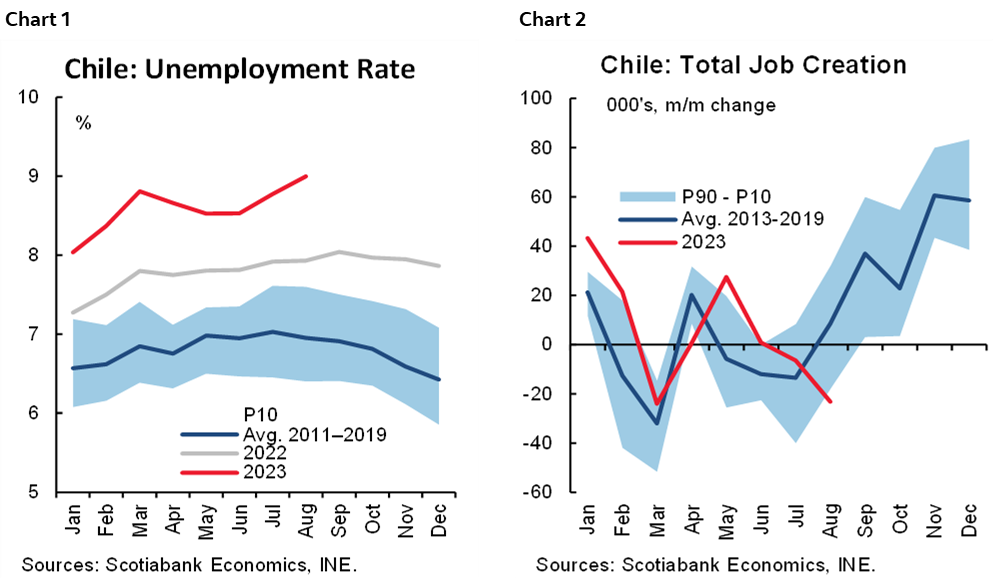

- Chile: Unemployment rate reaches 9% in August, the highest since early 2010 (excluding the pandemic)

- Mexico: The expectation of higher inflation complicates the outlook for Banxico

- Peru: Inflation continued decelerating in September

CHILE: UNEMPLOYMENT RATE REACHES 9% IN AUGUST, THE HIGHEST SINCE EARLY 2010 (EXCLUDING THE PANDEMIC)

The labour market lost 23k salaried jobs, mainly private. President Boric announced a 3.5% growth in the Fiscal Budget for 2024.

This morning, the statistical agency (INE) released the unemployment rate, which rose to 9% (chart 1) due to the worrisome weakness of employment but favoured by the low dynamism of the labour force. A faster recovery in labour participation would have led to even greater increases in the unemployment rate. In the quarter ending in August, the economy lost 23k jobs (chart 2), mainly salaried ones. The slow recovery of the labour force would respond, this time, not to the abundance of liquidity, but to the low levels of confidence and availability of jobs. It is possible that people are excluding themselves from the job search due to the low perceived chances of finding a job.

The loss of 23k jobs was mainly due to private salaried employees (-15k), concentrated in commerce. Although the fall in salaried employment was fairly generalized, including public employees (-4k), the destruction of more than 19k jobs in commerce stands out. Also noteworthy is the weakness shown for several months in employment-intensive sectors such as manufacturing and construction. Unemployment insurance administrative records (which exclude the public sector) also show a contraction of salaried employment in the private sectors, even greater than that observed during the subprime crisis.

There was a loss of 4k salaried public sector jobs in the context of fiscal adjustment. The contribution of the public sector to employment at the beginning of 2023 was relevant and allowed maintaining positive total job creation figures in the first quarter. More recently, the public sector contributed through the hiring of employees in education, health and public administration. However, in August, the Ministry of Finance announced a USD2 bn cut in public spending to cope with lower-than-expected revenues, which anticipates a weak contribution of the public sector to labour market dynamism in the coming quarters.

Related to this, on Thursday, September 28th, President Boric announced the delivery of the 2024 Fiscal Budget bill to congress, which will have 60 days to discuss and approve the initiative. In the announcement, Boric anticipated that fiscal spending will grow by 3.5% (adjusted for inflation) in 2024.

On Tuesday, October 3rd, the Ministry of Finance will present to congress the Q3-2023 Public Finance Report, which accompanied the Public Budget Bill. In the report, the MoF will provide more details on the macroeconomic forecast for the short and medium term, as well as details on public expenditures for 2024 contained in the Fiscal Budget Bill.

