- Mexico: September industrial activity slows

- Peru: Peru’s new economic plan has good intentions, but private investment still faces obstacles

Markets are counting down the hours to the 8.30ET release of US CPI data, with a slightly positive mood in European hours across rates, currencies, and equities. The overnight data run was inconsequential and this morning’s UK employment report mostly came and went with limited market impact aside from a slight underperformance of gilts that has faded in recent trading. BoE, Fed, and ECB speakers are also on tap in the G-10 while we continue to monitor US government funding developments. Colombian and Canadian markets reopen today after holiday closures on Monday.

USTs are bull flattening, as are EGBs but in more contained fashion. The USD is chopping around trading on nothing too obvious during the Asia/Europe crossover and beyond to sit 0.1/2% firmer against high-beta FX like the CAD and NOK versus 0.2% weaker against the EUR and GBP. Crude oil is unchanged to marginally firmer, while copper and iron ore add 0.3/4% with a small tailwind from China reportedly considering housing stimulus. SPX futures are up about 0.2% in line with ESX gains and a 0.3% lower FTSE.

The MXN is leading the majors, up 0.3%, to almost erase the lurch lower on Banxico’s less-hawkish decision last week to sit at ~17.55 at writing. Yesterday, in an interview to El Financiero, Banxico Gov Rodriguez said that the bank will not cut rates in December. This shouldn’t come as any surprise, but the governor also showed her dovish hand, noting that the expected progress in inflation “may allow to start discussing the possibility of adjusting our reference rate downward already in the next meetings”. That suggests Rodriguez is favouring a Q1 rate cut—which already was the pre-decision median in surveys.

At 6:30ET, we get the BCCh’s October 26 meeting minutes. Recall that at last month’s decision Chilean officials unanimously chose to reduce the overnight rate by 50bps to 9.00% and suspended the bank’s reserves replenishing program, surprising most with the cut size (vs 75bps) and changes to FX policy. Today’s minutes risk being stale, however, since the meeting took place before the release of an encouraging October inflation print (see our take here) that helped a rally in Chilean rates.

The main thing to look for in today’s minutes will be what may prompt the BCCh to go back to a 75bps cut at its December decision. The smaller 50bps cut in October was preferred due to, at the global stage, “a deterioration in financial conditions, with a combination of real, financial and geopolitical risks”, with “the escalating tensions in global financial markets” prompting adjustments in FX policy.

Since October 26, US 10-yr yields have fallen 30–35bps and oil is down about 10%. International financial conditions have, on net, eased and spillovers from the conflict in the Middle East seem relatively contained and oil prices are less of an inflationary risk. In early-November, the CLP closed as high as ~6.5% vs the USD from its pre-decision levels, in a clear reflection of the suspension of dollar purchases and some broad USD weakness. But the CLP is now only about 1% stronger since the decision (partly as copper remains soft) which may motivate continued caution by the BCCh.

Colombia’s DANE will publish retail sales and industrial/manufacturing production data at 10ET, which are expected to show another year-on-year contraction across all three indices. Today’s figures will help us refine forecasts for tomorrow’s Q3/Sep GDP/economic activity data that we expect to show a relatively soft 0.4% q/q GDP rise that makes up less than half of the 1.0% q/q contraction in Q2. Brazil’s IBGE also publishes services sector data at 7ET ahead of Friday’s economic activity reading for Sep where a small rebound from a large 0.8% m/m decline is expected.

—Juan Manuel Herrera

MEXICO: SEPTEMBER INDUSTRIAL ACTIVITY SLOWS

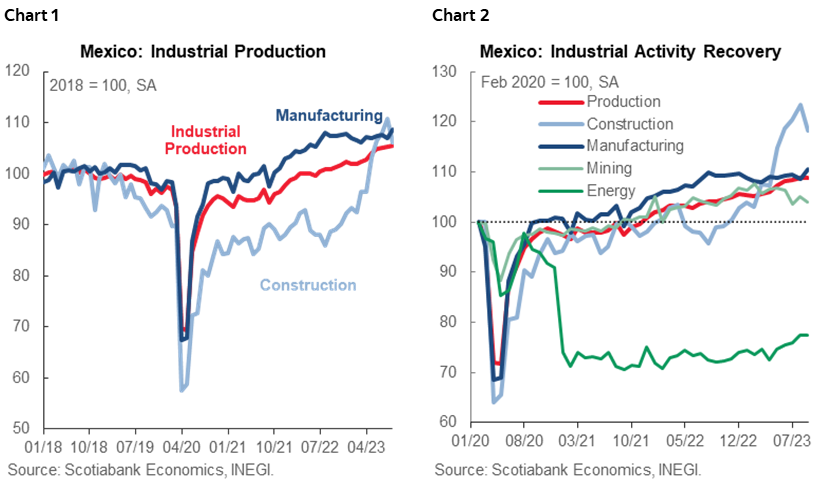

In September, industrial activity growth moderated to 3.9% y/y from 5.2% previously, with construction up 18.6%, utilities up 7.0%, manufacturing down 0.8% and mining down 0.5%. In the monthly comparison, it moderated slightly to 0.2% m/m from 0.3% previously, with seasonally adjusted monthly figures. Construction fell -4.1%, manufacturing increased 1.7%, while utilities decreased -0.2%, and mining -1.0%. On the other hand, in the January–September period, production recorded a 3.7% YTD increase.

