- Colombia: Manufacturing and retail sales contracted for fifth month in a row, but there are signs of recovery in some durable goods sales; Inflation expectations increased, and consensus is now pointing to a 25 bps rate cut in October

- Peru: GDP just can’t catch a break

It was a very quiet overnight session with not much doing in Asia hours to start the week, as Japanese markets were closed, before price action picked up a bit at the UST open in Europe. US and German curves are bear flattening, the USD is mixed in 0.1/2% ranges (MXN +0.2%), oil is at it again with a 0.5% gain alongside copper (+0.3%) versus iron ore (-1%), while SPX futures trade flat.

There’s little of note in today’s ex-Latam schedule. Only Canadian housing starts at 13.15UK and comments by Saudi’s Energy Min are worth a quick look ahead of a busy week that includes Canadian and UK CPI, the Fed (hold, hawkish guidance), the BoE (hike 25bps, data-dependent), and the BoJ (steady hand), among others, ending the week with PMIs on Friday.

Today’s Latam highlight, Colombian July economic activity, drops at 12ET on the heels of some disappointing manufacturing and retail sales data out last Friday (see below). The median economist projects a 1.1% y/y expansion at the start of the quarter, a touch below our team’s forecast of 1.3% y/y and in either case representing a weak pace of growth that has some economists (like in BanRep’s survey) expecting rate cuts to start next month in Colombia; we don’t see these starting until December.

Peruvian GDP disappointed yet again in data released at the end of the week (see below), and the weakness went beyond El Niño headwinds, reflecting depressed domestic demand. At 9ET, we’ll watch commenting from the country’s Fin Min Contreras on the state of the economy, which is looking possibly on track to miss our 0.5% forecast for growth in 2023.

Chilean markets are closed today and tomorrow for Independence holidays. Over the remainder of the week, we’ll get Brazilian and Mexican economic activity, H1-Sep Mexican CPI, and the BCB’s decision on Wednesday as the main event this week, with a 50bps cut expected to take the Selic rate to 12.75%.

—Juan Manuel Herrera

COLOMBIA: MANUFACTURING AND RETAIL SALES CONTRACTED FOR FIFTH MONTH IN A ROW, BUT THERE ARE SIGNS OF RECOVERY IN SOME DURABLE GOODS SALES

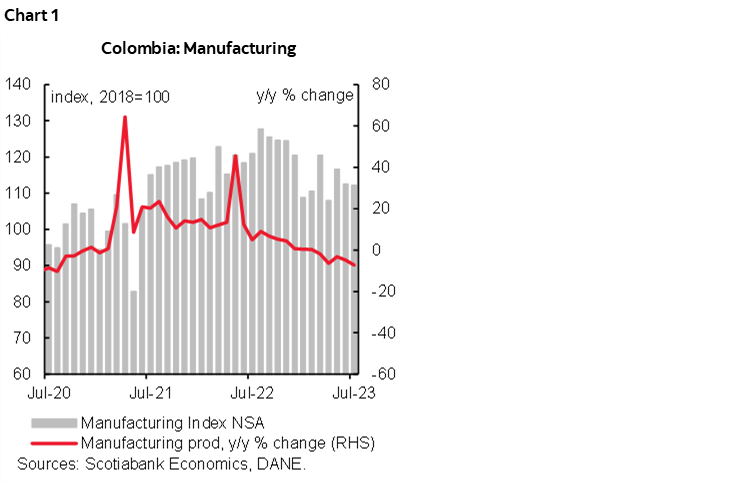

On Friday, September 15th, the National Administrative Department of Statistics (DANE) released information regarding manufacturing and retail sales for July 2023. Real output of the manufacturing industry once again fell by 7.2% y/y in July 2023, marking its weakest print so far this year. Meanwhile, real retail sales decreased by 8.2% y/y in July, but this was a more moderate decline compared to the previous month (-12.0% y/y in June). July marks the fifth consecutive month in which manufacturing production and retail sales have both sat in negative territory. Furthermore, these results have surprised market expectations, including our projections.

