- Colombia: Citi Survey shows expectations split between a 25bps cut or a hold ahead of December’s monetary policy meeting

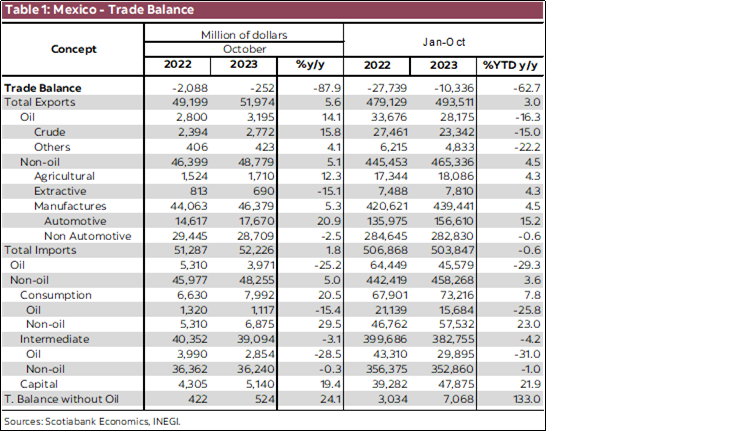

- Mexico: Trade balance recorded a smaller-than-expected deficit of USD252mn in October

The USTs rally kept going in Asia hours before European trading pumped the breaks on the decline in yields and with that helped the USD to broad-based gains while having limited impact on other asset classes. A combination (of uncertain weights) of short covering, momentum chasing, month-end, and taking the Fed’s Waller’s dovish comments yesterday a bit too seriously are all to blame for the rally. The G10 day ahead has German inflation at 8ET and US Q3 GDP revisions (where anything goes) 8.30ET, and some more central bank speakers, notably the Fed’s Mester; continue to keep an eye out for OPEC+ leaks.

USTs are rather evenly bid across the curve by 3–4bps. The increase in cut bets is also continuing today, as markets add another 5bps to end-2024 Fed cuts to see a cumulative 110bps in reductions (the first one is seen in May). The USD is heading into Americas trading with positive momentum behind it but still sitting somewhat mixed against the majors. The MXN is down 0.1/2% (aligned with the EUR and JPY) to undo Tuesday’s equally small gains. SPX futures are about 0.3% higher. Oil is tracking a solid 1.5% rise to its best levels of the week—and in fact its best levels since the OPEC+ meeting was postponed on the 23rd—as traders shake off some OPEC disagreement fears ahead of tomorrow’s gathering. Iron ore is up 0.9% (usual China story) and copper is only about 0.3% higher (after a 1.3% rise on Tuesday on supply tailwinds, see Panama and Peru).

Today’s Latam calendar is fairly quiet and the only marginally data point of note, Chilean unemployment rate, already came in line with consensus (at 8.9%); note Congress approved the 2024 budget bill yesterday. The release of Banxico’s quarterly inflation and economy report at 13.30ET may outline in greater detail the bank’s outlook—and may reinforce their recent less hawkish guidance. BanRep’s Gov Villar also speaks at an event on the 2024 outlook. From a regional standpoint, developments in Peru look like the most relevant for markets.

In Peru, workers at the Las Bambas mines began striking over pay yesterday, in a well teed-up move. According to the union, the copper mine is running at about a fifth of its capacity. The strike was originally set to last indefinitely but the union’s head said yesterday that because labor authorities declared the strike as improper it will now conclude tomorrow. As Fin Min Contreras highlighted yesterday, Peru would be in a deep recession were it not for the mining sector. Mining and hydrocarbons GDP has risen nearly 10% y/y in the year to Q3, compared to a 9%+ drop in construction, a 7% drop in manufacturing, and a sharp slowdown in leisure GDP (e.g. hotels and restaurants to Q3 grew 3.4% y/y ytd versus 30.4% y/y ytd in 2022).

That’s one (small) Peru risk out of the way (at least temporarily), but the other, the flinging of accusations between the attorney general and the president’s office continues as the former faces serious corruption and influence peddling accusations—and she accuses the president of being responsible for protesters deaths. In the meantime, Peru’s Congress is (conveniently) pushing through the approval of a seventh withdrawal of pension funds. While the government (and BCRP head Velarde) have opposed it, the executive seems to be throwing in the towel and coming to terms with the fact that lawmakers will pass at least a reduced version of initial plans in coming days.

