- Colombia: Despite an increase in sales volumes, exports were negative in February

- Mexico: Banxico meeting minutes showed caution; we expect a pause in May

COLOMBIA: DESPITE AN INCREASE IN SALES VOLUMES, EXPORTS WERE NEGATIVE IN FEBRUARY

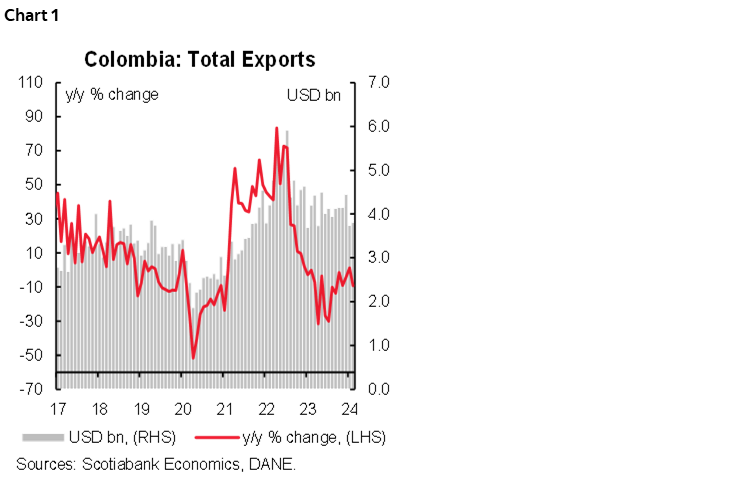

The National Statistics Institute (DANE) published export data on Thursday, April 4th. Monthly exports in February 2024 amounted to USD 3.81 billion FOB, with a decrease of 10.1% y/y (chart 1). This result marks the lowest level of exports in February since 2021. In terms of volume, there was an expansion of 3.5% y/y to 8.57 million tons in February 2024, compared to 8.28 million tons in the same month in 2023.

This result was due to a 23.4% y/y drop in February external sales of fuels and products of extractive industries, which amounted to USD 1.82 billion FOB and contributed negatively to the variation by -13.1 p.p. This was mainly due to the fall in sales of coal, coke, and briquettes (-35.9% y/y), which contributed -14.9 p.p. to the variation of the group. In terms of volume, the fuel group exported a total of 7.8 million metric tons showing an expansion of 1.9% y/y and a contribution of 1.8 p.p. to the variation explained by an increase in the production of coal, coke, and briquettes from 4.7 million tons in February 2023 to 5.3 million tons in 2024 (+13.3% y/y and 7.5 p.p.), while the oil and its derivatives component offset a decrease in volumes to 2.3 million tons from 2.8 million tons in February 2023 (-18.4% y/y and -6.4 p.p.).

On the other hand, external sales of agricultural products, food, and beverages amounted to USD 963.5 million FOB and showed a growth of 13.1% y/y compared to February 2023, along with a positive contribution of 2.6 p.p. to the variation. This behaviour was mainly explained by the increase in exports of bananas (including plantains) fresh or dried (79.2% y/y) and cut flowers and foliage (13.2% y/y), together contributed 8.9 p.p. to the group’s variation. In terms of volume, the agricultural products, food, and beverages group grew by 33.6% y/y and contributed 1.5 p.p. (490,938 metric tons).

In line with the positive behaviour of exports of agro-food products, exports of the manufacturing group were USD 796.2 million FOB and expanded by 3.5% y/y compared to February 2023, with a contribution of 0.6 p.p. to the total variation. This behaviour was mainly explained by the growth in external sales of machinery and transport equipment (37.1% y/y) and chemicals and related products (7.9%), which together contributed 8.4 p.p. to the group’s variation. In terms of volume, there was an annual growth from 244,429 tons in February 2023 to 268,589 tons in February 2024 (+9.9% y/y and 0.3 p.p.).

On the other hand, in February 2023, the group “other sectors” decreased by 4.7% year-on-year (USD 234.2 million and a contribution of -0.3 p.p. to the variation), mainly explained by the decrease in exports of non-monetary gold, which contributed negatively with 4.0 p.p. to the variation of the group.

In terms of participation, in February 2023, the reference month, exports of fuels and products of extractive industries participated with 47.7% of the total FOB value of exports; likewise, manufacturing with 20.9%, agriculture, food, and beverages with 25.3% and other sectors with 6.1%.

In fact, YTD Colombian exports amounted to USD 7.43 billion FOB and recorded a decrease of 6.8% compared to the same period in 2023, mainly due to a decrease of 17.6% y/y and -9.8 p.p. in the exports of the group of fuels and products of extractive industries (USD 3.7 billion FOB).