Friday’s data confirms that the economy likely reached its weakest performance in H1-2023 and there will be a gradual recovery of activity indicators in coming months. The effect of monetary policy tightening is evident, especially in the demand for durable goods. BanRep’s dilemma continues to be weak economic growth against still-high inflation, however, we think the inflation target mandate prevails and that is why we changed our call for rate cuts to December.

Manufacturing Production

Manufacturing production contracted 7.2% y/y in July 2023 (chart 1), marking the fifth consecutive month of decline and missing market analysts’ expectations (-5.0% y/y). In seasonally adjusted terms, manufacturing contracted by 1.2% m/m.

Out of 39 industrial activities, a total of 33 recorded negative variations in their real production, subtracting 8.9 p.p. from the total annual variation, while 6 sectors showed positive variations that collectively added 1.6 p. p. to the total variation.

In annual terms, the sectors that showed better performance were the manufacture of vehicle bodies and trailers (+10.7% y/y), coking, petroleum refining, and fuel blending (+10.4% y/y), sugar and panela processing (+7.7% y/y), and other manufacturing industries (+6.6% y/y). On the other hand, the sectors that recorded the largest contractions were rubber manufacturing (-52.5% y/y), motor vehicle manufacturing (-39.3% y/y), iron and steel industries (-30.5% y/y), precious metals industries (-28.5% y/y), and the manufacture of other types of transportation equipment (-26.5% y/y).

Furthermore, other significant industries experienced annual contractions, particularly those related to durable and semi-durable goods, such as spinning, weaving, and finishing of textiles (-24.0% y/y), manufacturing of travel goods, handbags, and similar leather articles (-20.4% year-on-year), clothing manufacturing (-18.3% y/y), manufacturing of furniture, mattresses, and bed bases (-10.5% y/y), and footwear manufacturing (-7.9% y/y).

Retail Sales

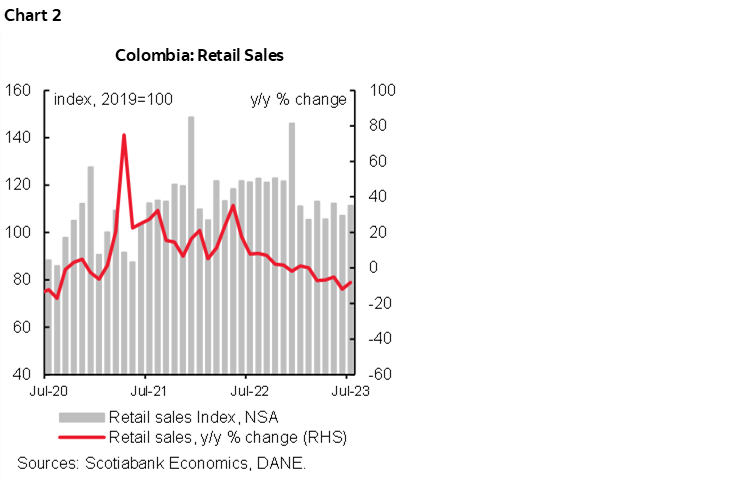

Retail sales contracted by 8.2% y/y in July 2023 (chart 2), showing a slight improvement compared to the previous month’s figure (-12.0% y/y in June). However, like the manufacturing industry, it recorded the fifth consecutive month in negative territory. This result slightly exceeded the -7.8% y/y expected by Bloomberg analysts. In seasonally adjusted terms, retail trade excluding fuels and vehicles showed a growth of 1.1% m/m compared to the previous month. These results indicate a slight recovery in household consumption this year, following three consecutive months of decline.

Out of the 19 lines of goods that make up the indicator, 13 lines of merchandise recorded negative year-on-year variations in their real sales, while 6 lines of merchandise recorded positive year-on-year variations in their sales.

