- Chile: GDP grew 1.8% y/y in July (0.3% m/m), with a remarkable and broad sectoral expansion

- Peru: El Niño influences a lower pace of inflation deceleration in August

CHILE: GDP GREW 1.8% Y/Y IN JULY (0.3% M/M), WITH A REMARKABLE AND BROAD SECTORAL EXPANSION

- Strong July GDP growth would not prevent a fall of up to 0.5% of GDP this year

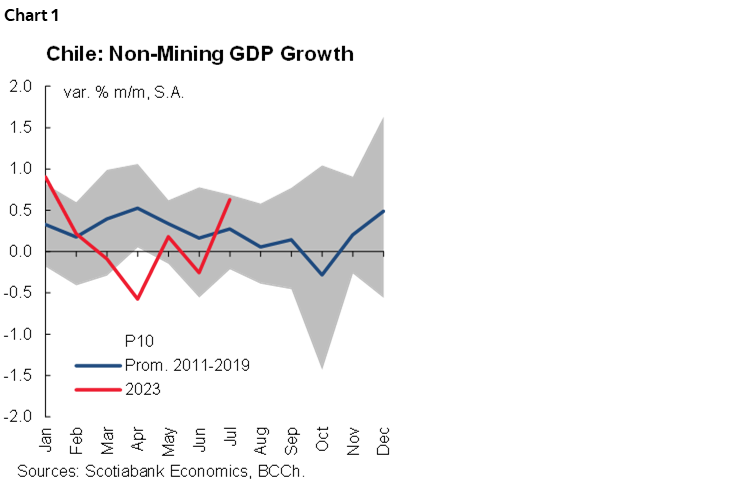

Well above our expectations and that of the consensus (Economists Survey: -0.3%; Bloomberg median: 0.8%), July GDP grew by 1.8% y/y (0.3% m/m), thanks to seasonally adjusted growth in the non-mining sectors (chart 1). This figure was robust enough to lead us to revise higher our 2023 forecast to a range between -0.5% and 0%, from -0.8% previously. Despite the better basis for comparison, this record shows genuine economic growth, as the services sector grew by a seasonally adjusted 0.3% m/m, as did industry (1.8%), commerce (1.4%) and other goods (1.7%).

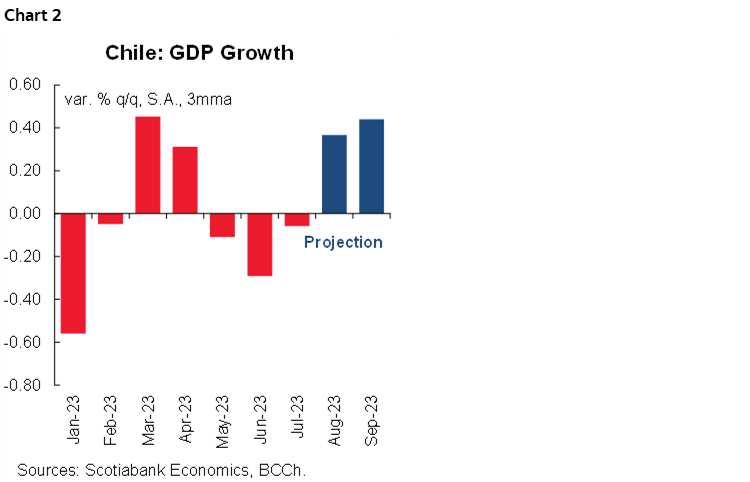

With this, it is very likely that we will see positive q/q growth in Q3-23, thus avoiding the technical recession we initially estimated (chart 2). However, we must be cautious, as August could again show a seasonally-adjusted contraction due to the impact of the floods in the south of the country.

Electricity generation continues to contribute to activity, although its contribution has an expiration date. Without minimizing the almost generalized growth at sector level, it is worth mentioning that electricity generation would be playing a very significant role in July’s GDP growth. Also taking into account the heavy rains in August, there is no doubt that power generation will contribute positively this year—more than other years—although its contribution to dynamism has an expiration date as long as there are no new weather events like the ones we have seen this winter. That is why we project that the contribution of this sector will decrease towards Q4.

The contribution of services to GDP growth in the rest of the year is not assured and will depend on the recovery of private investment. Services grew 0.3% m/m, thanks to the positive contribution of personal services, which would have been supported by the increase in health care services at the end of July. With data up to August, we did not observe a relevant increase in health care services, so the contribution of this sector to the economy’s performance would be moderate. In the coming months, business services could begin to prove supportive as private investment recovers. For now, the contribution of overall services for the rest of the year is not assured.

A positive surprise in commerce will be hard to repeat in the coming months. Commerce grew by a solid 1.4% m/m, both in wholesale and retail trade. This figure was the main surprise to our projection, which we attribute to greater dynamism in wholesale trade, mainly in machinery, equipment and materials. For August, we do not expect this high dynamism in commerce to be maintained, since high frequency indicators of purchases by Scotiabank and those published by the central bank continue to show declines in real consumption levels.

Looking ahead, assuming zero GDP growth between August and December, economic activity would contract by around 0.5% in 2023. Therefore, it will be key to determine the net effect that climate factors will have on activity in the coming months, as well as the impact of a possible recovery in private investment towards the end of this year. All in all, from August onwards we would again see negative y/y records for GDP growth.

