- Mexico: Changes on several data fronts drove upward revisions to our growth and inflation forecasts for 2024; Headline inflation continues to decline, supported by negative prints in energy; GDP proxy moderated in July, but the outlook remains solid for the rest of the year

MEXICO: CHANGES ON SEVERAL DATA FRONTS DROVE UPWARD REVISIONS TO OUR GROWTH AND INFLATION FORECASTS FOR 2024

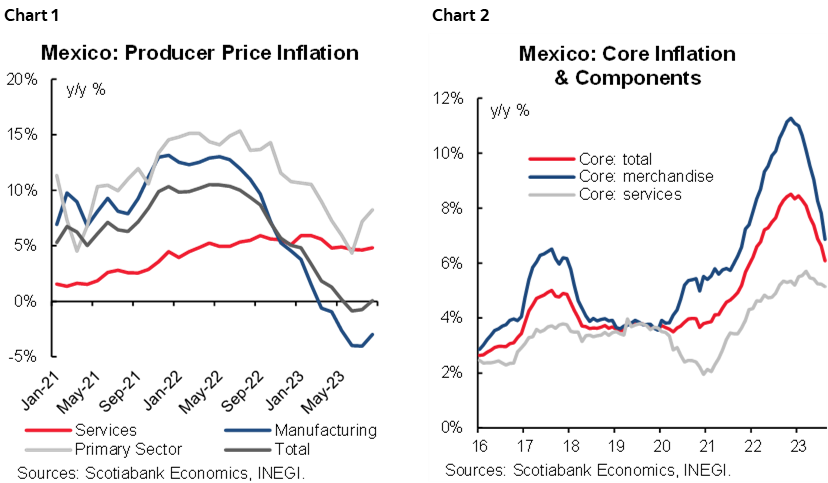

Services inflation continues to defy gravity, while merchandise price dynamics deteriorate a little.

Traditionally, producer price dynamics in Mexico have foreshadowed CPI inflation dynamics by about 6 months. In the current cycle, that relationship proved extremely accurate in predicting both the peak in headline inflation, as well as the dynamics for core goods and services inflation. Services inflation never rose as strongly as the rest of inflation components, but services inflation has proven to be the stickier, on both the producer and consumer side. We believe this is in large part due to the strength of the Mexican labour market, where unemployment currently sits at 3%, which remains close to its all-time low (the share of labour in the services sector tends to be larger in the cost structure). Merchandise inflation and non-core commodities have so far led the decline in Mexican headline inflation, but recent spikes in commodity prices, spearheaded by oil which is once again trading near US$100/bl, can light some warning signs (charts 1 and 2).

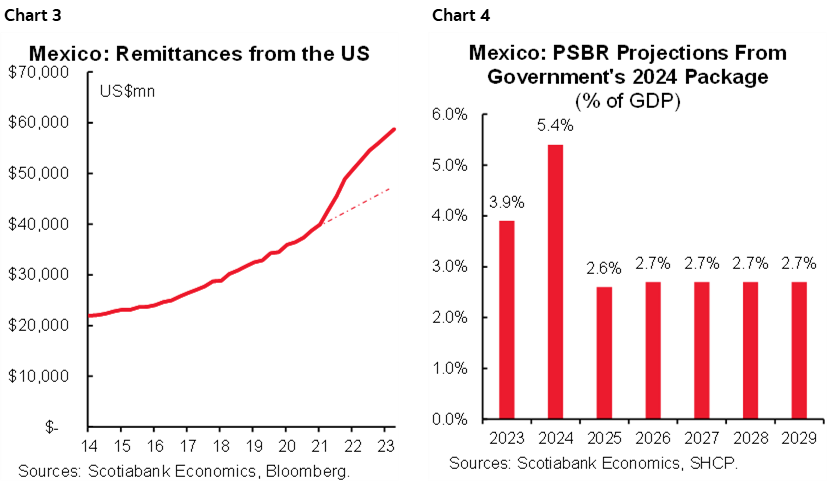

Mexican demand is getting strong boosts, which could pressure inflation.

If remittances had maintained their historic trend, we would likely be seeing levels just below US$50bn for 2023. However, following the pandemic, these flows have surged and are likely to close the year near US$65bn, which means Mexican consumption is getting about a 1 percentage point of GDP boost, relative to trend, thanks to these inflows (chart 3). In addition, in the recently published 2024 Economic Package from the government, the public sector’s borrowing requirements (the PSBR) are rising sharply to 5.4% of GDP. Within the rise in spending, physical investment is falling modestly, which suggests that much of the added public spending will likely end up boosting consumption (chart 4). Even in electoral years where the deficit does not rise as sharply (the projected PSBR for 2024 is the widest since 1988), we usually see about a 70bps y/y acceleration in growth for the 3 quarters heading into the election—and with this boost, it will likely be even stronger this time around. The combination of transfers from the government and remittances will likely keep demand red hot heading into the summer of 2024.

All this put together to us suggests that next year, Banxico’s decision makers will likely face a materially stronger growth picture than was of consensus a couple of months ago, but also a more challenging environment for inflation reduction. With this in mind, we are revising our Mexican GDP forecast for 2024 to +3.1% y/y, but also our inflation forecast to 4.6% y/y.

What about Banxico?