—Aníbal Alarcón

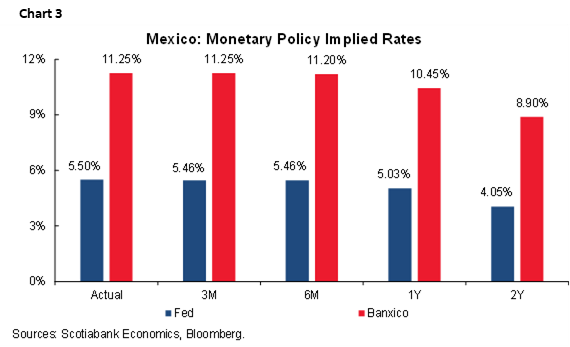

MEXICO: THE EXPECTATION OF HIGHER INFLATION COMPLICATES THE OUTLOOK FOR BANXICO

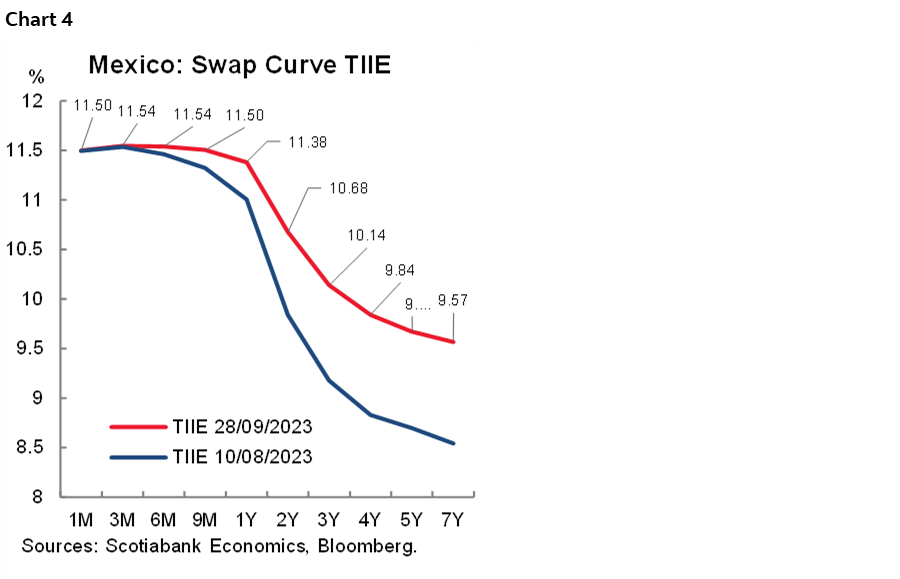

As expected, Banxico left the rate unchanged at 11.25%. However, the central bank revised upward the inflation outlook, and maintained the hawkish signal to keep the rate on hold for a prolonged period. Since the previous policy meeting, a lot of domestic and external factors have changed the economic outlook for the coming year, including the strong possibility of interest rates at a restrictive level for a longer period. In this regard, the statement noted that the global growth outlook suggests a stronger pace of expansion than anticipated for 2023. The board also mentioned that they anticipate high rates in advanced economies for a longer period. In this regard, we noted that the hawkish tone of the Fed at its last policy meeting, where it suggested the possibility of an additional rate hike in the remainder of the year, could generate some pressure on Banxico to maintain a restrictive tone (charts 3 and 4). Although a US government shutdown could dispel the chances of another hike, uncertainty around data developments and the Fed’s hawkish stance could remain in place.

In domestic factors, Banco de México highlighted the resilience of economic activity and the strength of the labour market. Although there was no mention of the Fiscal Package 2024, it noted that medium and long-term government securities rates have registered increases. We believe that the fiscal policy planned for next year could boost the economy’s growth, and thus generate greater upside risks on inflation, which would result in greater pressure for the central bank to maintain the rate for a longer period.

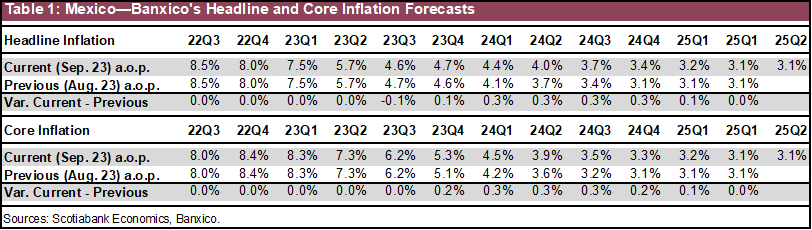

In this sense, Banxico revised upwards its inflation expectations, while highlighting once again an upwardly biased balance of risks for inflation. Thus, amid a high degree of uncertainty, the statement acknowledged a complicated and uncertain inflation outlook. The upward risks mentioned were: 1) persistence of core inflation, 2) exchange rate depreciation amid financial volatility, 3) greater cost pressures, 4) more gradual decrease in inflation owing to a strong resilience of the economy, 5) and pressures on commodity prices. On the downside, the risks mentioned in the statement were: 1) a further slowdown in the economy, 2) lower pass-through of cost pressures, and 3) that exchange rate appreciation would contribute more to cooling inflation. The central bank now expects inflation to converge to its target in the second quarter of 2025 (table 1).

In this sense, it will be necessary to maintain a restrictive level for longer. In our view, a faster pace in the economy for the following year will lead to greater pressures on the dynamics of core and headline inflation. Therefore, our expectation now is that the first monetary policy cut will take place in March of next year, although we do not rule out the possibility of other scenarios, depending on the development of economic data in the following months.

—Miguel Saldaña & Brian Pérez

PERU: INFLATION CONTINUED DECELERATING IN SEPTEMBER

We expect inflation in September to be close to 0.3% m/m, lower than that of August (+0.38% m/m) and that of September 2022 (0.52% m/m), so the pace y/y would decline from 5.6% to 5.3%. Our forecast is close to the official figure of 5.2% (MoF) and the market consensus (5.4%), according to a Bloomberg survey.

According to the monitoring of key prices that we carry out, we see that the correction in poultry prices has continued (-12%), partially offset by increases in prices of perishable foods (mainly citrus fruits and tubers), which reflects the impact of the adverse climatic conditions caused by El Niño. Core inflation would also be around 0.2%, falling from 3.8% to 3.7%.

Inflation in October 2022 was relatively low (0.35% m/m), a pace like the current one, so it is possible that the inflation trend will stabilize around 5.3% in October. The comparison base effect would play in favour again in November and December, although by then it is likely that perishable food prices will be under upward pressure, reflecting the effects of a strong El Niño scenario. The BCRP began its interest rate cut cycle in September, although with the warning that it would not be a cycle of recurring cuts, so there is the possibility of a first pause in October, the month in which we consider it more likely that the rate of inflation does not decrease.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.