Market Impact: July GDP growth provides strength to the June BCCh IPoM forecast (MPR) to be revised next week, where we expect an upward revision of 2023 GDP growth to the -0.25/0.25% range. The economy is starting to regain traction in its non-mining components relevant to the activity gap. In this context, the monetary policy strategy for the coming months is facilitated by support for the strength of the Chilean peso. The BCCh should discuss the alternatives of 75bps and 100bps cuts at its September 5 rate decision.

—Aníbal Alarcón

PERU: EL NIÑO INFLUENCES A LOWER PACE OF INFLATION DECELERATION IN AUGUST

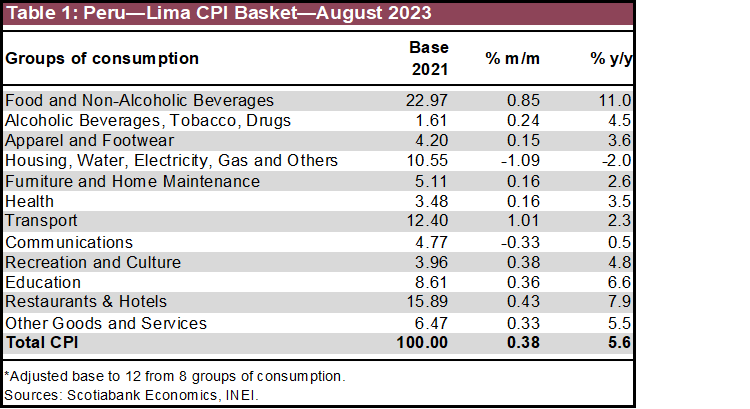

Inflation in August was surprising, since it was the same as in July, which is usually high due to seasonal factors. Lima’s CPI was +0.38% m/m in August, higher than the 0.30% forecast by Scotiabank, the 0.25% historical average (last 20 years), and higher than the 0.24% Bloomberg survey median. Despite this, year-on-year inflation continued to slow, going from 5.9% to 5.6%, in line with official expectations.

The surprise in inflation in August came from the rise in the prices of perishable foods, which offset the drop in poultry prices (-0.07ppts of contribution) and electricity prices (-0.11ppts). The effects of the strong coastal El Niño pushed up the price of lemons (+0.19ppts) and the drought in the south of the country pushed up the price of onions (+0.10ppts), together representing two thirds of inflation in the month. Adverse weather conditions have continued to affect the prices of some perishable products, mainly citrus fruits, and vegetables, since the number of roads with restricted traffic continued to increase, going from 24 in July to 42 in August, on average, consequences of the presence of the coastal El Niño, declared by the authorities since March, and of a global El Niño, declared since June.

The probabilities for the coastal and global El Niño for Q1-2024 have been increasing month by month, but the most worrying thing has been that until the previous reading, a weak/moderate scenario for the coastal El Niño was most likely. The latest reading sees a moderate/strong scenario more likely.

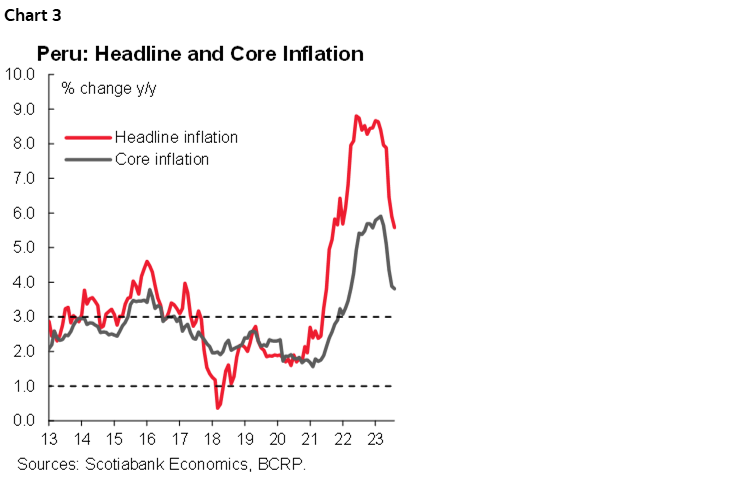

With inflation data for August, there have been 27 months in which inflation remains above the upper limit of 3% of the inflation target (table 1). Inflation at the national level (not only in Lima) went from 6.0% to 5.8%, exceeding inflation in Lima for 24 consecutive months. In August, of the 586 products that make up the consumer basket (base 2021), 338 increased (58%), 128 decreased (22%) and 120 remained unchanged (20%). This composition shows that the slowdown in inflation remains structurally slow. Core inflation rose 0.24%, deviating slightly upwards, after four months of being around its calendar month historical average. In interannual terms it went from 3.9% to 3.8%, slowing for the fifth consecutive month (chart 3). Cost pressures remained low, with year-on-year variations in negative territory, although they stopped falling, mainly due to the recovery of the FX rate. The PEN depreciated 3% on average in August.

Looking ahead, we expect inflation to continue to slow in September, although probably at a muted pace, since the increases in the prices of perishable foods in the final week of August would have an impact on September’s CPI. We maintain our inflation forecast of 5.0% for the end of 2023. The inflation data for August and the greater probability of a global and coastal El Niño for Q1-2024 may result in cautious sentiment at the BCRP, although core inflation is in line. Both in its latest statement and in recent monetary operations, the BCRP has given signs that it is ready to start the cycle of interest rate cuts, which we believe will happen soon. Our base scenario considers that the cut cycle could start at its next meeting on Thursday, September 14th, without changing the monetary policy stance, but it is not so clear that it will do so.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.