In annual terms, the main growth was observed in sound and video equipment (televisions) with a variation of +13.0% y/y in July, followed by non-alcoholic beverage products (+10.2% y/y), household appliances, furniture (+4.4% y/y), and personal hygiene and perfumery products (+4.2% y/y). It is worth noting that the growth of durable goods such as televisions, appliances, and furniture in July indicates a slight improvement in household consumption patterns, reinforcing our hypothesis that the second half of 2023 is expected to witness a gradual recovery in economic activity and an improvement in household consumption.

However, the performance of retail sales in July 2023 was influenced by a decline in the sales of motor vehicles and motorcycles primarily for household use (-32% y/y), other motor vehicles and motorcycles (-28.1% y/y), as well as hardware, glass, and paint (-18.0% y/y), and personal or household use information and communication equipment with a decline of (-14.0% y/y).

Final Remarks

While Friday’s data is weaker than we expected, sales of durable goods such as televisions, furniture, and appliances are beginning to show slight signs of recovery, which we expect to continue gradually into the second half of 2023. Additionally, we will have to wait and see how sectors related to services perform with the publication of the ISE next Monday. At Scotiabank Colpatria, we estimate a year-on-year economic activity growth of 1.3% for July.

Nevertheless, achieving a result within this range will likely not significantly affect market expectations regarding monetary policy decisions at the end of this month, given that the most recent inflation data have biased the likelihood toward a later start of the central bank’s easing cycle. At Scotiabank Economics Colombia, our official call for a rate cut begins in December due to the slower pace of inflation deceleration.

INFLATION EXPECTATIONS INCREASED, AND CONSENSUS IS NOW POINTING TO A 25 BPS RATE CUT IN OCTOBER

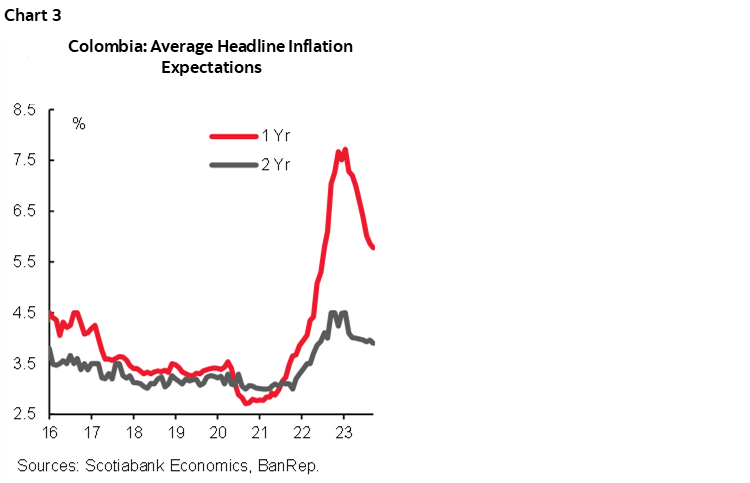

On Friday, September 15th, the Central Bank (BanRep) released its monthly survey of economic expectations. The upside surprise in August inflation leads to an upside revision in inflation expectations for the year-end. Dec-2023 inflation is now expected at 9.55%, while one- and two-year expectations remain above the target range at 6.05% y/y and +4.14% y/y, respectively. The monthly inflation for September is expected to be 0.53% m/m, which could take down headline annual inflation to 11.03% y/y, from the current level of 11.43%y/y. In Scotiabank Economics, the forecast is slightly above consensus at 0.60% m/m (chart 3).

