- Chile: September CPI at 0.7% m/m and 5.1% y/y driven by supply shocks

- Colombia: Inflation met expectations and continued its gradual decline; a rate cut in December is still possible

Overseas markets began the week (and reopened in China from holidays since late-Sep) with sharp moves in reaction to Hamas attacks on Israel over the weekend. With US, Canadian, Japanese, and Chilean markets closed today and with no real data of note outside of Mexican CPI later this morning (see below), Israel-Hamas headlines will likely be the focus of thin markets that await the Fed’s minutes on Wednesday and US CPI figures on Thursday.

Crude oil gapped about $2/bbl at the open and added a couple more dollars that were later unwound to track a 3%/$2.5/bbl gain on the day. On the flip side, risk-off sentiment has currencies quite a bit lower against the dollar (with only a few exceptions like the JPY), with the MXN standing as the worst performing major today, shedding 0.6/7%—but still within Friday’s range. Global curves are well bid across the maturity spectrum (3/4bps in Germany and the UK), while SPX futures are down around 0.6%, and oil’s gains are accompanied by a 0.8% increase in copper and a 1% haven bid in gold that contrasts with a 2% drop in iron ore.

At 8ET, Mexican headline inflation is seen slowing marginally to 4.48% from 4.64% in August, against a more respectable slowdown in still-elevated core inflation to 5.75% from 6.08% (both in line with H1-Sep data). Prices growth is closing in on Banxico’s 2–4% target band, but progress has somewhat stalled of late given less favourable base effects and upward pressure from energy and government-regulated prices, and we see little change in y/y headline inflation over the balance of the year.

Still, though today’s print is highly unlikely to greatly influence opinion within Banxico’s board, we’ll watch the results of services inflation which remains sticky above 5% and is a key reason for the bank remaining hawkish for longer (which should be evident in Thursday’s September meeting minutes). The trend for this basket could be a better guide to when officials may begin reducing rates, which we don’t see starting until late-Q1 and risks are tilted towards later rather than sooner.

—Juan Manuel Herrera

CHILE: SEPTEMBER CPI AT 0.7% M/M AND 5.1% Y/Y DRIVEN BY SUPPLY SHOCKS

September inflation: three products explained 55% of the monthly increase

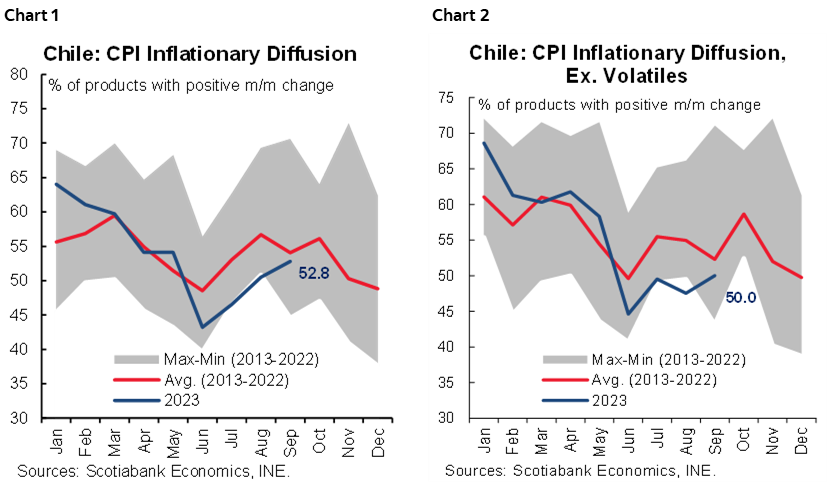

Last Friday, Chile’s statistics agency (INE) released October CPI figures, which showed an increase in prices of 0.7% m/m, above consensus and our expectations (forwards: 0.5%; Bloomberg: 0.6%) but with a composition largely explained by volatile items. Indeed, the CPI ex volatiles (SV) stood at 0.19% m/m in line with our expectation and below its historical monthly average for a September month. This becomes clearer when we see that only three products (gasoline, potatoes and tourist packages), which are very reactive to the recent rise in the exchange rate or affected by the August floods, explain 55% of the total monthly increase of the CPI.

