- Colombia: The current account deficit remains low and is struggling to find traditional financing sources; Diego Guevara is Colombia's new Minister of Finance after Bonilla's resignation; Exports rise as non-traditional exports gain ground

COLOMBIA: THE CURRENT ACCOUNT DEFICIT REMAINS LOW AND IS STRUGGLING TO FIND TRADITIONAL FINANCING SOURCES

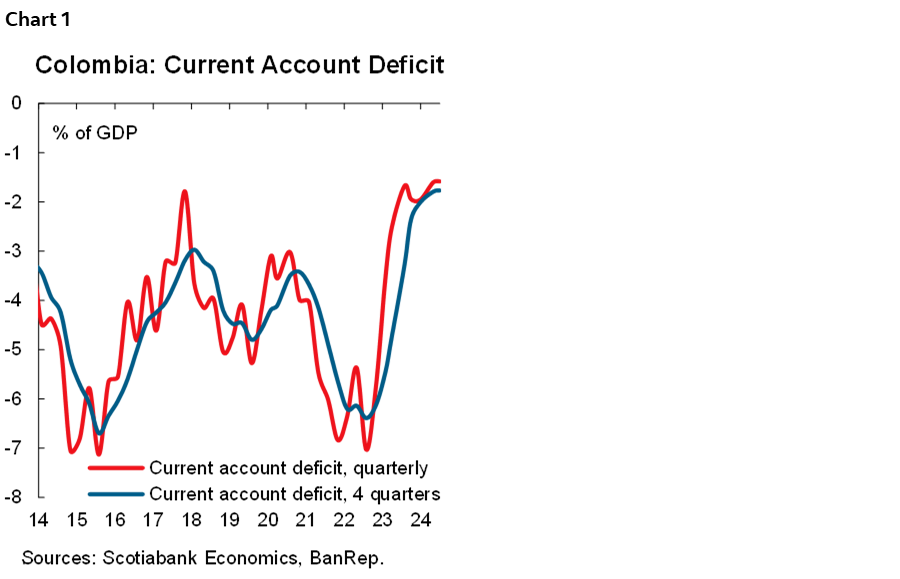

On Monday, December 2nd, the central bank (BanRep) released the Q3-2024 Balance of Payments (BoP). The current account deficit stood at USD $1.63 bn, equivalent to 1.6% of GDP, close to the narrowest levels since 2009 (chart 1). The overall picture shows that Colombia passes the worst in terms of economic deceleration; however, it still suggests that the recovery is not gaining significant momentum. The most interesting part is that despite the current account deficit being low, the traditional sources of financing (net FDI and net portfolio investments) are more challenging to find. The funding relies more on other sources, such as credit from the private sector and the reduction of assets in foreign currency from the public sector, complemented by purchases in international reserves. This structure on international accounts, coupled with a noisy fiscal context, points to structural forces that favour FX volatility and reduce the probability of a significant appreciation of the COP in the medium term.

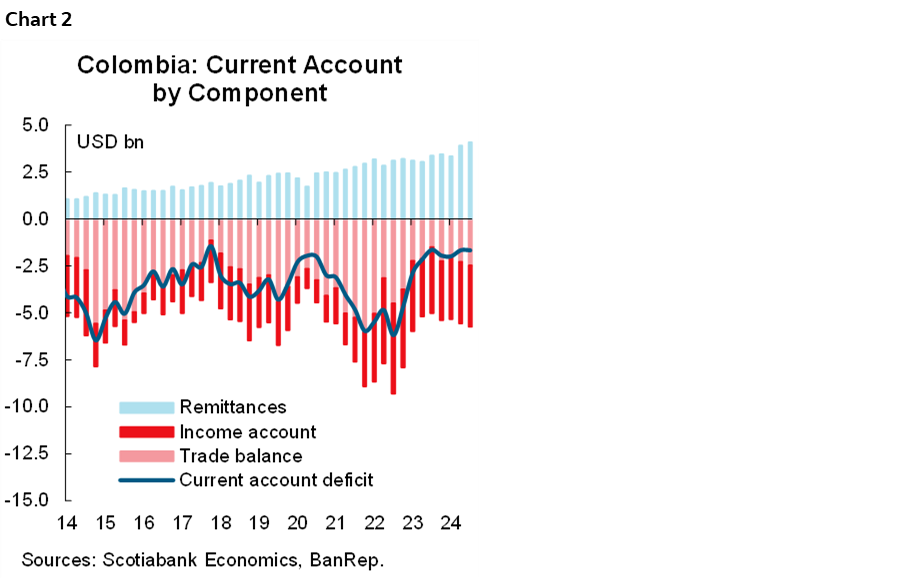

Regarding the BoP structure, the current account deficit remains low, reflecting mixed forces. On the positive side, remittance inflows are helping, but on the negative side, lower income account outflows and a widening trade deficit via deterioration of exports suggest that the overall economy remains weak. The previous composition is reflected in the financing account, FDI weakens while portfolio investments represent net outflows in the quarter. So, the task of accumulating international reserves has been important to have a buffer to respond in case of potential external shocks.

