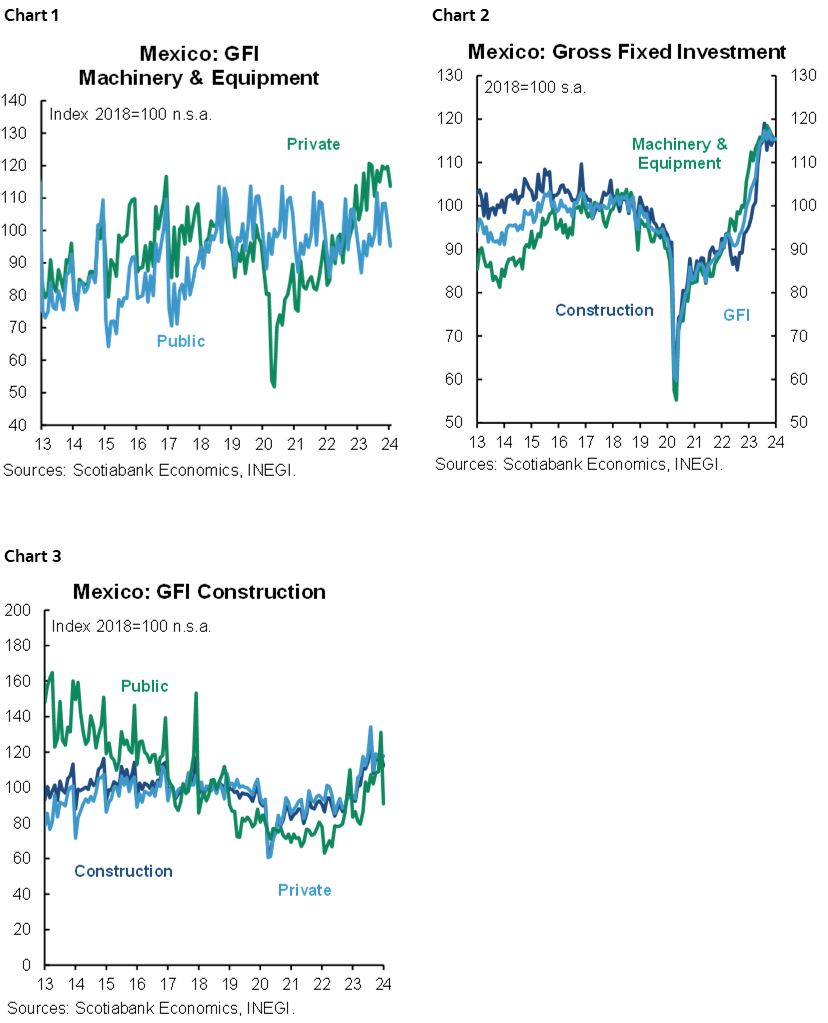

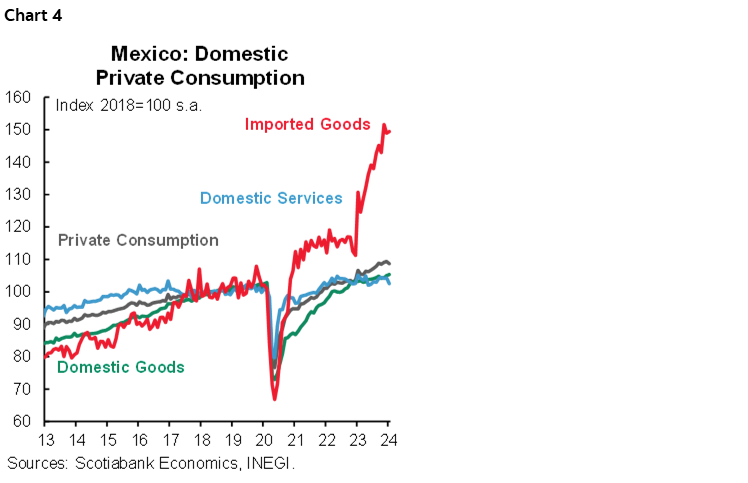

- Mexico: GFI showed a strong annual advance in January despite a stagnant monthly pace; consumption slowdown in January on weak domestic goods consumption, while imported goods purchases remain strong

It’s the quietest day of the global week, giving markets a breather ahead of the release of US NFP tomorrow. With Chinese and Hong Kong markets closed, and no major data in APac, a sizable miss in Swiss headline and core inflation data was the overnight highlight. The release has triggered a half-percent decline in the CHF that is the only major losing ground against the USD today; with antipodean and high-beta FX leading, though the MXN sits flat.

European equities are up 0.2–0.4% in the major indices in line with gains in US equity futures. Crude oil prices are little changed, in contrast to a nice 1.3% rally in copper opposite to a sharp 1.8% drop in iron ore on strong Aussie exports. The post-ISM services rally in USTs got an extra push from an uneventful Powell appearance after the UK close yesterday, but Asia markets practically erased all these gains and European hours are providing only a small bid amid a relatively heavy sovereign issuance slate. US Challenger job cuts at 7.30ET should come and go until the release of jobless claims an hour later followed by another round of Fed speakers—who may not offer much new.

