- Peru: BCRP resumes cutting cycle; New car sales declined in March, with a negative impact on Q1-24 sales

PERU: BCRP RESUMES CUTTING CYCLE

The board of the Central Bank of Peru (BCRP) surprised and chose to cut its policy rate by 25bps, to 6.00%, when the market consensus and we expected another pause. Although the BCRP’s statement indicated that both local and global inflation are showing some resistance in their downtrend, it considers that these effects are transitory and that the decrease in inflation will continue throughout the year.

The statement has a more dovish tone by specifying that the BCRP expects inflation to converge not only into the 1–3% target range, but also specifies that it expects a gradual return to the center of the target range (2%) in coming months, highlighting that 12-month inflation expectations decreased slightly from 2.65% to 2.56%. The weakness of the impacts of the El Niño event and its early conclusion would also partly explain this position. The risks associated with climatic factors were no longer mentioned in the statement.

This assessment of local conditions would have counteracted the international factors that seemed to have taken a greater role in the March decision. Inflation is taking a long time to subside in the world and the US economy has been showing signs of strength in the labor market, putting upward pressure on interest rates in USD (which for a UST10 year term are close to 4.60%, the highest level in six months). This could delay the start of the Fed's rate cut cycle. The BCRP expects in its base scenario that the Fed will begin the rate cut cycle during the second half of the year.

The first readings for April inflation are favorable and suggest that inflation would be below the historical average (0.22%), making it likely that inflation will return to the target range (between 1% and 3%) relatively soon. These elements would have been implicitly validated by the BCRP, being sufficient to continue the cycle of rate cuts.

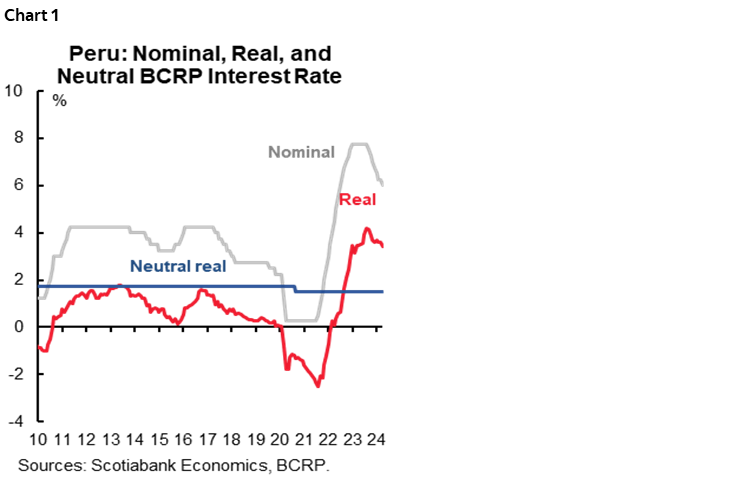

By cutting the reference interest rate to 6.00%, the real interest rate was reduced from 3.6% to 3.4%, still far from the 2.0% considered a neutral level, accumulating 20 months of contractionary territory (chart 1). The forward guidance remained unchanged, stating that “if necessary, it will consider additional modifications to monetary policy.” So far in 2024, monetary policy decisions are aligned with our vision, which is why we maintain our forecast of a rate of 4.25% by the year-end.