In the YTD up to the third quarter of 2024, the current account deficit stood at USD $5.33 bn, representing 1.7% of GDP and a weak picture compared to what was observed one year ago. Regarding monetary policy, the BoP suggests that economic activity has stopped slowing down but remains in a negative output gap. One year ago, the low current account deficit triggered the vote for the first cut in the cycle against economist consensus. This year the current account deficit number could support an acceleration in the easing cycle; however, the fiscal concern and the FX depreciation will tilt the vote towards a continuation in prudent 50bps rate cuts. At Scotiabank Colpatria, we project an interest rate closing 2024 at 9.25% and 6.75% for Dec-2025. In terms of the current account, the deficit is expected to represent less than 2% of GDP. However, the financing gap will lead the FX to at least maintain current levels.

Further details about the balance of payments numbers:

Current account:

In Q3-2024, the current account deficit stood at USD $1.67 bn (1.6% of GDP, chart 2), very similar to the previous quarter’s and previous year’s deficit (~USD $1.67bn and USD $1.65 bn, respectively). In the YTD, the deficit was USD $5.33 bn (1.7% of GDP), which was 20% lower than in 2023. The income account is the main source of the deficit (USD $9.88 bn), and the main offset force is transfers (USD $11.3 bn), in which remittances account for most of that. In the trade balance, the deficit is widening from USD $5.87 bn one year ago to USD $6.75 bn in Jan–Sept of 2024. The deterioration is for a bad reason: a weakening of exports in the context of deteriorated terms of trade.

- Trade balance of goods: In the YTD up to September, the trade deficit in goods was USD $6.43 bn. Exports contracted by 4.2% y/y, mainly on lower coal and oil exports, which offset the better performance of some agricultural and industrial products. In the case of imports, in the YTD, it stood at USD $44.3 bn (-0.4% y/y); the contraction is explained by lower imports of transport equipment and agricultural inputs, while consumption products are picking up by 7.3%, a composition that is even more challenging for the financing side.

- The trade balance of services in the YTD had a deficit of USD $319 m. The most dynamic part of exports is still in tourism-related flows, in terms of exports of services the balance has been good, while imports are also increasing.

- Income account: The income account also reflects the weak performance of economic activity. During the YTD up to September, the income account deficit stood at USD $17.26 bn, lower by USD $413 m compared to the deficit in the same period of 2023, which reflects lower earnings for foreign firms. In fact, earnings represent 42.5% of total outflows while interest payments represent 30.7%; the former is the one that increases the most, suggesting that the current account’s widening source is more explained for the “higher for longer” international scenario.

- Transfers: Transfers continued contributing to a lower current account deficit. Net inflows in the YTD were USD $11.30 bn; remittances are at USD $8.68 bn, increasing by 17.2% and representing 2.8% of GDP and 12.3% of current inflows of the BoP. Remittances are an important part of the macro stability in some regions, and we have to keep an eye on the US policies to assess a potential impact in 2025.

Financing side:

