- Mexico: Industrial production slightly slows, remains strong

After the week started out with a bang on BoJ/PBoC developments, Tuesday’s Asia session lacked any notable news, while European hours delivered a mixed UK jobs report that at the very least does not add to BoE hike bets. The G10 day has little on tap while markets await US CPI data tomorrow. US equity futures are about 0.3% lower, crude oil is up 0.8% versus a small 0.3% decline in copper, and US and Eurozone curves are flattening in contrast to bull steepening in the UK.

The USD is 0.2/3% stronger against all key currencies including the MXN, where a 0.1/2% decline is only a scratch after a massive 1.8% rally yesterday that represented its best daily move since March 2022. The overall weak dollar on Monday combined with rising local yields (owing to Friday’s 2024 economic package, see yesterday’s Latam Daily) to support the peso.

Last night, Fitch said that the support that the government laid out for Pemex in the 2024 plan is “directionally positive”, but will stay its hand on the company’s rating watch until the budget is approved—and also noted that the measures do not “fully address all of Pemex’s short-term capital needs”.

Morena’s presidential nomination runner-up Ebrard said yesterday that he may quit the party if his complaints about the murky selection process are not addressed. Morena’s party head Delgado will speak later today on Ebrard’s accusations. This should have no influence on markets today, but his departure and possible candidacy with Movimiento Ciudadano are a risk to consider for next year’s presidential election.

Today’s Latam highlights are Brazilian August IPCA data at 8ET and the results of the BCCh’s economic expectations survey at 7.30ET.

Brazilian inflation is seen jumping to its highest pace since Q1, above the mid-4s in year-on-year terms (4.66% median), due mainly to less favourable base effects as fuel/utilities tax cuts fade; in September, a 16.3% increase in gasoline prices by Petrobras will also result in an inflation spike to 5%+. Setting the jump in headline inflation aside, and considering it is already seen ending the year around 5% (from the 3.2% low in June), markets will focus on the pace of price gains in services that are the BCB’s focus.

For now, markets are comfortable in their expectation that the Campos Neto-led central bank will move at a 50bps cutting pace over the next five or six meetings. But, sticky services inflation, a weaker real since late-July, and higher energy prices (and how expectations may be shaped) point to limited risk that the Brazilian front-end will rally in the near-term.

As for the BCCh’s survey, we’ll see whether the median aligns with the bank’s guidance that suggests they’ll stick to 75bps cuts at their two remaining decisions of the year, to close 2023 at 8.00%, or if it still sees a 7-handled year-end rate at 7.75% (a 25bps increase from the August survey median), which is our own forecast for year-end.

—Juan Manuel Herrera

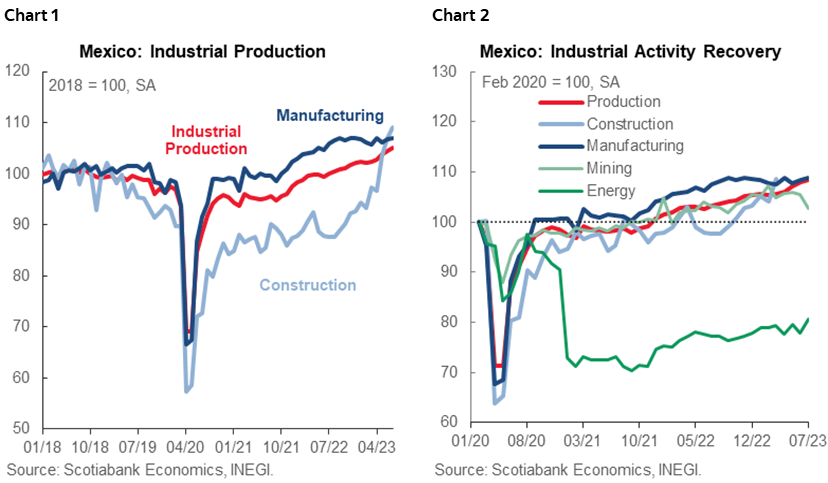

MEXICO: INDUSTRIAL PRODUCTION SLIGHTLY SLOWS, REMAINS STRONG

In July, industrial activity growth slightly moderated to 4.8% y/y from 4.9% previously (NSA terms), within which construction soared 25.7% y/y (from 22.9%), utilities rose 4.8% (from 0.3%), manufacturing rose 0.8% y/y (from 1.7%) and mining fell -0.7% y/y (from 1.6%). On a monthly comparison, it moderated slightly 0.5% m/m SA from the previous 0.8%. Construction led the way although it moderated 2.0% m/m (previous 3.3%), manufacturing slowed to 0.3% m/m (previous 0.6%), while utilities rebounded 3.5% m/m (previous-2.0%), and mining dropped -2.6% m/m (-0.4% previous). On the other hand, in the January–July period production increase 3.9% YTD.

Considering this print, we highlight the clear improvement in construction, although it took a little longer to recover, it already registers higher pre-pandemic levels, and it is more clearly observed by the change of base year by INEGI to 2018. On the other hand, manufacturing remains more stable, while energy remains far from 2018 levels, without showing a significant recovery. Win the short term, we expect additional strong annual increases in construction, supporting the positive expectations of nearshoring, linked also to the increase in construction in gross fixed investment. Manufacturing has had a smaller increase, owing to the slower pace of the US economy, in addition to restrictive rates that may be impacting the sector.

—Miguel Saldaña & Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.