- Chile: Pension reform debate in Congress delayed until after the plebiscite

- Peru: The economy has run out of time for positive growth in 2023

US bear steepening continued overnight as yields across the curve fully or almost fully return to their levels before the attacks in Israel two weekends ago. With no major escalation in the conflict over the past few days—and amid efforts from G-10 leaders to defuse the tension—markets have resumed their aversion to rates, especially the long-end, challenged by narratives of ‘higher-for-longer’ and increased US debt supply.

US equity futures are not doing much, drifting about 0.2% below yesterday’s close after a 1% rally in SPX cash markets on Monday. Crude oil is about 0.5% firmer, roughly in line with the small increase in iron ore prices but contrasting with copper’s ~1% decline after Rio Tinto reported a greater than expected production increase in Q3 (at 155k vs 150k Bloomberg consensus).

The USD is taking the UST yield gains (10s up 4bps) to rise against nearly all majors and claw back some of Monday’s losses. Though the USD is tracking mostly small 0.1/2% gains versus the bulk of the key G10 FX, it is posting a solid 0.5% increase against the MXN where higher US 10yr yields combine with a reversal of yesterday’s majors-leading 1.1% gain for the peso. At 13ET, Mexican Dep Fin Min Yorio testifies to a congressional committee today on the 2024 budget—the one that sees a large deficit increase and acted as a drag on the peso when first unveiled.

We’ll see whether the CLP can head in the opposite direction to the MXN after a 0.7% depreciation on Monday saw it close at its weakest level in eleven months at 946—after a very brief intraday period above the 950 pesos mark—amid USD buying from locals. We’ll watch comments by BCCh president Costa at an event on financial education at 8ET.

Colombian markets will reopen today to a generally quiet Latam day, where the results of Banrep’s survey of economists are the regional data highlight (watching inflation expectations and forecasts for the timing of the bank’s first rate cut) alongside Brazilian services volume figures at 8ET.

The day ahead has US retail sales and Canadian CPI at 8.30ET as the top items in the global calendar, while we continue to monitor Israel headlines; US industrial production, and some Fed and ECB speakers are also on the docket.

—Juan Manuel Herrera

CHILE: PENSION REFORM DEBATE IN CONGRESS DELAYED UNTIL AFTER THE PLEBISCITE

The pension reform is one of the emblematic initiatives of Boric’s government and contemplates some proposals for which there is broad political agreement and others where it has not been possible to advance. For example, there is broad agreement that it will be necessary to increase the Universal Guaranteed Pension (PGU), whose cost is estimated at 1.2% of GDP and would be financed by the tax reform (in the process of negotiations). On the other hand, there is disagreement between the government and the opposition parties regarding the increase in mandatory contributions, mainly on the percentage that could go to personal accounts and the percentage destined to solidarity. The government’s reform proposes an increase of 6 ppts in the mandatory contribution (charged to the employer) that would go entirely to solidarity. Although in recent weeks the government has been open to allocating only 4 ppts for this purpose, no agreement has been reached with the opposition parties, so the government has decided to freeze its processing in congress until after the plebiscite on the new constitution (December 17th). Our opinion is that the bill would be taken up again in March 2024, in parallel with the discussion of the second part of the tax reform related to the increase of personal and corporate taxes.