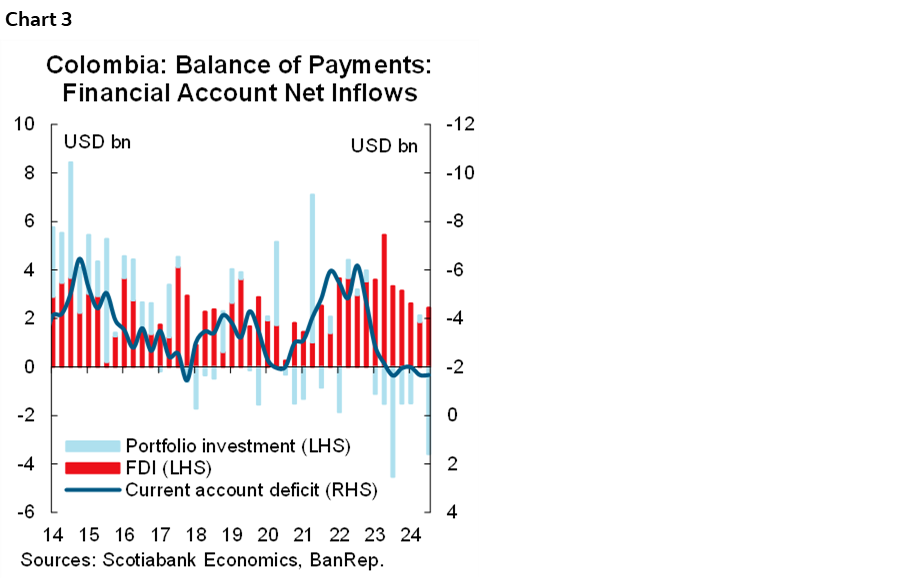

The financial account registered net inflows of USD $3.519 bn (1.1% of GDP), including the IR accumulation of USD $2.91 bn made by the central bank (chart 3).

- Foreign Direct Investment: FDI gross inflows stood at USD $9.95 bn in the YTD, falling 25.4% y/y. The main destinations were oil and mining (31%), financial services (24%), and manufacturing (17%). However, we identify that, at least in the case of financial services, inflows are related to capitalizations, maybe to support the sector’s losses rather than to expand capacity.

- Portfolio investments: Total inflows stood at USD $1bn, a very low amount but similar to what was observed one year ago, suggesting that the appetite from foreign investors for Colombian assets remains weak. On the other hand, investment from domestic investors in foreign markets is at a high level of USD $2.5 bn, putting further pressure on the FX.

DIEGO GUEVARA IS COLOMBIA’S NEW MINISTER OF FINANCE AFTER BONILLA’S RESIGNATION

Yesterday, President Gustavo Petro asked Ricardo Bonilla to resign from his position as Finance Minister as a result of his involvement in an investigation into the irregular distribution of resources from the public disaster fund. Bonilla confirmed his resignation on Wednesday afternoon, and after that, Diego Guevara was named the new Finance Minister.

Diego Guevara has been in the Finance Ministry since the beginning of Petro’s government and prior to being named Minister he was the General Vice-minister, which will ensure a smooth transition in leadership. Minister Guevara has a Ph.D. in Economics from the most recognized public university in Colombia, Universidad Nacional de Colombia, and his main experience before being part of the Min Fin team was mainly on the academic front.

During his academic experience, he was recognized as being interested in heterodox macroeconomic theories and, in the political environment, collaborated in annual minimum wage negotiations in technical studies for labour unions. Given this background, we highlighted that Guevara has been pragmatic during his time in the Finance Ministry and has demonstrated a strong interest in preserving macroeconomic stability while respecting the current institutional framework.

All in all, our take is positive regarding the appointment; however, we recognize that the fiscal context is challenging. Minister Guevara has said that Colombia is at the edge of the knife in terms of compliance with fiscal rule emphasizing that the fiscal strategy has been implementing spending cuts coupling the shortfall of fiscal income. However, the challenge will continue in 2025. Just this month, Minister Guevara must lead the discussion of the Financing Law that is expected to rise COP 12 tn (~0.8% of GDP) in fresh fiscal income sources. Additionally, he should be aware of the minimum wage negotiation, a critical parameter for the fiscal budget.

Another fiscal milestone will be the Financing Plan for 2025, which will show how the Government will manoeuvre markets pursuing funding sources next year. In that regard, we highlighted that yesterday’s green bonds auction was weak, probably penalizing the lack of liquidity in this reference since its inception.

Minister Guevara will also participate as president of the BanRep’s board in December; we expect him to continue favouring a 75bps rate cut. In our opinion, Guevara was a natural candidate for BanRep’s board for potential replacements that will take place in February 2025. However, his leadership in the Finance Ministry takes him out of this possibility.

As we mentioned before, Guevara has participated in the Finance Ministry since the beginning of Gustavo Petro’s mandate, which is a strong signal of continuity, and we expect he will continue showing a strong commitment to compliance with the fiscal rule, which could moderate potential volatility in COLTES and FX markets.