As mentioned above, the monthly increase of 0.7% in the headline index is explained by the rise in the prices of volatile items and the increase in services (ex-volatile), which despite these increases continues to fluctuate around its historical average, indicating that the second-round effects have dissipated.

As for the goods CPI, the exchange rate weakening that started in July has not yet significantly affected prices. This is evident when looking at the total diffusion of the CPI basket and, in particular, that of goods (ex-volatile), see charts 1 and 2. However, the impact of the exchange rate, which should manifest itself in the short term in Q4-23 CPIs, is still pending. On a year-on-year basis, goods inflation fell to 4.9% (ex-volatile), while excluding food from this underlying measure, inflation stood at 1.5%.

For the central bank (BCCh), the September CPI will be read in conjunction with that of August, reflecting a muted basket of demand-related factors. Indeed, core CPI increased by a modest 0.1% between August and September. However, we also believe that the BCCh will be cautious about the recent CLP depreciation and its impact on prices during the last months of the year. We see no reason (for now) not to proceed with a further 75bps cut at the October 26th meeting, the magnitude of which would only be questioned if the peso’s depreciation continues to accentuate in the coming weeks.

—Aníbal Alarcón

COLOMBIA: INFLATION MET EXPECTATIONS AND CONTINUED ITS GRADUAL DECLINE. A RATE CUT IN DECEMBER IS STILL POSSIBLE

Monthly CPI inflation in Colombia stood at 0.54% m/m in September, according to DANE data released on Friday, October 6th. The result was aligned with expectations of 0.53 m/m, according to BanRep’s survey, and slightly below Scotiabank Colpatria’s expectation of 0.60% m/m. The main monthly contributor to the monthly inflation was food inflation, which stood at 0.74% m/m, and is relatively high given the usual seasonality, while housing and transport were the second and the third main contributors, respectively. The good news came from tradable items, such as vehicles with significant negative monthly inflation, which is an important signal of the effect of the COP appreciation and weak demand.

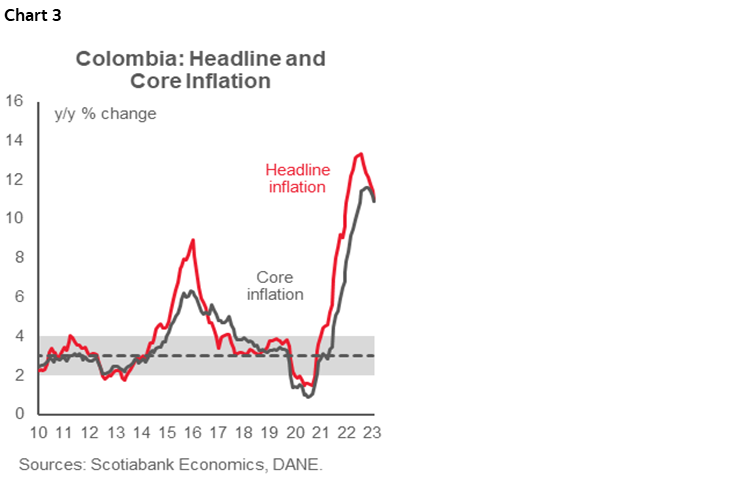

Headline inflation declined for the sixth month, from 11.43% in August to 10.99% in September (chart 3), the lowest since August 2022 (10.84% y/y). According to our projections, the headline inflation could reach a single digit around November. Core inflation fell for the third consecutive month; non-food inflation fell from 11.19% to 10.88%, while inflation ex-food and regulated prices were 9.51% y/y, also down from the previous number of 9.92% y/y in August, mainly due to a moderation in tradable goods inflation.

In any case, both headline and core inflation remain well above BanRep’s 3% target; however, both affirmed their downward trend. In y/y, food and restaurant inflation was much lower than September 2022. They accounted for the 50% of the reduction in the headline annual inflation, while clothing and furniture groups accounted for 30%. The only group that partially offset the downtrend of headline inflation was education, that still reflects higher indexation effects.