—Juan Manuel Herrera

COLOMBIA: CITI SURVEY SHOWS EXPECTATIONS SPLIT BETWEEN A 25BPS CUT OR A HOLD AHEAD OF DECEMBER’S MONETARY POLICY MEETING

Citi’s November survey, which BanRep uses as one of its indicators for inflation expectations, the monetary policy rate, GDP, and the COP, was published on Tuesday, November 28th.

Key points included:

- GDP projections deteriorated amid a weaker-than-expected third quarter. The 3Q-GDP growth was released on November 15th posting an unexpected 0.3% y/y contraction, that could explain the deterioration in activity forecast for 2023 and 2024. For 2023, analyst consensus projects a 1.08% y/y GDP expansion, 13 bps lower than the previous month’s survey. On the other hand, GDP growth expectations for 2024 declined significantly (26bps) and now stand at 1.47% y/y vs the last expectation of 1.73% y/y growth. It is worth noting that despite projections assuming a mild acceleration in economic growth, projections have been deteriorating for eleven consecutive months.

- Inflation expectations were revised to the upside. On average, headline inflation is expected to be 0.48% m/m in November, bringing annual inflation to 10.20% y/y. Expectations for the end of 2023 rose to 9.53% y/y (+4 bps vs the previous survey), while expectations for 2024 increased to 5.20% y/y from 5.08% y/y in October. It is curious to see inflation expectations increasing since in the previous month CPI inflation results were below expectations. On the other side, higher inflation expectations for 2024 probably incorporate risks around indexation effects, regulated price increases, and “El Niño” weather phenomenon.

- Scotiabank Economics’ inflation forecast is lower than the analyst consensus. We estimate monthly inflation of 0.41% m/m and annual inflation of 10.08% y/y in November. During this month, we anticipate gasoline and utility fee prices will lead inflation to the upside, while food prices could remain under control. Tradable goods prices are also expected to give a breath in headline inflation amid lower FX and retailers giving discounts to customers.

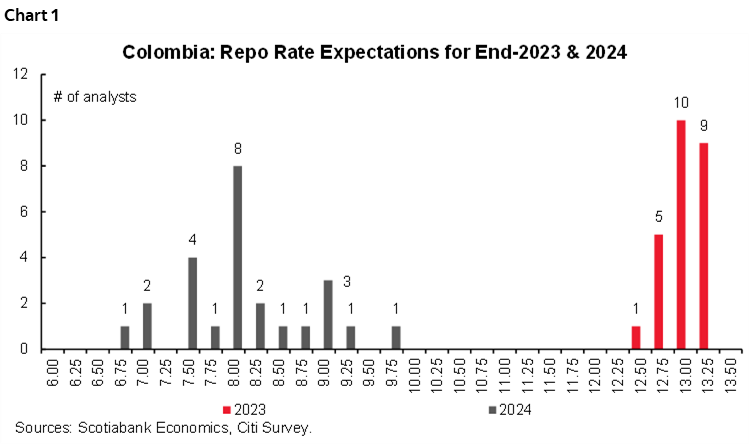

- Monetary Policy: opinions are very divided for December’s meeting: 10 out of the 25 analysts expect BanRep will kick off the easing cycle with a 25 bps rate cut; however, 9 out of 25 analysts expect a rate hold at 13.25%. Only 5 analysts expect a 50 bps rate cut and one expects a 75 bps cut to 12.5%. For 2024, the monetary policy rate is expected to close at least 350 bps lower, the median expectation is at 8% (a 525 bps cumulated cut).

- In Scotiabank Economics, we still see the possibility of having the first rate cut in December, however, it strongly depends on further inflation correction and more evidence of economic weakening.

- Finally, the exchange rate is projected to average USDCOP 4,113 by the end of 2023 (compared with USDCOP 4,179 in October) and USDCOP 4,148 by the end of 2024 (compared with USDCOP 4,156 in October). Scotiabank Economics projections are still pointing to a 4250 pesos exchange rate for December 2023 and 4316 pesos for 2024.