—Jackeline Piraján

EXPORTS RISE AS NON-TRADITIONAL EXPORTS GAIN GROUND

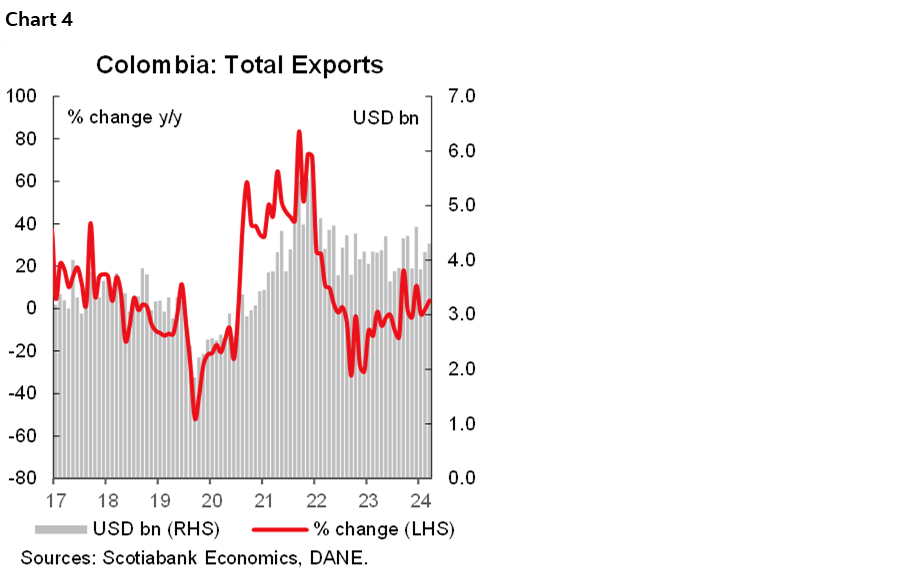

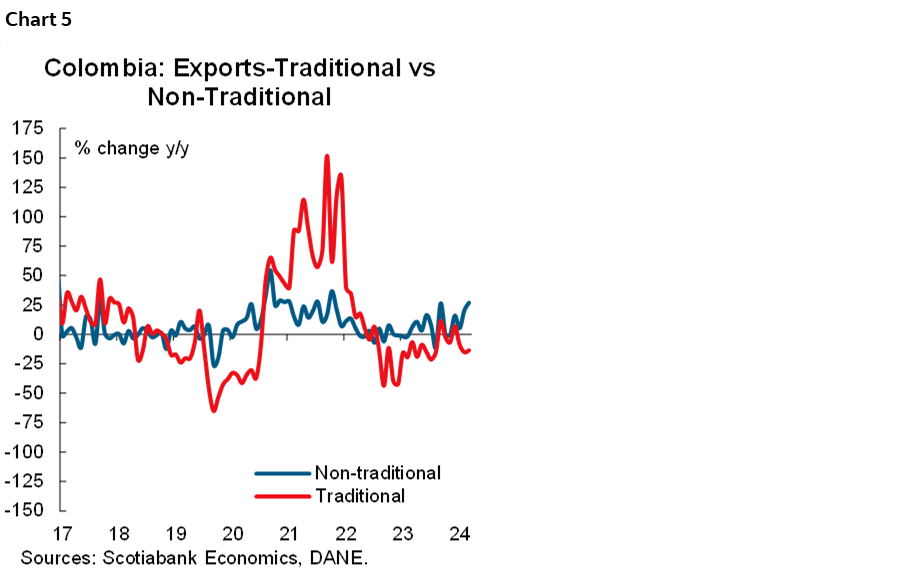

DANE published export data on Wednesday, December 4th. Monthly exports in October stood at USD $4.31 bn FOB, registering an increase of 3.8% compared to October 2023 (chart 4), returning to a positive trend after having registered declines in the previous two months. Compared to last month, total exports registered an increase of 3.7%. In general, non-traditional exports are gaining a share, while international oil prices and a lower exported volume of coal offset the result.

The share of non-traditional exports in October represented 52% of total exports, an increase of 9% compared to the share they had in October 2023. Two components largely explain the behaviour of non-traditional exports: one associated with the boom in the agricultural sector and the second with a growing export of non-monetary gold, which in October contributed 5.8 ppts to the total.

- Traditional exports registered a contraction of -13.48% due to less favourable fuel prices. The volume of oil exported remains relatively stable, however, there is evidence of a contraction of -20.21% y/y in terms of billing, associated with a lower oil price, since in October 2023 it was around $88 USD/b and in October of this year it averaged $75 USD/b, becoming a factor against the exchange rate given a lower inflow of flows by a sector that represents about 30% of total exports. On the positive side, coffee exports maintain a good dynamic favoured by a higher international price, registering a growth of 82% y/y.

- Non-traditional exports reached historical highs reaching US $2.25 bn FOB. In October, non-traditional exports increased 26.9% compared to October 2023, driven by a good performance in food products (excluding coffee), which grew 17.7% y/y, where fruits and some animal products stand out. Additionally, exporting of manufactured goods increased by 7.8% y/y, reflecting the good economic performance of the chemical industry. Finally, the exporting of non-monetary gold, which represents 11% of total exports, increased 92.4% y/y, reaching USD $503 m FOB (chart 5).

—Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.