- Mexico: Banxico minutes stands for a first cut in 2024Q1, but Deputy Governor Espinosa calls for caution; Inflation rebounded in the first half of November; services continue to persist

MEXICO: BANXICO MINUTES STANDS FOR A FIRST CUT IN 2024Q1, BUT DEPUTY GOVERNOR ESPINOSA CALLS FOR CAUTION

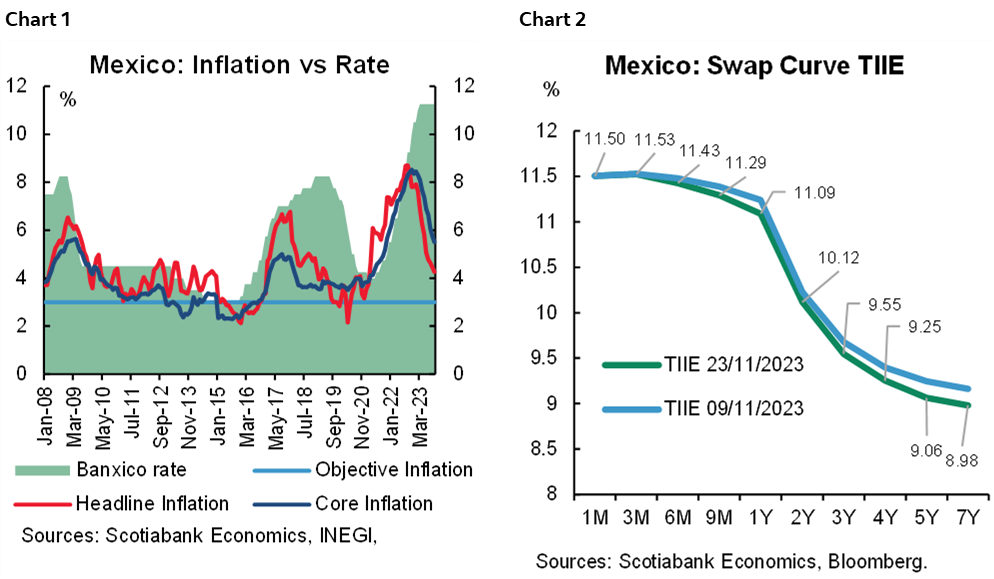

Banxico minutes for November’s monetary policy meeting showed a more dovish tone than statement. Several members were of the opinion that the disinflationary process is in a better position than a year earlier, despite uncertainty and a still upwardly biased balance of risks. Overall, the consensus of the Governing Board considers it appropriate to begin the downward cycle gradually in the first quarter of next year, in line with private expectations. However, we highlight the dissenting opinion of Deputy Governor Irene Espinosa, who advocates maintaining a cautious tone in a scenario in which inflation risks have increased in recent months.

Regarding the current economic outlook, members highlighted the behaviour of inflation since the second half of 2022. In this regard, some members recalled the different trends in the core components, where merchandise has presented a straight decline, but services presented a marked stickiness, and a rebound in the latest prints. Most members continue to expect inflation to converge to target in the second quarter of 2025. Despite this, the Board considered that the balance of risk remains skewed to the upside.

Members had different opinions on changes in the balance of risk; Deputy Governor Espinosa based her dissenting opinion on the strength of economic activity, the cyclical position of the economy, the tightening of the labour market, the persistence of core inflation, the recent upward trend in non-core inflation, inflation expectations above the target, and a procyclical fiscal policy, all of them increasing the bias at the time of the meeting. On the other hand, another member considered that the balance has improved with respect to March. Another member, in a more dovish tone, argued that classifying the balance of risks as biased to the upside at the current environment implies that inflation could decline more gradually than expected, while last year, the balance of risks implied the possibility of greater increases in inflation.

Regarding forward guidance and the future of monetary policy, most members considered that the first interest rate cut could take place in the first quarter of 2024. In addition, there was some consensus regarding the uncertainty in the outlook, so several members considered important to remember that future decisions will remain data-dependent, as adjustments could be gradual and spaced as inflation could present setbacks in a still complicated outlook. Some members also pointed out that the lack of coordination between fiscal and monetary policy could delay the effects of the restrictive stance and complicate the normalization of monetary policy.

Lastly, we agree with Deputy Governor Espinosa’s dissenting opinion, where she underlines that the disinflationary process has slowed down in the second half of the year, and stressed the importance of maintaining a cautious forward guidance in light of a still uncertain environment, and a balance of inflation risks more biased to the upside.

