- Colombia: Citi survey: Economist consensus points to stability in monetary policy rate in June

Overnight markets extended yesterday’s weakness on the lack of progress in US debt ceiling negotiations with SPX futures tracking a 0.4% decline, in contrast to modest moves in Treasury markets as the UK’s CPI beat motivated a jump in global yields. The USD is broadly stronger, and getting stronger over the past hour, while crude oil sits on a near 2% gain on the day contrasting with further losses in iron ore (-4.5%) and copper (-1.5%)—with the former again reflecting worrying Chinese steelmaking demand dynamics.

The MXN is the only major currency holding up well against the USD, as it aims to end a six-day streak of losses (with some political risk weighing on sentiment) thanks to a 0.2% gain at writing. Mexico’s INEGI publishes H1-May CPI data at 8ET, where the median economist polled by Bloomberg and us expect a deceleration of 0.1–0.2ppts in both core and headline inflation (consensus at 6.13% and 7.49%, respectively). The slowing of inflation supports Banxico’s on-hold stance, but with this decline still being moderate (particularly in core) it also supports the bank’s guidance that rates will remain elevated for a considerable time (as expected by economists that see rate cuts starting no sooner than December).

April Chilean PPI and Colombian Industrial/Retail confidence data are also due for release today though we don’t anticipate markets to react to these prints, and the global market mood surrounding the debt ceiling discussions will remain in the driving seat. Chile’s central bank president Costa speaks to a Senate committee today at 10.30ET with the publication of the BCCh’s Financial Stability Report today.

—Juan Manuel Herrera

COLOMBIA: CITI SURVEY: ECONOMIST CONSENSUS POINTS TO STABILITY IN MONETARY POLICY RATE IN JUNE

The results of the May Citi economists survey, which BanRep uses as one of its measures of inflation expectations, monetary policy rate, GDP and COP, was published on Tuesday May 23.

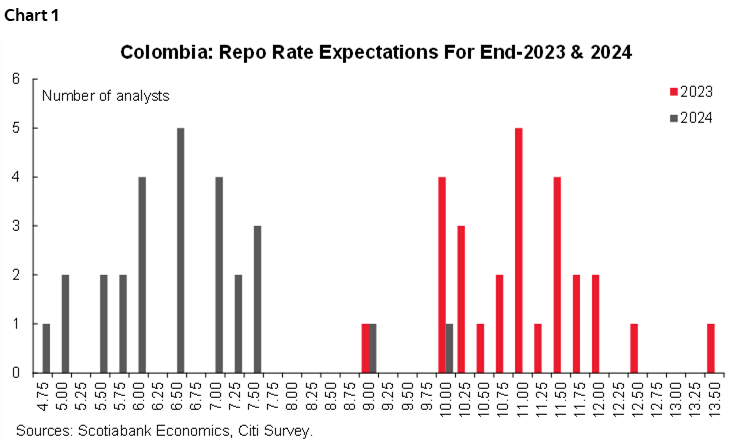

Key points:

- Economic activity projections improved for 2023 but weakened for 2024. For 2023, it is estimated at 1.13% (+8bps vs previous survey), while the rebound expected for 2024 was revised to the downside for the fifth month in a row and now is at 2.16% (previous 2.28%).

- Inflation will affirm its downward trend in May. Analysts expect May’s monthly inflation rate at 0.63% m/m on average, which will make the headline inflation go down from 12.82% to 12.58%. By the end of 2023, inflation is expected at 9.08% (+3 bps vs previous survey), and by the end of 2024, it is expected at 4.96% (14 bps above the previous survey), which is still above the central bank target range between 2% and 4%.

- Scotiabank Economics is broadly aligned with consensus, with inflation expectations at 0.65% m/m and 12.60 % y/y. In May, inflation is expected to remain high versus historical standards (0.28% m/m pre-pandemic average), amid still high indexation effects, especially in rent fees. On the other side, gasoline prices, food, and regulated prices will continue to add pressure to the upside.

- For the June monetary policy meeting, 20 out of the 22 analysts in the survey expect rate stability at 13.25%, and two analysts expect a 25bps hike to 13.50%. For December 2023, expectations range between 10.50% and 13.50%, and the median is 11.75%. For December 2024, the expected range is between 5% and 10%, and the median response is 7 % (chart 1).

- USDCOP forecasts for December 2023 is at 4621 pesos (vs. 4682 pesos in the previous survey), while for Dec 2024 is at 4499 pesos.

—Sergio Olarte, Santiago Moreno, & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.