- Mexico: Retail sales moderated their rise in September, while wholesale sales showed a strong increase, highlighting intermediation and vehicles; Citibanamex survey showed multiple rates scenarios for 2024

Closed Treasury markets with US and Japan holidays saw quiet trading in Asia hours with a bit more activity in Europe on the release of better than expected PMIs in the Eurozone and the UK. The G10 day ahead is very quiet aside from ECB meeting minutes and speakers. In Latam, the highlights are Mexican H1-Nov CPI at 7ET and Banxico’s meeting minutes at 10ET, accompanied by Peru Q3 GDP data after the close.

SPX futures and Eurozone and UK indices are all little changed, while UST futures and EGBs are bear steepening against bear flattening, very weak, gilts on a strong PMIs beat. The PMIs beat has the GBP leading all key majors with a 0.5% rally in a widespread dollar-negative market where the MXN finds itself lagging with only a 0.1% rise. In the commodities space, oil has been chopping around between the $76 and $77/bbl in WTI, sitting 1.0% lower at writing, but still about $2.5/bbl higher than yesterday’s lows on OPEC’s meeting postponement. Iron ore is off 1%, in contrast to a 0.5% rise in copper.

Mexico’s bi-weekly H1-Nov inflation is expected to print an unchanged to slightly higher headline of 4.2/3% but a slight deceleration in core inflation to 5.3% from 5.5%; still all too high, especially in services running around 5.3%. Banxico’s November meeting minutes will likely be more interesting for markets. At this decision, the bank surprisingly tweaked guidance on the time that will be spent at the rates peak, switching from the overnight rate having to remain at 11.25% “for an extended period” to “for some time”. The minutes may shed some light on why officials favoured this language tweak which has raised the odds of a Q1 rate cut versus those of a Q2 cuts start.

Monthly data showed that Peruvian GDP fell a surprisingly large 1.3% y/y in September (see Latam Daily), exceeding our already more negative than consensus forecast of a 0.8% drop. It was a particularly worrying result, considering that weakness was not simply concentrated in El Niño-impacted primary sectors, but spread throughout domestic demand industries, especially manufacturing and construction. With the monthly data at hand, Peru’s economy contracted for a third consecutive quarter, by 1.0% y/y in Q3 according to our economists’ estimates—in line with the median of forecasts submitted to Bloomberg. Today, plenary Congressional debate will begin on the 2024 Budget that needs to be approved no later than November 30.

