- Chile: Right wing gains more than three-fifths of Constitutional Council; ability for dialogue will be key to present a Constitution that will be approved

- Colombia: Headline inflation peaked, and core inflation stabilized, paving the way for rate stability in June

CHILE: RIGHT WING GAINS MORE THAN THREE-FIFTHS OF CONSTITUTIONAL COUNCIL; ABILITY FOR DIALOGUE WILL BE KEY TO PRESENT A CONSTITUTION THAT WILL BE APPROVED

On Sunday, May 7, the election of the Constitutional Council took place, where 51 councillors were chosen under a mandatory voting system. The election pacts, or lists, formed for this election were the following: (i) Partido de la Gente (center); (ii) Todo Por Chile (moderate left): PR, PPD and DC; (iii) Partido Republicano de Chile (extreme right); (iv) Unidad Para Chile (extreme left): Socialist, Communist and Government coalition; (v) Chile Seguro (moderated right): RN, UDI and Evopoli.

Preliminary results (95% of the votes) give 33 seats to right-wing parties, of which 22 were won by the Republican Party (extreme right), gaining the ability to block proposals. On the other hand, the pro-government parties (Unidad para Chile) obtained less than the two-thirds (17 seats in total), with no veto power.

In light of these results, the parties of the government alliance have the great challenge of generating and achieving dialogue with the right-wing parties within the Constitutional Council.

In our opinion, if the necessary dialogue to discuss left-wing proposals is not achieved, the probability of having a new rejection of the Constitution in December could increase.

Overall, the Republican Party (Partido Republicano) obtained 36% of the votes, followed by Unidad para Chile with 28%. Chile Seguro obtained 22% of the total votes. Meanwhile, Indigenous Peoples obtained 1 seat in the Council. Thus, the Constitutional Council will be composed of 51 members. Also noteworthy is the absence of the People's Party (Partido de la Gente) in the Council, as well as the traditional moderate left (Todo por Chile) and the independents, all without participation in the Constitutional Council.

The elected Council will begin its work on June 7, considering the final draft issued by the Commission of Experts. Finally, the exit referendum will take place on December 17.

Market reaction: due to the high vote in favor of right-wing parties (obtaining 33 seats), we anticipate favorable impacts on local assets: CLP appreciation, stock market gains and falling short-term interest rates. In our opinion, the positive evolution of local assets in the medium-term will depends on the ability of the Constitutional Council to draft a Constitution that can be approved in the next electoral process.

—Aníbal Alarcón

COLOMBIA: HEADLINE INFLATION PEAKED, AND CORE INFLATION STABILIZED, PAVING THE WAY FOR RATE STABILITY IN JUNE

Colombia's pace of monthly CPI inflation was 0.78% m/m in April, according to DANE data released on Friday, May 5. The result was below expectations of the BanRep survey (0.87% m/m) and came well below Scotiabank Economics' projection of 1.16% m/m. Food inflation was the game changer this time. It posted the first monthly contraction since June 2021, replacing a high statistical base of 2022 (2.75% m/m), making the headline inflation finally peak.

Year-on-year headline inflation finally fell from its highest level since 1999, from 13.34% in March to 12.82% in April (chart 1), the lowest since November 2022. But additionally, Friday's data included a positive surprise since core inflation metrics showed more moderate increases. Ex-food inflation stood at 11.51% y/y, vs. 11.42% in the previous month, while ex-food and regulated inflation stood at 10.48%, falling from the last month's figure of 10.51% y/y. On that front, we observed some tradable goods decelerating, and other relevant services, such as hotels, also pointing to more moderate inflation.

Friday's results are very positive, and we think this is the right signal BanRep expected to consider to pause the hiking cycle. Our call is for rate stability in the June meeting, at a 13.25%, lasting until October, when we expect BanRep would start to discuss rate cuts. On the other side, the signal we received from food inflation is encouraging since it finally reflects the moderation of input prices and the recent dynamic by the PPI. If it continues, it increases the probability of seeing lower-than-expected inflation by the end of 2023.

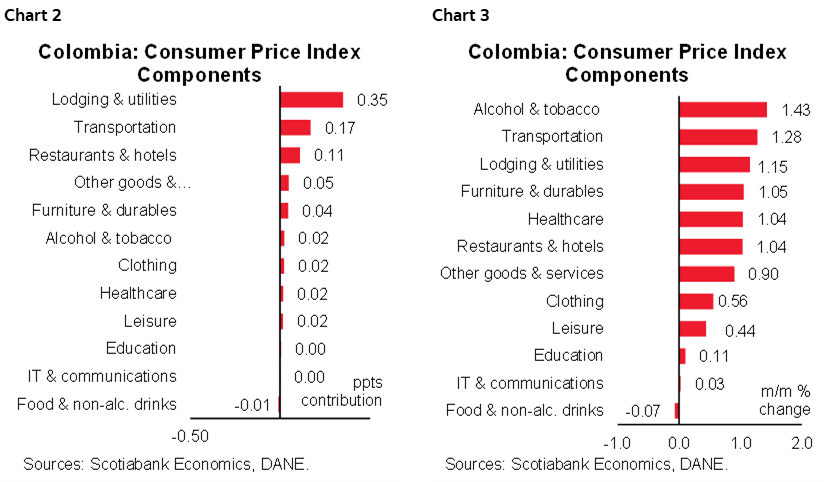

Looking at April’s numbers in detail, food inflation was the only group that showed monthly contractions (charts 2 and 3).

The highlights are:

- Foodstuff inflation posted the first contraction (-0.7% m/m) since June 2021, which is very positive news. In April, potatoes (-8.75% m/m), fresh fruits (-3.42% m/m), tomatoes (-2.18% m/m), and onions (-2.33% m/m) price contractions offset the gains in other prices, either way we observe that other items within the food group are showing deceleration. If inflation continues showing more moderate inflation in forthcoming months, the headline inflation could fall faster since the statistical base effects from 2022 were very high. The only risk to the upside that we are facing is a materialization of a strong El Niño Phenomenon that affects the food supply for the second half of the year.

- The lodging and utility group was the main contributor to the upside to monthly inflation (+1.15% m/m, and +35 bps of contribution). Rent fees continued increasing significantly (+1% m/m) due to indexation effects to December 2022 inflation. Utility fees increased again (+1.62% m/m), which strong contribution from water fees (+3.1% m/m), and electricity fees (+1.69% m/m).

- The second most significant contributor to headline inflation was the transportation group, showing a 1.28% m/m figure and a contribution of 0.17 ppts to overall inflation. Gasoline prices (3.36% m/m), vehicle prices (0.98% m/m), and air tickets (+1.98% m/m) are leading to the still strong upside pressure of the group. It is worth noting that vehicles sales are moderating significantly, showing double-digit contraction vs 2022, which could contribute to moderate inflation in the vehicles sector. In the case of gasoline prices, those are expected to continue increasing since the current price is at 11767 pesos, and the finance minister is talking about taking It to 16000 pesos per gallon.

- In April, goods inflation decreased from 15.08% m/m to 14.32% m/m, signaling the moderation of food prices and some tradable items. In the case of services inflation, it increased from 8.73% y/y to 8.98% y/y, which is related to the indexation effects observed in some items that are labour intensive.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.