—Sergio Olarte & Jackeline Piraján

MEXICO: TRADE BALANCE RECORDED A SMALLER-THAN-EXPECTED DEFICIT OF USD252MN IN OCTOBER

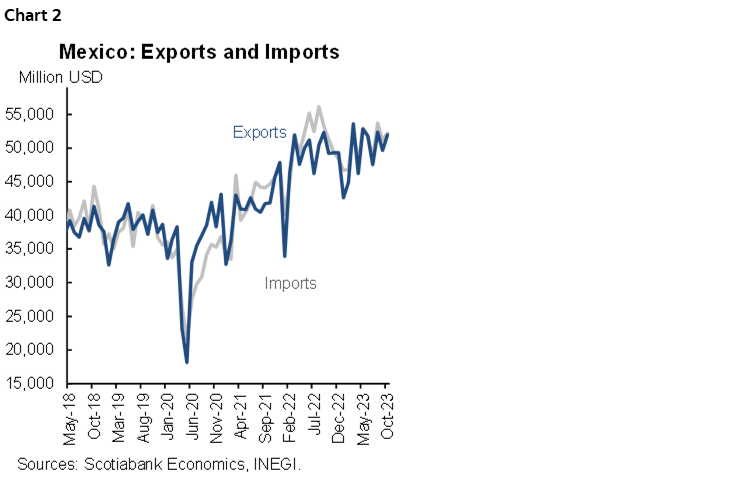

In October, the trade balance reported a deficit of -$252.5 million dollars (chart 2), from -$1,481.38 million in September. Imports rose 1.8% y/y (-3.9% previously), highlighting capital imports 19.4% (19.6% previously), and consumer imports, which increased 20.5% (10.3% previously), while intermediate goods dropped -3.1% (-8.8%). Exports bounced back to 5.6% y/y (-5.1% previously), as manufactures rose to 5.3% (-6.6% previously), and automotive exports rose 20.9% (3.7% previously). On a cumulative basis, the YTD deficit was -$10,336 million (table 1). On the other hand, the deficit of the oil balance was -$776.2 million dollars, while the non-oil balance obtained a surplus of $523.7 million.

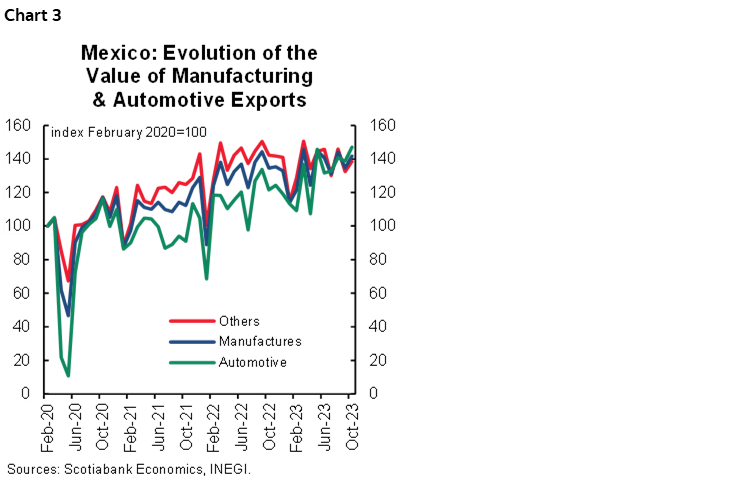

During this year, the automotive sector has been driving exports as numbers have rose 15.2% YTD (table 1 again). However, manufactures started the year very strong and have moderated slowly to a cumulative annual increase of 4.5% YTD. On the other hand, agricultural and non-oil extractive exports have remained more stable (+4.3% in both cases YTD), while oil exports face a -16.3% YTD drop.

On the import side, cumulative numbers have remained negative in the last three months, with a -0.6% YTD drop in October. The decrease comes from a -4.2% drop in intermediate goods, despite a 21.9% YTD soar in capital goods and a 7.8% in consumption goods.

In the short term, we expect similar results, with imports driven by consumption and capital goods, and autos leading total exports (chart 3). We believe the current USDMXN, as well as positive expectations for economic activity will hold positive numbers for imports, whereas manufactures and especially autos will remain benefiting from resilient demand in the US economy, as well as the advantage of the USMCA and its geographical position, also fostering expectations regarding nearshoring.

—Miguel Saldaña & Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.