—Juan Manuel Herrera

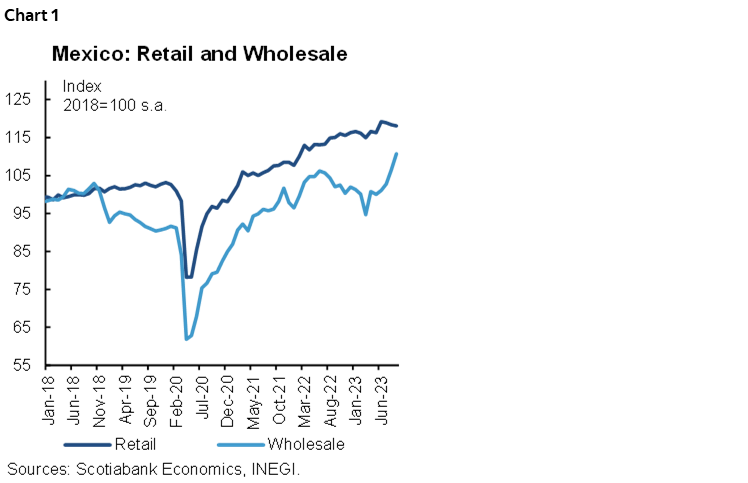

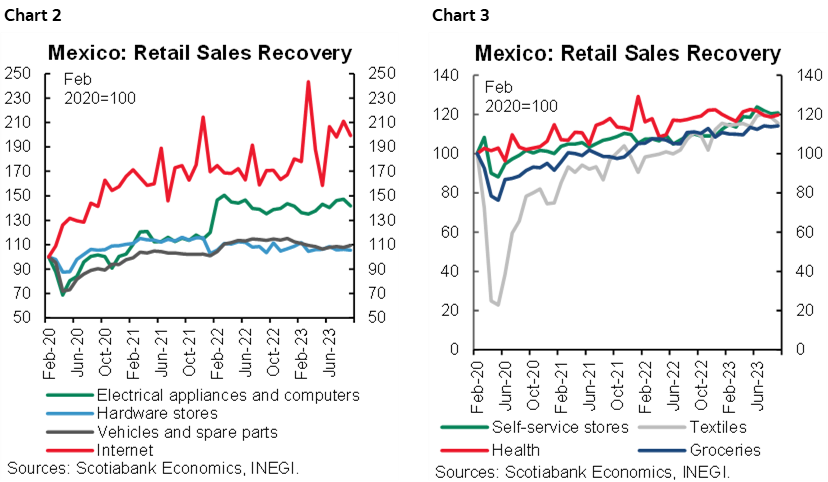

MEXICO: RETAIL SALES MODERATED THEIR RISE IN SEPTEMBER, WHILE WHOLESALE SALES SHOWED A STRONG INCREASE, HIGHLIGHTING INTERMEDIATION AND VEHICLES

September retail sales moderated their pace to 2.3% y/y from 3.2% previously. By components, trade in groceries remained at 2.8%, textile products slowed down to 4.1% (previously 10.7%), self-service and department stores increased to 11.4% (10.1% previously), health care 1.2% (0.3% previously), while the deepest drop was in recreation and personal use items at -11.5% (4.6% previously). In its monthly comparison, sales fell -0.2% m/m from -0.5% previously, with five of its nine components in the negative. On an annual basis, wholesale trade increased to 7.1% y/y from 2.8%, the largest increase was in intermediation at 46.9% y/y (19.4% previously) and vehicles at 22.6% (14.8%), while the deepest drop was textiles at -8.7% (-16.9% previously). On a monthly basis, wholesale sales increased to 3.9% m/m from 3.6% previously.

In the cumulative comparison, data contrast a little since retailers have grown from January to September 4.3% YTD, and the most relevant components have been in department stores (10.2%), internet (14.9%) and textiles (15.3%). On the other hand, wholesalers recorded a cumulative annual fall of -1.1% YTD, with the deepest falls being in raw materials (-5.1%), food (-2.3%) and textiles (-0.1%), however, it seems that the trend is to converge with retailers in the coming months, after having shown 5 months of negative annual change so far this year.

The perspective is that sales will slow down in the short term according to the effect of the monetary policy rate, mainly retail sales, while wholesale sales may continue with their upward trend for a few months, due to the high growth shown during this year. However, we consider that retail and wholesale will both benefit in 2024 by the increase in public expenditures published in the 2024 economic package, in line with our expectation of strong economic activity in the first half of the year.

CITIBANAMEX SURVEY SHOWED MULTIPLE RATES SCENARIOS FOR 2024

In the Citibanamex Survey, the average response points to slightly lower inflation at the end of the year at 4.61% (4.65% previously), and 4.05% (4.01% previously) in 2024. All respondents expect the rate to remain at current levels of 11.25% by the end of the year, and they expect the first cut to be in March 2024, at -25 bps, although two participants expect it could be -50 bps. By the end of next year, they foresee a rate of 9.25%, although with several possible scenarios in a range of 10.25%–8.0%. The average growth remained at 3.4% for this year and at 2.1% for 2024, although we anticipate that 2024 will be revised upwards in the next surveys. Finally, the average exchange rate rise was revised downwards by $17.83 ($17.93 previously) by the end of the year, and by 2024 at $18.70 ($18.73 previously), due to the recent strengthening of the USD/MXN.

—Miguel Saldaña & Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.