- Colombia: Monetary Policy Preview—BanRep is expected to hold in a split vote

- Mexico: Trade balance is set to close the year in deficit

COLOMBIA: MONETARY POLICY PREVIEW—BANREP IS EXPECTED TO HOLD IN A SPLIT VOTE

On Friday, September 29th BanRep will hold its regular monetary policy meeting, market and economist consensus, and our expectation is that BanRep’s board will keep the policy rate at 13.25%, however, this time the consensus can be broken. Since the last meeting in July, activity data continued showing a mixed picture: a weak performance in goods-related sectors and still-resilient services sectors. On the inflation side, the slowdown continued, however, August inflation surprised to the upside reflecting a reversal in food prices.

Finance Minister Bonilla has emphasized that he will vote for a rate cut, but some board members, including Governor Villar, remain concerned about inflation and probably will be tilted to the stability side.

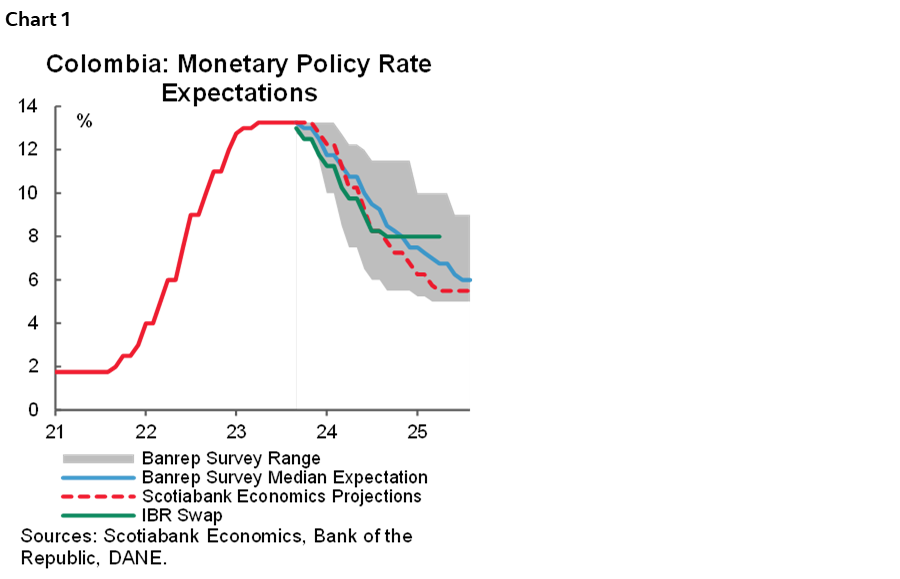

Economists and market consensus are both anticipating rate cuts until October 2023. In Scotiabank Economics the first cut of 50 bps is expected in December 2023 (chart 1), however, it strongly depends on inflation affirming a downward trend, especially core inflation. In any case, our bias is towards having the later start of the easing cycle but at a faster pace, either way by the end of 2024 we expect the monetary policy rate to close at 6.75% and the potential end of the easing cycle between 5.50% and 6%.

Key points to keep in mind ahead of BanRep’s vote:

- In July, BanRep maintained the monetary policy rate stable at 13.25% in a unanimous vote. In this session, the board remarked on inflation progress, however, they also highlighted that inflation and inflation expectations remain well above the target of 3%. Additionally, they said uncertainty remains high amid the potential effect of the “El Niño” weather phenomenon, supply shocks amid the Russian invasion of Ukraine, and gasoline price increases.

- Since the last monetary policy meeting, economic activity data continued weakening. Domestic demand slowdown continues with mixed signals among sectors. Credit continued decelerating and consumer credit passes from expanding 5% in July to 2.0% in recent data. Manufacturing and retail sales continued reflecting the economic slowdown, however, services sectors remained expanding. That said, despite the economy slowing down, the positive side is that households are reducing their financial burden, which is the main purpose of the monetary policy tightening.

- Inflation surprised to the upside in August, proving that inflation convergence towards the target could take longer than expected. In August, inflation came in at 0.70% m/m, well above market expectations and despite headline inflation continued the downtrend, it remains at a double-digit level (11.43% y/y). Core inflation stood at 11.19% ex-food and 9.92%, excluding food and regulated prices. In that context inflation expectations increased by the end of the year to 9.55% and one and two years ahead are at 6.05% and 4.14%, still above BanRep’s target range (between 2% and 4%).

All in all, BanRep’s discussion could become harder by the minute. The board is now facing a mixed picture in which a dilemma is starting to surge: the slowdown in the economic activity is motivating requests from some sectors for a rate cut, and also is a concerning issue for the government since it limits the potential tax collection in the future. On the other side, inflation correction proved to be fragile and still with high uncertainty due to weather phenomena, setting of the minimum wage increase, and gasoline prices increment among other issues that could make inflation convergence slower than expected.