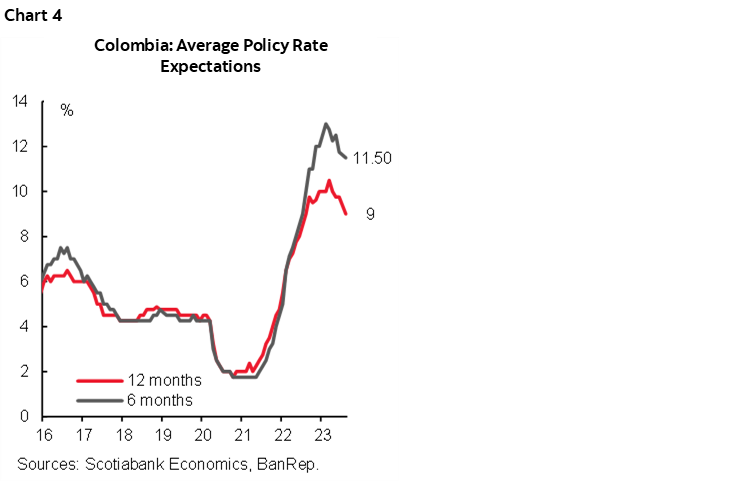

Regarding monetary policy, economists’ consensus anticipates stability in the monetary policy rate at 13.25%, in September which aligns with Scotiabank Economics’ expectations. The first cut is still expected in October, and by the end of the year, the rate is expected at 12.50%, 50 basis points higher than in the previous survey. In Scotiabank Economics we revised our expectation, and now the first rate cut is expected in December, with a magnitude of 50 bps, however the main bias continues to be for a later start of the easing cycle but with a stronger move.

Key points from the survey:

- Short-term inflation expectation. For September, the consensus is 0.53% m/m, which implies an annual inflation rate of 11.03% y/y (down from 11.43% in August). The maximum expectation at 0.75% and the minimum at 0.30%. Scotiabank Economics forecast is 0.60% m/m and 11.06% y/y.

- Medium-term inflation was revised to the upside. Inflation expectations for December 2023 increased to 9.55% y/y, +0.47 percentage points compared to the previous month’s survey (table 1). Upside revision responds to the upside surprise on August’s inflation results. The headline inflation expectations for the one-year horizon are at 6.05% y/y (+1 bps vs previous survey), while the two-year outlook increased by 10 basis points to 4.14% y/y.

- Policy rate. The median expectation (chart 4) points to a 25 bps rate cut in October. By the end of 2023, the policy rate is projected to reach 12.50%. It is worth noting that expected monetary policy path was revised to the upside compared with the previous survey, and the expectation for Dec-2024 now is at 7.50% (previous 7.25%). In Scotiabank Economics, the first rate cut is expected in December, however it strongly depends on further inflation correction. However, if inflation reduction continues proving to be fragile, we think the first cut could be delayed until Q1-2024.

- FX. The projections for the USDCOP exchange rate for the end of 2023 averaged 4094 pesos (12 pesos lower compared to the previous survey). For December 2024, respondents, on average, expect the peso to settle at USDCOP 4065 pesos. The USDCOP rate for the end of September is expected to be around 4020 pesos.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

PERU: GDP JUST CAN’T CATCH A BREAK

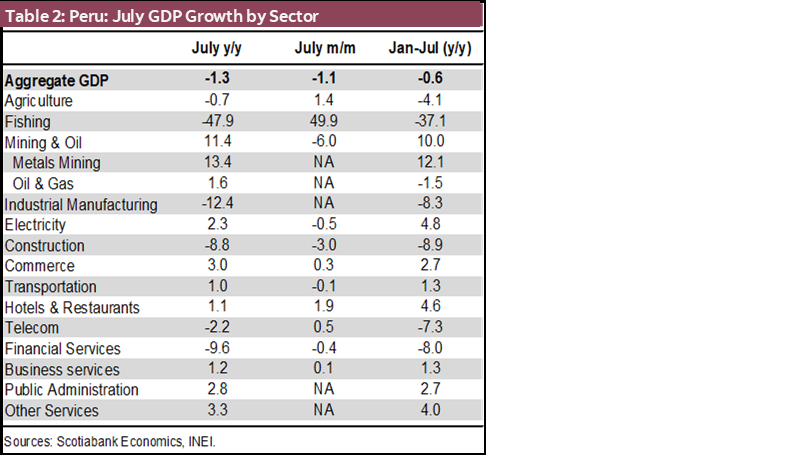

Oh dear! July was simply dismal! Not because of the weather, which was actually sunny for a mid-winter month. It was the economy which was as cold as ice. GDP plunged 1.3%, y/y. In seasonally-adjusted month-on-month terms the result was equally bleak, down 1.1%.