—Aníbal Alarcón

PERU: THE ECONOMY HAS RUN OUT OF TIME FOR POSITIVE GROWTH IN 2023

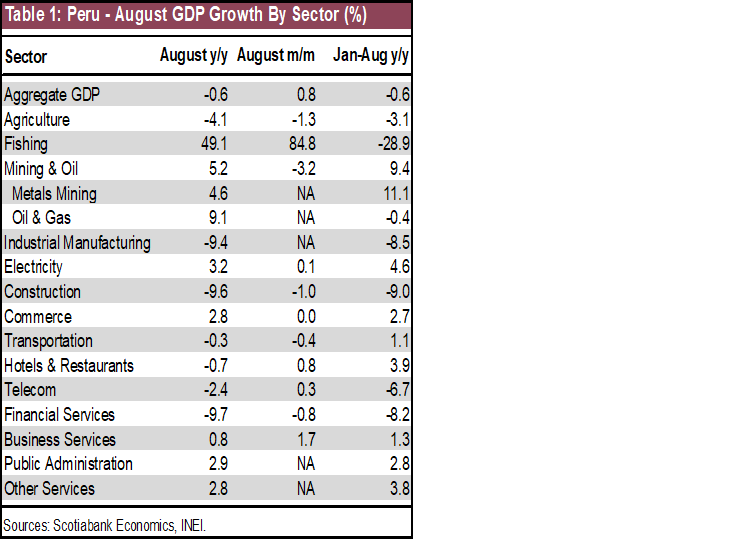

The 0.6% y/y decline in GDP in August released this weekend was unequivocally bad, with very little in terms of silver linings. August represented the fourth consecutive month of negative GDP growth, and, together with July’s 1.3% decline, means third quarter growth will be the third consecutive quarter of negative growth. Growth in the year-to-August was a solid -0.6%. Moreover, the figure means that our forecast of low albeit positive 0.5% GDP growth for full-year 2023 no longer stands up to scrutiny, and is now under revision.

What happened in August?

First, El Niño continued impacting agriculture. The sector’s 4.1% y/y decline in August was harsh and indicates no let up yet of climate events on agriculture. The fact that agriculture GDP also declined in month-on-month terms only adds to the degree of concern. As a reminder, though, low agriculture growth not only reflects severe weather, but also a dearth of fertilizer at the beginning of the crop planting seasons last year as a result of the Ukraine-Russia conflict. Up until the conflict, most of Peru’s imports of fertilizer came from Russia.

Fishing GDP rose to a strong 49% y/y, and one might be tempted to see in this figure the end of the El Niño impact on growth. If only. August is an off-season month for fishing, and the month’s strong showing was simply the effect of exploratory fishing off a very low y/y base. The end of the impact of El Niño on fishing is still a ways off.

Metals mining, this year’s heretofore formidable outperformer, only rose 4.6% y/y in August, well below the double-digit growth it had been displaying in previous months as the Quellaveco base effect begins to wear thin. The large Quellaveco copper mine came on stream in July 2022, and was just ramping up production in August.

And then there are the sectors that are linked to domestic demand. Both construction and industrial manufacturing continue to disappoint. Construction declined a hefty 9.6% y/y, still showing no improvement over its previous trend, as the decline in August was a tad worse than year-to-date growth. Worse yet, perhaps, was the evidence that month-on-month growth was negative.

Industrial manufacturing GDP (here called “manufactura no primaria”) also underperformed just as severely in August as in previous months, with no signs of a rebound (table 1).

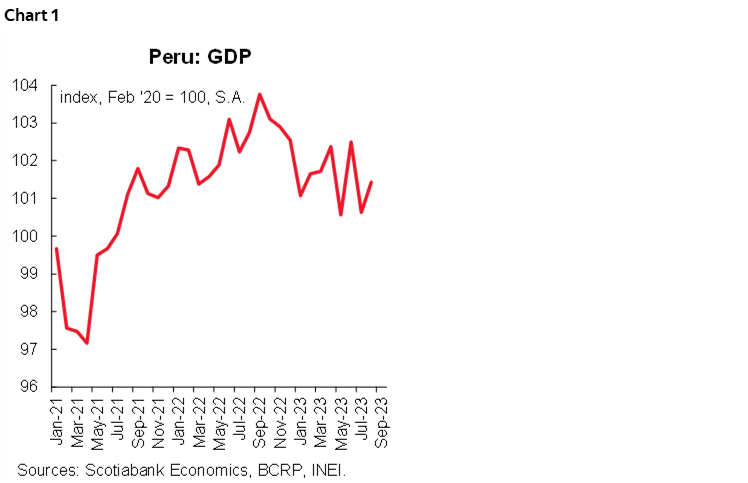

In seasonally-adjusted terms, the GDP index has been mired in the doldrums for a full year now, with nothing indicating that it will snap out of it for the remainder of the year. The chances for positive growth in 2023 are looking increasingly dim (chart 1).

So, where are the silver linings? Well, GDP did rise in month-on-month terms, up 0.8%. Although this improvement relied much too heavily on fishing GDP, which is not a dependable driver of growth. Lower impact sectors such as hospitality, telecom and business services did perform better in m/m terms than y/y, which is mildly hopeful, and even financial services seems to be moving towards stability. None of these are sufficiently indicative of domestic demand however.

Perhaps the most hopeful sign in terms of domestic demand actually comes from the job market. The unemployment rate in Q3 was 6.7%, up a tick from 6.6% in Q2, but down from 7.7% a year ago. More importantly, jobs growth was 5.3% q/q in September (4.9% y/y), and average pay was up 11.4% y/y, above inflation. In principle, these figures suggest that domestic demand should at least stop falling soon. However, for some time now the labour market dynamics appear to be somewhat divorced from GDP growth.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.