- Colombia: Monetary policy views

- Peru: New data point to a weak GDP number for June

COLOMBIA: MONETARY POLICY VIEWS

Central banks continue to be in the spotlight across the world. The Fed is finally expected to start its easing cycle at its September 2024 decision, the BoC, BoE, and ECB have already started, and Latam countries are in the midst of policy rate normalization. However, uncertainty around the timing and the pace of the easing cycle is rising and economic surprises are driving significant volatility across markets as each piece of information contributes to model expectations about whether the economy, especially the US’s is facing a soft, hard, or no landing. What is true is that the main topic of conversation is around monetary policy rates.

In Colombia, BanRep has shown that graduality and patience in the policy rate normalization is the necessary strategy given elevated uncertainty in domestic and international inflation, while market volatility has resulted in unusual FX volatility. The recent Monetary Policy Report, with information up to May, ratifies the graduality approach, however things can change quickly, the most recent example was the US employment data that brought into the conversation the possibility of having a more aggressive Fed easing cycle. In Colombia, we had our own episode of unexpected deterioration in the labour market: in June nationwide unemployment jumped by 1ppts to 10.3% with employment destruction at the margin of 131 thousand y/y (-43 thousand in S.A. terms). Thus, is it possible that the new data can trigger a more aggressive path for BanRep’s easing cycle?

The next BanRep meeting will be on September 30th, while the Fed’s meeting is on September 18th, which can bring some easing to BanRep’s board to increase the speed of the easing cycle if the Fed confirms the dovish tone due to weaker economic activity in the US. On the domestic front, services data is already showing a weaker performance, in fact, in June the services sector destroyed 177k employments y/y, implying that tertiary sectors are no longer boosting Colombian economic activity, which also would help core inflation to decelerate faster. Additionally, inflation expectations measured by analysts’ surveys and BEIs put headline inflation within the target range by June next year, dissipating somehow, credibility issues that for now, are the main concern for the majority of BanRep.

Of course data will be key and Colombia will have a lot of it before BanRep’s board decides again. We will have July and August inflation, Q2-2024 GDP growth on August 15th , and July and August labour data. According to our expectations, headline inflation in August will be 6.4% while core inflation will be 5.9%, and although Q2-2024 GDP will show a relatively good growth of 3%, it is going to be rather temporary due to one-timers such as better-than-expected coffee crops this years, statistical base effects on the public sector, and extraordinary electricity production through thermos amid “El Niño” weather phenomenon. Additionally, we will continue to see a lack in the investment part of the economy and a continued weakness in private consumption. All in all, we do see that external and domestic inflation and economic activity data will support an acceleration in the easing cycle path from BanRep by the September meeting, ending 2024 at 8.5% as the monetary policy rate.

—Sergio Olarte & Jackeline Piraján

PERU: NEW DATA POINT TO A WEAK GDP NUMBER FOR JUNE

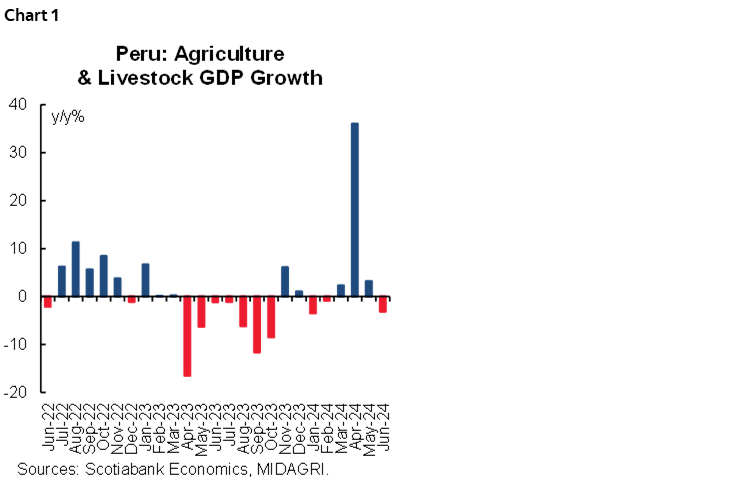

Early sector information for June GDP just keeps getting worse. Agriculture GDP figures for June were released this week, showing a 3.1% y/y decline. This throws our forecast of 2.0% y/y growth for June off track. We now expect something closer to 1.0%. Still positive, but quite a distance from the +5.0% growth of April–May. The decline in growth involved both products for domestic demand and agro-industrial goods. There is a chance that the volatility that we are seeing in agriculture this year (chart 1) reflects the volatile impact of El Niño on the sector last year, especially in terms of generating year-to-year changes in the growth and harvest timing. This volatility may persist for a few months still.

The weak June agriculture growth number adds to other weak early indicators, as stated last week: mining GDP fell 8.1% y/y, in June; cement demand was down 5%, and while fishing (+57%) and public investment (+9%) were both positive, they were much lower than the triple-digit growth figures in fishing and double-digit in public investment, of previous months. In addition, this year there was one day less in June than in 2023, due to a new holiday, although the impact of this should be rather marginal.

There is not much hope that domestic demand sectors will pick up the slack, considering that electricity growth was very weak, 0.6% y/y, in June. July may be better, however, if only because pension fund withdrawals began in late June, and should help bolster consumption to some extent starting in July. There is, therefore, no need to revise our full year GDP growth figure of 3.0%.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.