In the short term, we think construction will remain with strong annual increases, as the emblematic public construction projections have yet to be finished in 2024, before the end of the current administration. Keep in mind most of the advances in construction come from non-residential projects, as well as in the public component. On the other hand, the manufactures could remain somewhat plain in the coming terms, except in the auto sector, where increases in demand side indicator suggest production will have still an important dynamism, as it gets closer to record levels. Lastly, we also highlight the weak performance of utilities, as the component we not recovered from the pandemic, suggesting also a lack of investment in the sector. In the future, in order to remain with a positive investment trend in key manufactures sectors owing to nearshoring, we think it will also be necessary to increase first the utilities supplies, as energy is a key factor to consider in the expansion or establishment of manufactures plants owing to nearshoring.

—Miguel Saldaña

PERU: NEW ECONOMIC PLAN HAS GOOD INTENTIONS, BUT PRIVATE INVESTMENT STILL FACES OBSTACLES

The government, led by Finance Minister Alex Contreras, announced yet a new economic stimulus plan on November 10th. Like previous plans, the new one heads in the right direction, and is in general helpful, but falls short of doing enough to stimulate private investment, which is what the country needs to boost robust and sustainable growth.

The plan is called “Plan Unidos” (Plan “we’re united”). The change in name from the previous “Con Punche Peru” plans seem to be a tacit admission that those earlier plans did not have the impact that was hoped for. The overall intention of the government with the new plan is to attain 3% GDP growth, purportedly as a first stepping stone to 4%–5% growth.

Some of the main elements of the new plan include:

- PEN 15bn (USD4bn) in funds for small and micro businesses. In reality a PEN 10bn increase in an already existing program.

- PEN 1bn (USD270mn) to mitigate the impact of El Niño on agriculture. Interestingly, agroindustrial companies are included in the plan. Past plans focused on small farms, leaving agroindustrial firms to fend for themselves.

- PEN 200mn (USD54mn) for low-income housing. Also an expansion of a current program.

- Unblock four large-scale irrigations projects which have been on pause for some time. If successful (precedents aren’t favourable, but hope springs eternal), the projects could give a significant boost to agroindustry in future years.

- PEN 1bn (USD270mn) for development projects in the Amazon.

- PEN 890mn (USD237mn) in projects to help convert Peru into a regional seaport hub, including the Callao-Ancón-Chancay port axis, and strengthening the local shipping and port logistics industries.

- PEN 200mn (USD54mn) in temporary jobs programs.

- Expedite USD1.58bn in electricity infrastructure projects. This does not seem to imply an actual increase in spending, however.

- Tender USD8.0bn in public-private projects (PPPs) in 2024. This would be the greatest PPP tender program in years. We are cautiously hopeful on this, as the government successfully tendered USD2.3bn in PPPs in 2023. Note, however, that many of these projects may have a long gestation period.

- Measures to promote tourism, including expanding and improving the Lima and regional airports.

- A “taxes for services” program (“servicios por impuestos”). The facility would presumably mimic the partially successful “obras por impuestos” (tax deductions for public infrastructure investment) that currently exists. The program would allow companies to finance public health and education services, and deduct these costs from taxes.

- Measures to promote and accelerate mining investment projects.

- Expand the 2024 budget expenditure to include PEN 5.5bn in infrastructure maintenance. This is 8% greater than the 2023 budget, which is no larger than normal budgetary increases of the past. The difference, perhaps, is the intention to concentrate the spending in the first half of the year so as to have a greater impact on growth.

The plan also includes certain initiatives that will take longer to bear fruit, including develop a petrochemical industry, and renewable energy projects.

One gets mixed feelings regarding the potential of the program to make a difference. On the face of it, the plan seems quite ambitious. At the same time, many of the measures are simply an expansion of ongoing programs, or a more detailed enumeration of things that the government was already known to be working on. This gives a certain sensation along the lines of been there, seen that. And yet, the magnitude and breadth of the measures give pause for thought. One example of the difficulties in assessing the plan: while the government in general is seeking to expedite a long list of investments, both ongoing and planned, which is all good and well, the quid lies in the capabilities of the authorities and institutions involved to successfully execute the investment projects.

One of the stated intentions of the plan is to accelerate GDP growth, initially to 3% and eventually to 4%–5% growth. This suggests that the government conceives the plan as at least in part a Keynesian stimulus program. But the plan also has a longer term view given its intention to transform the regulatory and investment environment that the State provides for private business. The plan doesn’t talk of reform but, rather, suggests piecemeal measures. Most of the measures are small in scale. But, at the same time they add up and up. The plan falls short of being a shock program that would lead private business to think that this time is different and, therefore, to rush to invest. However, it could, if well executed, provide for an incremental incentive over time for private investment to rise slowly but surely, as regulatory blocks are removed, and more and more APPs and infrastructure projects are tendered.

The main problem is that it won’t be quick. And Peru needs a bit of speed. Especially considering that, in Peru, politics does tend to move quickly, which poses a threat in itself.

It's not clear that the government could do more in increasing spending. Even before this plan was announced we did not expect the government to comply with the legal fiscal deficit rule either in 2023 or 2024. It is also not clear how much more could be done in expediting infrastructure projects, or changes in regulations. But where the government could definitely do more is in stimulating mining investment. Minister Contreras mentioned hopes to activate USD4.6bn in mining investment projects, mainly through easing regulations and reducing regulatory approval times. That might work in normal times. But Peru already has a series of large-scale mining investment projects, such as Tía María, that a ready to go ahead, and are stymied, not by regulatory issues but due to social issues. The government apparently feels it is too weak to take on the challenge of give these large investment projects its support.

The plan is not a bad one, but it is not likely to be enough to aggressively stimulate private investment. The political environment is too strong an obstacle. Under a different political context, the package would be much more beguiling.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.