Banxico’s meeting minutes at 11ET are today’s Latam highlight, offering the view of officials on their decision to begin rate cuts last month. With revisions higher to its headline and core inflation projections and a data-dependent mode, it seems likelier that Mexican officials will skip the upcoming decision, considering that “there remains challenges and risks that merit continuing a prudent management of monetary policy.” On politics, Sheinbaum adviser called state-owned oil company Pemex one of the “great black holes” for Mexican resources yesterday, suggesting that the leading candidate may take a more proactive approach in controlling the company’s finances.

Back to monetary policy, we got the BCCh’s updated projections in their quarterly MPR published yesterday, where the policy rate forecast were roughly aligned with market pricing by year-end, seeing a 5.00% level in December. Overall, there were no major surprises in the publication, which was followed by an appearance in Senate by BCCh Pres Costa that offered little of note aside from highlighting (again) that monetary policy risks are coming from abroad—namely CLP weakness. That aside, Chile’s economy is showing signs of improvement in early-2024 that could also back a slower pace of easing in coming meetings; markets expect a 50bps move in May followed by another shift lower to 25bps in June. Costa speaks again today at 7.30ET on the MPR.

In Peru, Congress voted through Boluarte’s cabinet nominees yesterday, but the President today faces a vote on whether to move ahead with two impeachment motions. Despite her high disapproval rating with citizens, this renewed impeachment effort is unlikely to succeed (again). The removal of the president needs a two-thirds majority to occur, but this vote would only take place if a lower 40% threshold is reached in today’s vote (which has not been reached in previous motions against Boluarte). Peru political noise continues while we remain of the view that the President will continue in her charge until the 2026 elections.

—Juan Manuel Herrera

MEXICO: GFI SHOWED A STRONG ANNUAL ADVANCE IN JANUARY DESPITE A STAGNANT MONTHLY PACE

During January, gross fixed investment accelerated on an annual basis, going from 13.4% to 15.3% y/y. Particularly, machinery and equipment rose 9.7% (5.0% previously), as the domestic subcomponent increased to 2.4% (0.0% previously), and the imported 15.2% (8.9% previously). On the other hand, construction had a smaller increase of 20.8% (21.8% previously), since non-residential construction slowed to 29.8% y/y (40.4% previously) and residential construction rose 10.1% (-0.4% previous). Despite strong annual figures, in the seasonally adjusted monthly data, the GFI remain stagnant at 0.1% m/m (0.0% previously), machinery and equipment fell -0.2% (-0.9% previously), and construction 0.3% (1.1% previously).

On the construction side, it summed nine months of consecutive double-digit increases, although this was the lowest print of them, partly owing to possible adjustments in demand, since a significant slowdown is observed in the public subcomponent with an increase of 9.0% y/y (19.1% previously), while the private sector remains more solid at 23.5% y/y (22.6% previously). These changes can also be attributed to the public infrastructure projects, that are expected to be finished before AMLO’s administration ends, so we expect smaller increases in the non-residential component.

Regarding machinery and equipment, despite having rebounded annually, it remains out of the sixteen month streak of double-digit advances that ended in December 2023. In line with this, the private subcomponent led the way, although it was slower compared to previous months, this time it increased +10.0% y/y, below the greater than 20.0% advances observed in 2023. Public investment is weaker in machinery and equipment, but positive, this time at 1.4% y/y (1.6% previously). This component could maintain a positive pace as economic activity remains solid, also favoured by access to credit as rates go down.

CONSUMPTION SLOWDOWN IN JANUARY ON WEAK DOMESTIC GOODS CONSUMPTION, WHILE IMPORTED GOODS PURCHASES REMAIN STRONG

Also in January, private consumption slowed in real annual terms, from 4.4% to 2.9% y/y as domestic goods dropped -1.0% y/y (0.3% previously), domestic services increased 2.3% y/y (1.6% previously), and imported goods decelerated 17.5% y/y (28.1% previously). However, in its seasonally adjusted monthly comparison, private consumption fell -0.6% m/m (0.2% previously), derived from a drop in domestic goods of -1.7% m/m.

The domestic side of the index decelerated to 0.5% y/y (0.9% previously), the drop in national goods is attributed to non-durable items, which decreased -3.0%, being the eleventh consecutive drop in this subcomponent. On the other hand, durable goods lead the advance in the national index, although they slowed to 7.9% (11.5% previously).

The consumption of imported goods also slowed but remains strong at 17.5% y/y (28.1% previously), owing to a significant slowdown in durable goods to 19.0% (47.9% previously), and in non-durable goods to 11.5% from 20.3% previously, although the semi-durable products accelerated to 30.6% (20.3% previously). This item has benefited from the appreciation of the Mexican peso, which is currently at similar levels to 2015 figures, so the acquisition of imported goods could remain strong as long as the appreciation of the peso persists.

January’s slower figures were somewhat signaled by monthly GDP proxy, which came out below consensus in the same month, and summed three consecutive months of sequential monthly decreases, although the growth outlook for 2024 remains strong. In the case of consumption, we believe that the strength of the labour market will foster a robust pace during the year. Furthermore, the increase in public spending in the first half of the year (particularly social spending) will also represent important support for household consumption. Finally, lower interest rates can benefit the acquisition of durable goods, giving a greater boost to demand during the year.

—Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.