Former results affirm our expectation that there is no room for rate cuts in the October 31st BanRep meeting; however, if inflation continues its progress according to our projections and the government proves no intentions of setting the minimum wage increase for 2024 well above inflation, we think BanRep could still consider kicking off the easing cycle in December 2023.

In forthcoming months, it will be relevant to see how COP strengthened vs. one year ago could support lower tradable prices and if the El Niño weather phenomenon impact is material in key prices.

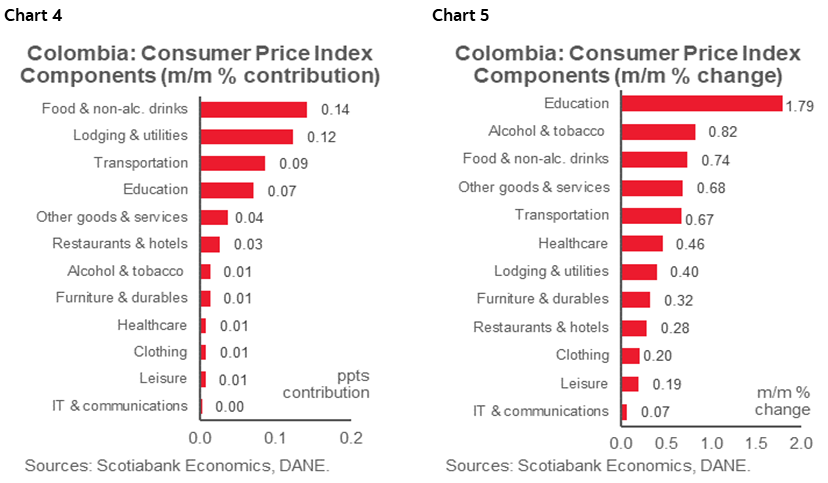

Looking at the September figures in detail, food inflation is the group that generated the greatest upside pressure on inflation during the month (charts 4 and 5).

The highlights are:

- Food inflation remained elevated and again was the main contributor to the monthly inflation, recording inflation of 0.74% m/m and contributing to the headline by 14 bps. There were significant increases in food items such as tomatoes (+39.8% m/m), onions (+13.5% m/m), and fresh fruits (+3.91% m/m). On the negative side, the main price reductions were on plantains (6.99% m/m), tree tomatoes (13.55% m/m) and oranges (-14.98% m/m); it is worth noting that 17 out of the 59 food items are showing price reductions, similar to the previous month dynamic of 14 out of 59. In the forthcoming months, the main challenge remains the El Niño weather phenomenon. Having said that, we estimate that the possible upside impact on food prices could be reflected in H1-2024 if this phenomenon turns out to be intense.

- The lodging and utilities group was the second contributor to the rise in monthly inflation. The group recorded +0.40% m/m inflation and +12 bps contribution. Rent fees continued to rise at a similar pace compared with previous months (0.58% m/m), showing that indexation effects are still present. Utility fees decreased by 0.18% m/m due to a significant reduction in gas prices (-2.13% m/m).

- Transportation was the third largest contributor to headline inflation, with a 0.67% m/m and a contribution to headline inflation of 9 bps. Gasoline inflation rose by +3.43% m/m due to a COP 400 increase. It is relevant to note that tradable goods, such as vehicles, partially offset the upside pressure from gasoline in the transportation group. In that regard, vehicle inflation posted a -1.47% m/m inflation, the most significant reduction, at least, since 2009. Vehicle price reduction reflects the COP appreciation and the effect of weak demand.

- The government maintained stable gasoline prices in October; however, Minister Bonilla said that increments will be resumed in November, and by February 2024, diesel prices are expected to increase, which could have spillovers to other key elements of the CPI basket.

- Inflation by major groups: goods inflation continued decreasing, going down from 11.83% y/y to 10.44% y/y, while services prices remained relatively stable at 9.14% vs. the previous 9.16%, reflecting still some robust demand in that sector, but also the effect of indexation. Tradable goods, excluding food, posted a 9.51% y/y inflation, lower than the previous month’s 9.92% figure. It is worth noting that clothing, home appliances and vehicles are the items that are contributing the most in the tradable goods inflation reduction.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.