Despite the improvement in global financial conditions, exports are expected to show a weak performance in 2024 due to the fall in international prices of commodities such as coal, oil, and coffee, as already observed in the February results. Imports will continue to decline, albeit at a slower pace of imported intermediate goods to replenish stocks is expected to improve in a context of moderate economic growth and falling international prices of basic products. However, the widening of the current account deficit will be limited by the continued dynamism of tourism exports, the normalization of freight, the decline in the benefits of some foreign direct investment companies, and the high level of workers’ remittances, in a context of lower inflation and a moderate cycle of interest rate cuts.

Key Highlights:

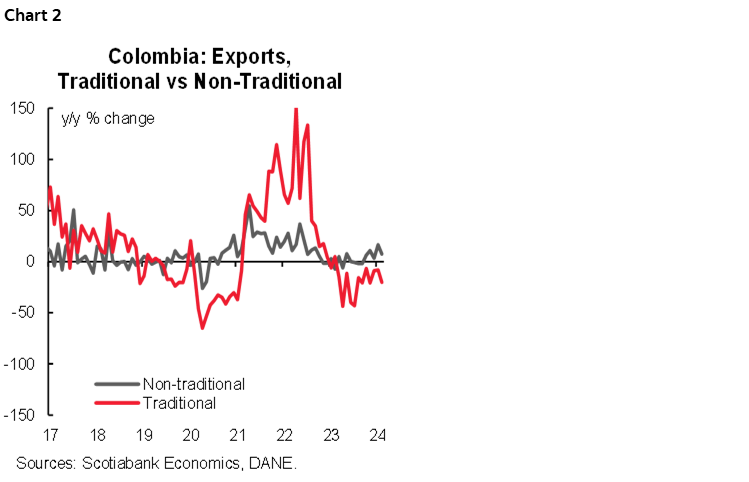

- Traditional exports (related to coffee, oil, and mining) declined in value but recovered in volume. In February, traditional exports amounted to USD 2.0 billion FOB, a decline of -21.4% y/y, in contrast to the 7.7 million tons exported, whose growth was 1.3% y/y.

- Among the components of traditional exports, petroleum and its derivatives declined by 14% y/y in February (USD 1.1 billion FOB). This was followed by coal exports, which fell by 35.9% y/y in February (USD 632.5 million), and coffee exports, which fell by 1.3% y/y (USD 246.8 million).

- In terms of volume, external sales of oil and its derivatives fell by 18.4% y/y in February (2.4 million tons). As for coal exports, they recorded an expansion of 13.3% y/y in February (5.3 million tons), while coffee exports abroad increased by 11.2% y/y in February (~49 thousand tons).

On the other hand, non-traditional exports reached USD 1.8 billion in February 2023, recording a growth of 29.8% y/y (chart 2). In addition, in terms of volume, non-traditional exports reached 838,693 metric tons (+29.8% y/y vs. February 2023).

—Sergio Olarte & Santiago Moreno

MEXICO: BANXICO MEETING MINUTES SHOWED CAUTION; WE EXPECT A PAUSE IN MAY

The minutes of Banxico’s March meeting revealed the arguments behind the votes for a rate cut, and in the case of Deputy Governor Espinosa, the arguments for leaving the rate unchanged. In general, it seems that one of the main arguments of the members who voted for the cut was the increase in the ex-ante rate to a level close to 7.50% due to the decline in one-year inflation expectations. The ex-ante rate is calculated from inflation expectations, and the current interest rate, so by holding the target rate unchanged, the ex-ante rate should rise when inflation expectations fall. Another argument used by some of the members was that, although the inflationary outlook remains uncertain and with an upward balance of risks, some shocks have begun to be mitigated and the disinflation process has progressed since the rate has stood in restrictive territory.

On the other hand, Deputy Governor Espinosa communicated in her dissident vote that “monetary policy has had to face additional challenges, such as pressures from wage increases and an expansionary fiscal policy, to steer inflation towards the 3% target.” In addition, she considered it was premature to start reducing the monetary restriction amid higher private analysts’ inflation forecasts higher than those released by Banxico, underlining that it would put at risk Banxico’s credibility regarding its commitment to the price stability mandate.

Another member of the Governing Board considered that “it is still not time to begin a rate cutting cycle. However, he/she expressed that there is some room for an isolated fine-tuning in order to maintain a restrictive, but not overly restrictive, monetary policy stance.” This same member stated that a restrictive, elevated and lasting monetary policy stance is required. Comments from several other members also pointed to a longer, paused and data-dependent cutting cycle.

Regarding the inflation outlook, the Board members took into account data up to February, when a slight increase in core inflation was observed, although the figures of the second fortnight core component repeated an annual increase, surprising to the upside. In this regard, the Governing Board inflation forecasts have been modified upwards on several occasions throughout this restrictive period and continuously remain below the forecasts of private sector analysts.

We distinguished some concern from the members of the Board of Governors about the current inflation outlook, as well as the expectations of private sector analysts. In addition, given the uncertainty surrounding inflation and the recent rebound in the core component, we believe that the Board will leave the rate unchanged at the next monetary policy meeting with gradual adjustments during the year, raising our year-end rate outlook to 10.0%.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.