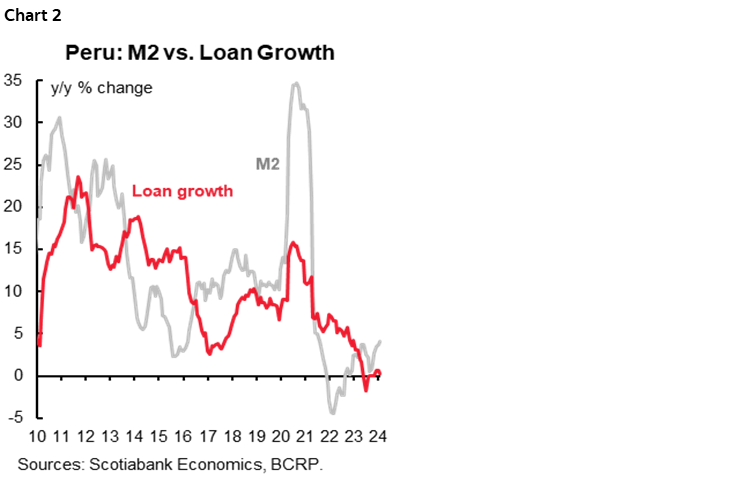

Our base case sees cuts of 25 basis points per meeting until Q4-24, when we expect a further pause once the real rate approaches the neutral 2% level. The main risk factor for now is the possibility of a delay in the Fed's rate cut cycle. The BCRP survey showed that the market maintained its key rate expectation for the year-end, at 4.50%, for the third time consecutive month. Monetary conditions showed a partial recovery in their latest reading. Liquidity accelerated its expansion in February (+2.3% y/y, for the fourth consecutive month), although loans does not take off (+0.3% y/y), see chart 2. Financial savings continue to accelerate (+8.2% y/y), for the ninth consecutive month; although its composition would change after Congress approved the seventh withdrawal of private pension funds.

—Mario Guerrero

PERU: NEW CAR SALES DECLINED IN MARCH, WITH A NEGATIVE IMPACT ON Q1-24 SALES

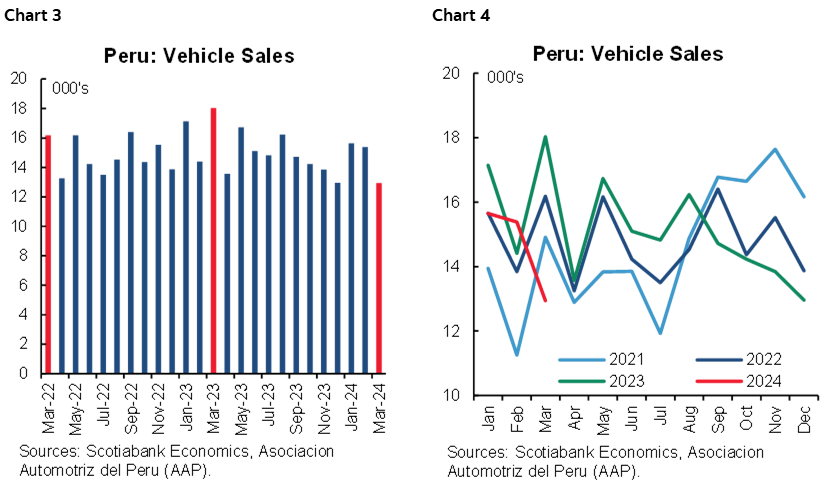

New car sales in March experienced a drop of 28% YoY. While this decline was within our expectations based on the high sales recorded in March 2023, which was also the highest monthly figure since January 2014, the magnitude of the drop was higher than we anticipated, with March 2024 sales being the lowest since July 2021.

The fall in sales can be attributed to the Easter holidays, which led to an increase in non-working days from four in March 2023 to eight in March 2024. We estimate that sales would have fallen by less than 20% in the absence of this effect. Additionally, greater seasonal spending on education due to the beginning of the school and college year, which usually takes place in March and typically competes with spending on cars, was higher than expected due to an increase in tuition. Moreover, Easter holiday travel expenses during March 2024, and which occurred in April 2023, limited the budget for new car purchases, especially in the light-vehicle segment.

New vehicle sales in Q1-23 fell by 11% YoY, primarily due to a 13% decline in light vehicles sales. This was not offset by an 8.4% YoY increase in sales of heavy-duty vehicles. However, we remain confident about the sales outlook in the coming months, particularly during 2H24, driven by a base effect, as 2H23 sales were the lowest in 2023. Moreover, the anticipated reduction of interest rates for vehicle purchases, following the gradual reduction of the central bank’s reference rate, could boost vehicle sales.

Despite lower-than-expected results for Q1-24, we are still confident in our growth outlook. Our 2024 forecast is now nearly 1%, with light-vehicle sales slightly higher than the previous year. Heavy-vehicle sales are expected to outpace the sector’s growth. Despite March’s challenges, we remain optimistic about the industry’s future and expect a rebound in the coming months.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.