In Scotiabank Economics, the base case is for rate stability in September and October and a rate cut in December, which will strongly depend on inflation dynamics. As mentioned before, if uncertainty remains significantly high for inflation, the bias is towards later but the strongest rate cuts will come in 2024.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

MEXICO: TRADE BALANCE IS SET TO CLOSE THE YEAR IN DEFICIT

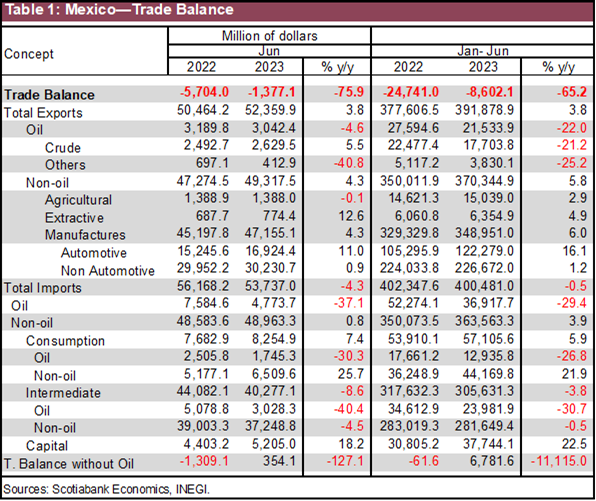

In August, the trade balance reported a deficit of -$1.377 billion dollars (bd), from -$881.2 md previously. Imports fell -4.3% y/y (-7.7% previous), highlighting the deceleration of capital imports 18.2% (23.3% previously), while consumer imports rose 7.4% (-9.1 previously), but intermediate goods fell -8.6% (-10.4% previous). Exports accelerated 3.8% y/y (2.9% previously). Two details, manufacturing exports moderated by 4.3% (6.8% previously), and automotive exports by 11.0% (35.7% previously). On the other hand, the oil trade balance registers a deficit of -$1.731 bd, since exports fell -4.6% y/y, being the seventh negative print, and imports once again drop -37.1% y/y (-50.8% previously). In the cumulative period from January to August, the trade balance recorded a deficit of -$8.602 billion, exports have grown by 3.8% YTD and imports have fallen by -0.5% YTD compared to the same period in 2022 (table 1).

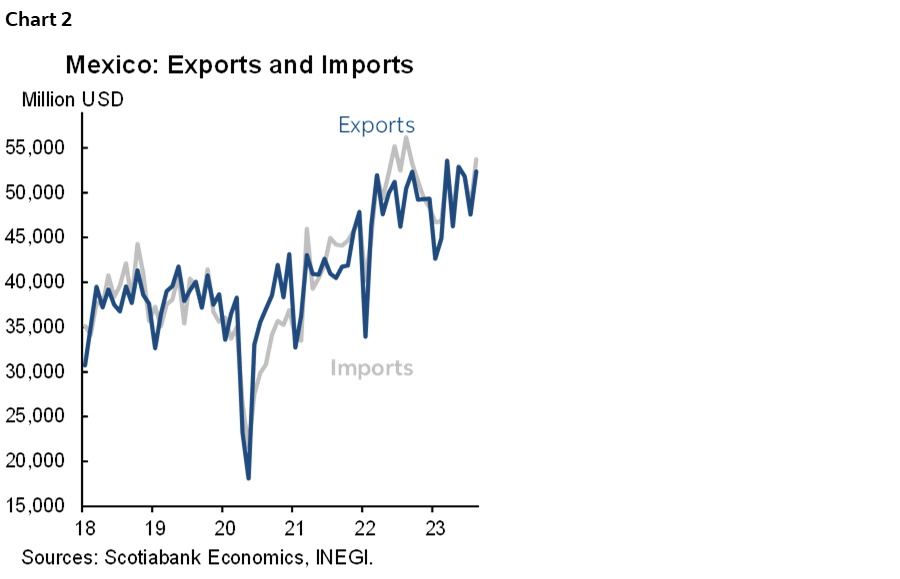

These data reflect the solid external demand for Mexican products through exports, despite an economic slowdown that has been less pronounced than anticipated in many economies. It is important to highlight that exports of automotive products have experienced a moderation in their growth, pending possible delays in the sector in coming months owing to the workers’ strike in the United States. On the other hand, regarding imports, negative prints have been observed for intermediate goods during the last six months (chart 2). This has been partially offset by a steady increase in imports of capital goods, which have seen growth for 31 consecutive months, as they are essential for the operation and development of companies. We expect the trade balance to close the year with a deficit, since, to date, surpluses have only been recorded in the months of March and June. This is partly due to the influence of the exchange rate, which can curb exports if strength continues, while for importers, the absence of currency hedging can be a challenge in the event of a depreciation in the medium-term.

—Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.