We tend to agree with what is discounted in the TIIE curve now; that Banxico will keep rates on hold for the next 6 months, and to cut about 100bps over the next 12 months. By the end of 2024 we expect the policy rate to sit at 9.50%. Longer term, we think estimating the neutral rate is going to be challenging. The pension reform that kicked in this year will mean a rapid acceleration of Mexico’s pension fund AUMs. Without revisions to the “siefores” investment regimes, which currently cap foreign investments at 20%, the assets under management of the domestic pension system look set to grow faster than investable assets. This could in turn lead to an appreciation in investable assets, which can reduce the cost of capital within Mexico (at least as long as public finances remain orderly, and demographics keep the population in its growing stage—which based on UN population projections will be the case for at least the next 20 years or so). Now, the neutral rate in Mexico is consistent with about a 450bps spread relative to the US, both with traditional macro models as well as through a principal components analysis. Bootstrapping the TIIE curve shows that the implied spread between Mexico and the US is starting to tighten, and has at points in recent months gone south of 400bps, which could suggest markets are starting to price in such a scenario. It may well prove to be the case that the terminal rate Banxico has once inflation gets back to target, will sit at 400bps north of the US or potentially a little tighter than that.

—Eduardo Suárez

HEADLINE INFLATION CONTINUES TO DECLINE, SUPPORTED BY NEGATIVE PRINTS IN ENERGY

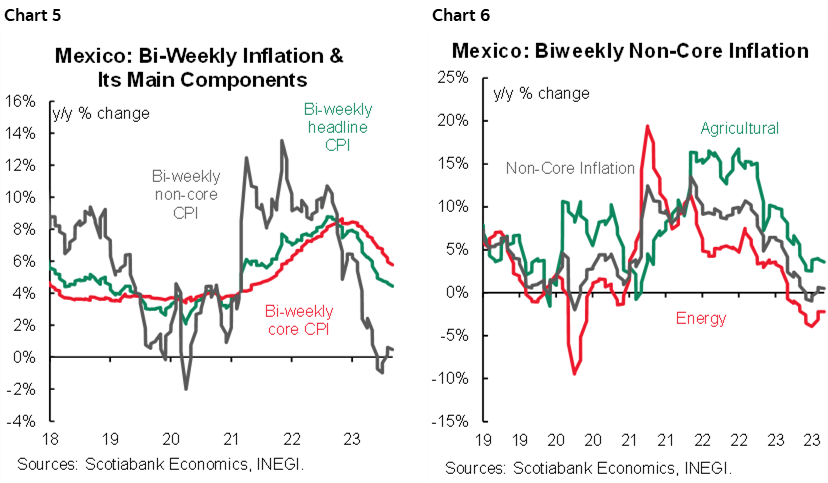

In the first half of September, annual inflation fell from 4.60% to 4.44% y/y (vs. 4.48% consensus), representing its ninth consecutive downward print and the lowest since March 2021, while the core inflation went from 5.96% to 5.78% y/y (vs. 5.76% consensus). Merchandise decelerated 6.35% (6.66% previously), and services decelerated marginally 5.08% (5.11% previously). On the other hand, non-core inflation moderated 0.48% (0.61% previously), highlighting the energy item, that continues to fall, this time -2.20%. In its biweekly comparison, headline inflation almost remained at the same level of 0.25% 2w/2w (0.26% previous, 0.30% consensus), as the core component rose 0.27% 2w/2w from 0.08% (vs. 0.25% consensus) and the non-core moderated to 0.19% 2w/2w from 0.82% (charts 5 and 6).

These data suggest that inflation will be persistent, and we do not expect significant downward prints in the last quarter of 2023, as we expect inflation at 4.70% by the end of 2023, due to possible increases in agriculture, as the core component has been falling for 12 months but at a slower pace. Analysts expect that headline inflation will close in a range of 4.30%–5.50%, which reinforces the perspective of stickiness. Also, these levels of inflation and the strength of economic activity can lead to a longer period of high rates, which is why the 2024 terminal rate will be revised upwards in the following surveys, which currently the median is 8.50% for 2024.

—Brian Pérez

GDP PROXY MODERATED IN JULY, BUT THE OUTLOOK REMAINS SOLID FOR THE REST OF THE YEAR

In July, the GDP monthly proxy (IGAE) moderated 0.2% m/m from 0.5% m/m s.a. previously, slightly below consensus of 0.3%. The industry sector moderated 0.5% (0.8% previously), services fell -0.1% (0.4% previously), and primary activities also fell to -0.2% (1.0% previously). In its annual comparison with non-seasonally adjusted figures, the index moderated to 3.2% y/y from 4.1% previously, below the 3.5% consensus. By sectors, industry grew 4.8% y/y (4.9% previously), with manufacturing moderating to 0.8% (1.7% previously), while construction posted a significant increase of 25.6% (22.9% previously), mainly owing to public projects, as we have stated in previous editions. Services moderated to 2.2% (3.7% previously), with wholesale trade rebounding to 2.3% (-0.51% previously), while retail trade slowed to 4.7% (8.4% previously), and primary activities moderated 3.7% (4.0% previously). In a cumulative basis, economic activity stands with a 3.6% YTD increase in the first seven months of 2023, with solid advances in both industry (3.9% YTD) and services (3.5% YTD, see table 1 and chart 7).

GDP forecasts have been continuously revised up since the beginning of the year, mainly owing to stronger-than-expected consumption in the first half of the year led by services. In the last months, industry have also surprised up, as construction soars benefitted by a stronger dynamism in civil engineering projects (most of them by public sector). For the rest of the year, as the labour market still shows signs of solid indicators, we expect services to continue to be resilient, and industry to show advances coming from the auto sector and construction. Thus, we expects 3.3% GDP during 2023, with upside risk that could materialize in the second half of the year.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.