- Colombia: Inflation continued decreasing; however, it is insufficient to trigger an acceleration in the monetary policy easing cycle

A quiet start to the week in the G10 contrasts with a busy first half of the week in Latam. The weekend and the overnight session were absent of broad market drivers—aside from swings in commodity prices—but USTs are continuing their post-NFP selloff in Asia (Chinese markets reopened after a two-day holiday). A bare US data day ahead awaits, but we’ll keep an eye on appearances by the Fed’s Goolsbee and Kashkari.

A 3-4bps yields increase across the UST curve overnight has spread to EGBs and gilts, but is having limited impact on overall risk sentiment as USD gains and losses are mostly confined to +/-0.2% ranges and US equity futures sit little changed. A quiet weekend in the Middle East translated into a sharp drop at the open in crude oil prices, but these have come back from intraday lows to show a more modest ~0.5% decline since Friday. In the metals space, the return of Chinese traders and a decline in local steel inventories have iron ore surging 6%, but copper is managing ‘only’ a 1% gain.

With a quiet offshore data and events backdrop, Latam markets should then have little from abroad to drive local price action, but domestic calendars will pay close attention to March CPI releases. Friday’s post-market Colombian CPI data (see below) is followed by Chile’s own prices figures in just a couple of hours, and Mexico’s and Brazil’s at 8ET on Tuesday and Wednesday, respectively. With Colombian inflation roughly in line with expectations, there may be only a small reaction in local markets at the open—and the continued US rates selloff may play a bigger role.

For today’s Chilean CPI data, our economists project inflation accelerated slightly in March to print a 0.7% m/m increase in prices (translated into a non-chained 3.5% y/y) owing to transportation, educational services, and housing prices that would account for 0.6ppts of the 0.7ppt rise for the month. Within transportation, it will be higher fuel prices and airfares that will drive most of the rise in prices of the overall category. The weaker CLP has been a headache for BCCh officials, as the positioning of markets for sharp rate cuts led a depreciatory narrowing of Chile’s rate differential to the US—but also regional peers. A strong print today may see markets start to weigh more heavily the chance of a 25bps rate cut by the BCCh at its May meeting, though we think the bank will opt for the larger half-point reduction.

—Juan Manuel Herrera

COLOMBIA: INFLATION CONTINUED DECREASING; HOWEVER, IT IS INSUFFICIENT TO TRIGGER AN ACCELERATION IN THE MONETARY POLICY EASING CYCLE

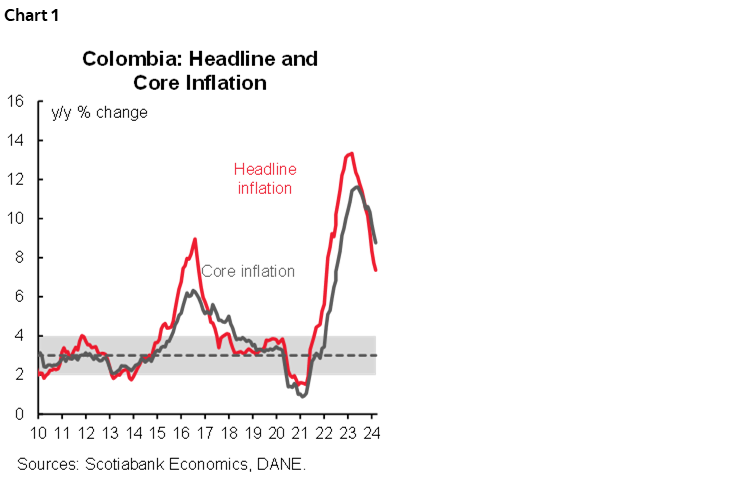

Monthly CPI inflation in Colombia stood at 0.70% m/m in March, according to DANE data released on Friday, April 5th. The result was above economists’ expectations of 0.64% m/m, according to BanRep’s survey and closer to Scotiabank Colpatria’s expectation of 0.71% m/m. Annual headline inflation continued slowing down from 7.74% to 7.36%, the lowest level since January 2022 (chart 1). Core inflation (ex-food) decreased from 9.20% y/y in February 2024 to 8.76% y/y in March, while inflation excluding food and energy went down by 50bps to 6.77% y/y. Although inflation cumulated a 598bps reduction since its peak, we now don’t expect the central bank to accelerate the easing cycle since concerns around the political scenario could continue affirming the cautious approach from the majority of the board due to a possible significant spike in the country’s risk premium that can bring back a sharp FX depreciation and affect durable goods prices. That said, we expect a 50bps rate cut at April's meeting (April 30th).