INFLATION REBOUNDED IN THE FIRST HALF OF NOVEMBER; SERVICES CONTINUE TO PERSIST

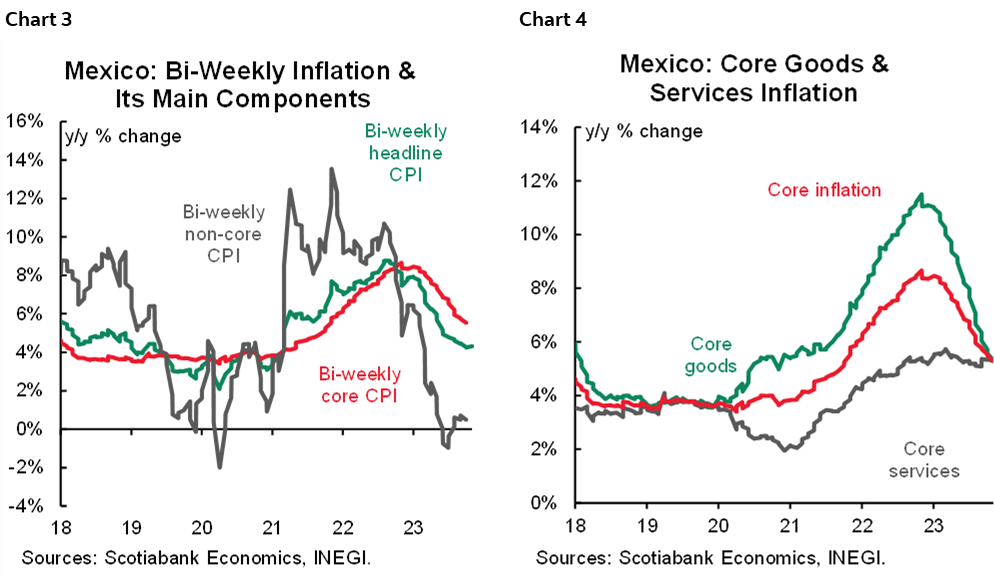

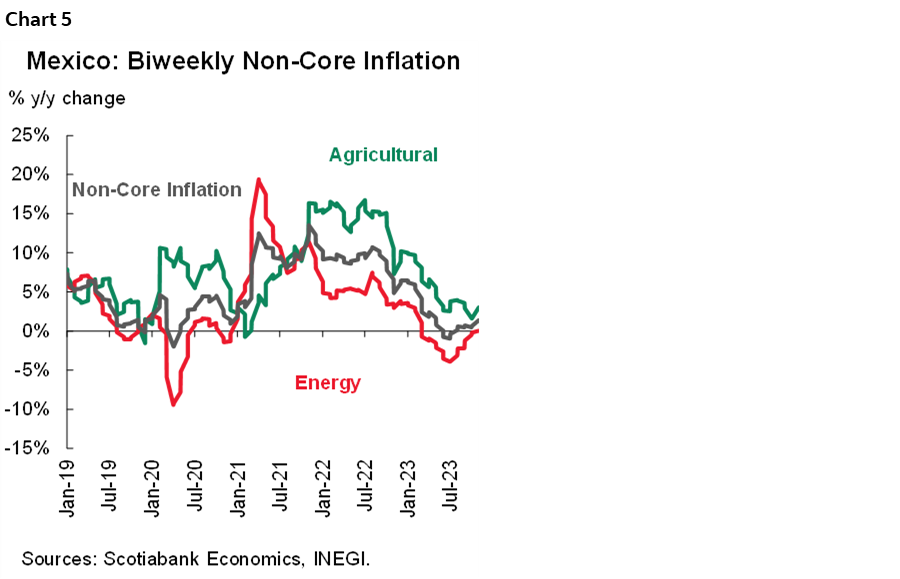

In the first half of November, inflation edged up to 4.32% y/y from 4.27% y/y (vs. 4.31% consensus), see chart 3, while core inflation slowed down from 5.54% y/y to 5.31% y/y (vs. 5.33% consensus). Merchandise decelerated 5.32% y/y (previously 5.55%), and services 5.28% y/y (previously 5.35%), see chart 4. On the other hand, non-core inflation increased 1.41% y/y (0.64% previously), see chart 5, highlighting energy and government tariffs, which rose for the first time in 15 months at 0.05% y/y (-0.19% previously). In its biweekly sequential comparison, headline inflation increased to 0.63% 2w/2w (0.13% previously, 0.58% consensus), while the core component rose 0.20% 2w (0.18% previously, 0.21% consensus) and the non-core 1.96% from 0.0%.

During the year non-core months have contributed significantly to the headline inflation downwards trends (chart 3 again), however, looking at recent setbacks, we consider that non-core items could pose some problems in the short term, owing to occasional setbacks in headline inflation, as core inflation could face some stickiness although still with a downward trend (chart 4 again). These results reinforce the perspective that we have presented for a few weeks on a rebound in inflation by the end of the year, hoping that it will be reflected in the upcoming monthly prints, due to increases in non-core inflation.

—Miguel Saldaña & Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.