance of risks is “very biased to the upside” and that it “would be a mistake to lower the rate too soon”. On the other hand, Gov Rodriguez held to her relatively dovish stance (sounding modestly confident about the inflation path), as did Mejia (who said a rate move should be considered due to better inflation), while Espinosa had a more balanced view noting that headline CPI deceleration may stall due to upside risks and that wage increases are pressuring services inflation. We expect Banxico to announce a 25bps reduction next month in a 4–1 vote split.

As we had highlighted as a possibility in yesterday’s report, Canada is due to reimpose visa requirement on Mexican travelers on the basis of slowing the inflows of asylum seekers—but also likely amid claims that Mexicans are using Canada as a gateway to the US. The requirement, which excludes seasonal workers and students, should be announced later this morning to come into effect at 23.30ET today. Yesterday, Pres AMLO said that he may skip the next North American leaders summit “if there is no respectful treatment” of Mexico. There is a chance that US Pres Biden also announces some measures to limit Mexican immigration or ramp up border safeguards. For Mexican assets, AMLO retaliation may be a greater risk than US or Canadian measures. Broadly, Mexico-US/Canada relations are trending in a negative direction and we may see more restrictive immigration/trade policies announced in coming months ahead of elections in the US and Mexico.

Today’s Chile data flood at 7ET is the highlight of the Latam day, while Mexican, Brazilian, and Colombian unemployment figures are worth a look, but are unlikely to shake up local markets too much. Chilean retail sales, industrial/manufacturing production, commercial activity, and copper output figures, all for January, will help us refine expectations for tomorrow’s economic activity data. Retail sales are seeing contracting again in y/y terms for the twenty-first month in a row, while closing in on the zero mark. Industrial production is expected to show only a small decline.

—Juan Manuel Herrera

CHILE: ENCOURAGING, BUT NOT CONFIRMED, LABOUR MARKET RECOVERY

- Private salaried job creation in commerce and construction; the worst in these sectors would have been left behind

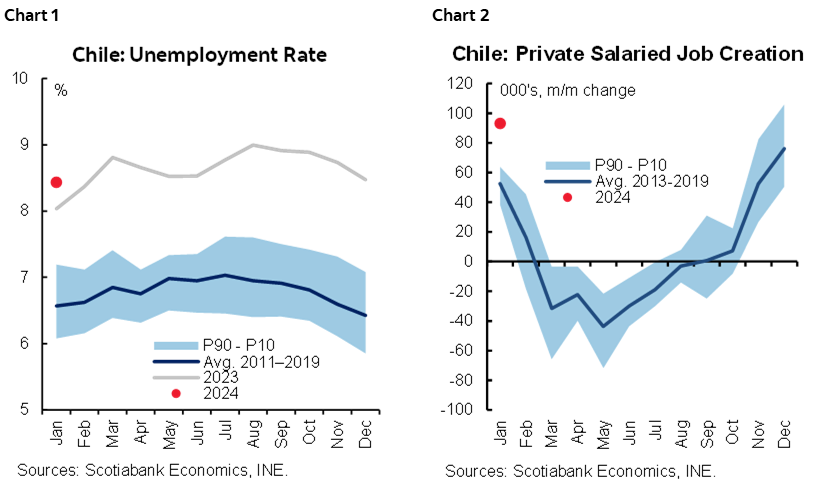

On Wednesday, February 28th, the statistical agency (INE) released the unemployment rate, which fell to 8.4% in the quarter ending in January 2024, below market expectations (consensus: 8.6%) and closer to our projection of 8.5%, although still high based on a historical perspective (chart 1). The drop in the rate was explained by the creation of 50k jobs, similar to the evolution of the labour force, which confirms the green shoots we reported in the last two moving quarters. Reflecting this is the strong creation of private salaried employment (+93k, chart 2), the highest in almost two years (since Feb 2022), concentrated in agriculture, construction and commerce, although stronger than seasonal in the latter sector. At Scotiabank, we continue to see weakness in the labour market, although framed within a recovery. Signs of recovery in private employment in construction and commerce could be indicating that the worst in these sectors is behind us. We expect the pace of job creation to slow in the next few months, but to continue to be marginally positive due to the execution of scheduled private and public investment.

Thus, the good creation of private salaried employment (+93k) provides support to the labour market without taking into account the creation of public employment or self-employment. The increase in private salaried employment was well above the usual seasonality for the month of January, being one of the few categories that created jobs in the month. In fact, the public sector destroyed 14k jobs, while 29k self-employed jobs were lost. With this, the labour market continues to move towards greater formalization, providing more sustainable support to private consumption. In this regard, 35k formal jobs were created, the third consecutive increase in this type of employment. Although last year there was also a strong creation of salaried employment in the same period, it was led by the public sector, unlike what is happening this year, where the private sector seems to be regaining dynamism.

Commerce and construction led in job creation, indicating that the worst is now behind us in these sectors. Employment in commerce has fully recovered to its pre-pandemic level, while construction continues to lag far behind. While the figures at the margin contribute to the recovery of employment in the sector, it is still far from the pre-Covid level. Agriculture also stood out for the increase in employment, although this was not very different from the usual seasonality observed in the sector. On the negative side, the destruction of employment in the manufacturing industry, which was mainly of salaried jobs in the private sector, was noteworthy.

—Aníbal Alarcón

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.