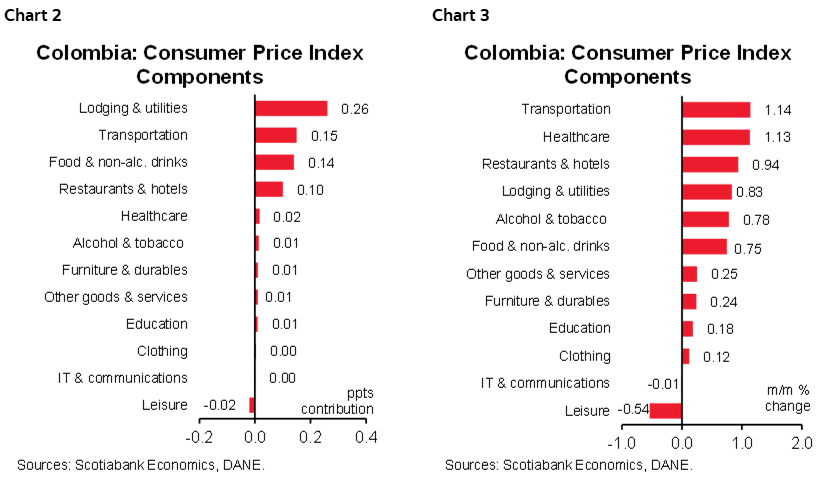

During March, three groups accounted for 55% of monthly inflation (charts 2 and 3). Lodging and utilities group is once again the main contributor with a monthly inflation of 0.83% m/m and 26bps of contribution, which reflects mainly the effect of indexation in rent fees and increments in utilities, especially gas prices. The transport group contributed 15bps due to increases in public transport systems, while food, fruits, and vegetables continued with an upward price trend.

In annual terms, most of the groups continued with a disinflationary trend, however, rent fees are still trending up as indexation is higher than anticipated, something that we could attribute to a deficit in the housing supply deepened due to the lack of construction in a context of high-interest rates and higher demand for renting houses given high-interest rates that do not allow households to buy homes. In the case of utility fees, monthly inflation remains under control, but we expect a rebound in forthcoming months, especially in electricity due to the thermoelectric generation that is used in response to the “El Niño” weather phenomenon and its impact on the level of reservoirs.

In terms of goods and services inflation, we continue seeing mixed progress. Goods-related inflation decreased from 4.32% to 3.08%, technically achieving the inflation target, but explained mainly by the disinflation of tradable goods due to the low demand and the FX appreciation. In the case of services, the picture is still challenging. Inflation decreased from 8.47% to 8.28%, still well above the target for the central bank but affected mainly by the indexation in key prices such as rent fees.

All in all, today’s results would not be enough to convince the cautious side of BanRep’s board. Instead, we think they will continue the easing cycle at a 50bps pace with a split vote, like March’s meeting. It is worth noting that in April’s monetary policy meeting, the board will have a fresh set of forecasts from the economic staff, and in that sense, it will be important to know how the risk balance has changed, given the significant improvement in inflation and the weaker than expected performance in the economic growth.

Finally, it is also worth noting that since April, the disinflationary force will moderate. In the case of food inflation, the tailwind from the statistical base effect will vanish, which could mark a rebound in the annual inflation of food. Our preliminary calculation points to an annual inflation still above 7% in April and a reduction below 6% in Q4-2024. Our forecast is compatible with the central bank’s guidance about achieving the target range by mid-2025.

Other highlights:

- Lodging and utilities group contributed 26bps to headline inflation. Rent fees are showing a stronger indexation than the previous year, something we attribute to supply issues amid the huge deceleration in housing construction. In the case of utility fees, this month’s gas leads to price increases; however, in the future, we expect to see a higher upside pressure in electricity due to the impact of the “El Niño” phenomenon.

- The transport group was the second main contributor (+1.14% m/m and a contribution of 15bps). Regulated prices of the public transport system in Bogota and other cities explained the rebound, while in the case of tradable goods, such as vehicles, they continue going down (-0.43% m/m), cumulating more of a 5% price reduction since July 2023, previous behaviour is strongly related with the FX appreciation but also with weak household demand.

- Food inflation was 0.75% m/m, contributing 14bps. Monthly food inflation remains high, but under control in annual terms (1.73% y/y). Fresh fruits are still pointing north (+7.58% m/m), followed by plantains (+3.58% m/m), potatoes (+2.27% m/m), and vegetables and legumes (+2.70% m/m). Despite monthly food inflation being above the historical average, statistical base effects have contributed to the disinflation. Since April, we won’t have this tailwind since food inflation in April 2023 was negative (-0.07% m/m), which suggests that the disinflationary trend will moderate in forthcoming months.

- The restaurant and hotel group contributed 10bps to headline inflation (+0.94% m/m). This group also reflects indexation but especially the minimum wage since it is a labour-intensive sector. However, it is important to note that despite the price increase in this group being almost mandatory, the economic performance has been deteriorating, which poses a dilemma between what prices dynamics are reflecting and the financial performance of the sector. Again, previous issues could not be enough to trigger a more aggressive action from the central bank in the easing cycle.

—Sergio Olarte, Jackeline Piraján & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.