At least now, after seeing the July GDP numbers, we have a better understanding of why the BCRP went ahead in lowering the reference rate on September 14th after having suggested it might not do so only two weeks earlier. As information on July GDP came in, this may well have tilted the decision towards lowering rates.

The worst part was, El Niño wasn’t even the main culprit. It was mainly due to sectors linked to domestic demand.

The impact of El Niño was real, but a bit softer than in previous months. Fishing was down 0.48%, which is hefty, but off the highs of 70% of previous months. The 0.7% y/y decline in agricultural GDP was linked to El Niño, but it was also the lowest decline this year. Moreover, agricultural GDP was actually up a promising 1.4% in m/m terms. Fishing and agriculture together only represented 0.24 percentage points of the 1.3% decline in GDP (table 2).

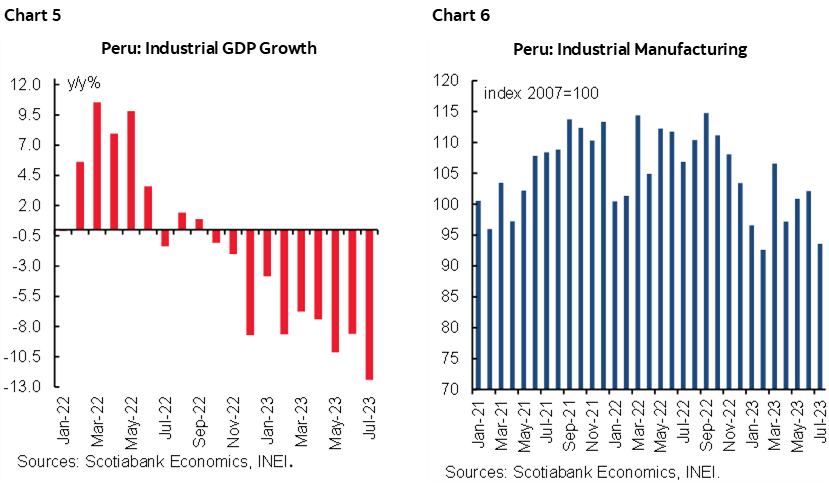

The biggest and most worrisome factor behind July’s steep drop was industrial manufacturing which fell a whopping 12.4% y/y, and 1.9% m/m. Industrial manufacturing has now declined for ten consecutive months, and 8.3% in the year-to-July. This is a greater decline than is warranted by domestic demand, which is weak but not this weak. It is our understanding that many industrial companies in different sectors came into 2023 with high inventories, which are still being worked off (charts 5 and 6).

The 8.8% y/y decline in construction was in line with trend, which is no consolation, especially considering that this represented a 3% decline in m/m terms. The silver-lining is that cement demand has started to creep up in m/m terms, and provides hope that construction GDP will start to turn around, if not in August, at least at some point in the next three or four months.

What is denominated as production taxes fell 5.5% and, given its weight (8.3%) took nearly 0.4 pp off growth, which is a pretty strong impact.

All other sectors were in line, more or less. Metals mining continued outperforming, up 13.4%. A number of sectors linked to domestic demand, including electricity, commerce, business services, transportation, restaurants and government services, rose broadly in line with expectations. Note that these were mainly service sectors, which contrasts with goods-producing sectors (e.g. industrial manufacturing), giving credence to the argument that the latter are working off excess inventories.

The bottom line is that July GDP was under double pressure, from El Niño and from slow domestic demand. The impact of El Niño will subside in the months that follow, until the second round begins in early 2024. However, slow domestic demand appears more structural and less temporary. Here the sectors to follow are industrial manufacturing and construction. Both need to begin to turnaround.

As a final note, year-to-July growth is now -0.6% y/y. This means that the economy needs to turn around quite quickly for it to end 2023 with any growth at all. Our GDP forecast of mild 0.5% growth for 2023 is still in play, but the July result has augmented the downside.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.