- Colombia: Monetary Policy Preview—BanRep to hike 25bps amid economic slowdown and moderated inflation expectations

It was a risk-on overnight session with no obvious catalysts for upbeat trading that is seeing SPX futures 0.8% higher on the day alongside a mixed USD. Strength in Chinese tech shares is being assigned the role of market cheerleader but even there the reason for gains seems relatively thin. Crude oil is stronger (1%) on the API’s inventory report (crude and gasoline inventories down sharply), iron ore is up 1.4%, and copper is gaining 0.5% in line with the optimistic mood.

The MXN is happy to ride the risk-on sentiment’s coattails to post a majors-leading appreciation of 0.5% and stringing five days of gains as it sets its eyes on the 18 pesos level. The MXN is ignoring (not unreasonably so) the resignation of Mexico’s electoral institute executive secretary yesterday, who left in protest of AMLO’s electoral reform (which called for his dismissal and placed him in the spotlight). Another day, another clash in the AMLO-INE saga. The market will keep its focus on tomorrow’s Banxico decision where a 25bps is widely expected while guidance around continued hikes will likely be the most relevant item for traders.

Currency strength is not unique to the MXN among its peers in the region, as all Pacific Alliance FX and the BRL have done well since mid-month. In fact, despite the noise in markets, the core Latam currencies we track have gained against the dollar in March from the COP’s top performance of 4.2% vs the USD to a still respectable gain of 0.8% in the PEN (despite impeachment noise); March-to-date, the CLP, BRL, and MXN are 3.7%, 1.4%, and 0.9% higher, in that order.

On the topic of Peruvian politics, prosecutors announced yesterday that they have opened an investigation into Pres Boluarte and former Pres Castillo (who ran together in 2021) on accusation of money laundering. This is in addition to an investigation (launched in early-January) of Boluarte regarding “homicide or genocide” due to civilian casualties during the latest period of social unrest. Note that Presidents in Peru may be investigated, but not charged, while in office. Still, the vote later this week on whether to allow a debate on impeaching the President in Congress may have got a slight additional tailwind—though numbers still look tilted against the proposal. We think this is all mostly noise.

—Juan Manuel Herrera

COLOMBIA: MONETARY POLICY PREVIEW—BANREP TO HIKE 25BPS AMID ECONOMIC SLOWDOWN AND MODERATED INFLATION EXPECTATIONS

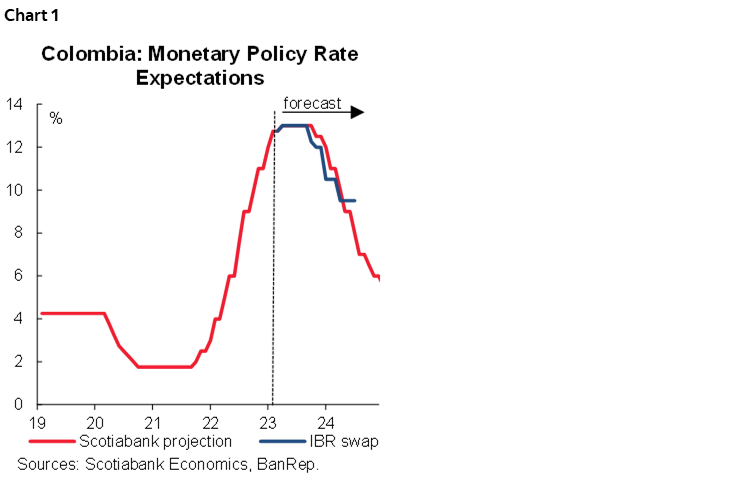

Tomorrow, BanRep is expected to deliver a 25bps hike to take its policy rate to 13%. Despite inflation not having reached a strict peak, inflation expectations 1Y and 2Y ahead are decreasing. In the meantime, the economy is showing signs of slowing, especially in formal sectors. Both fundamentals could contribute to the central bank affirming the end of the hiking cycle. A split vote signaling some members voting for stability and a communique revealing that the board is comfortable with the level of the interest rate would reinforce our base case scenario of a pause.

According to a recent survey, the economic analysts’ consensus expects a 25bps hike. The IBR market is pricing also a final 25bps hike and stability until August (chart 1). The Scotiabank Economics scenario is of stability after the March hike with cuts starting in October.

Key points ahead of Thursday’s BanRep vote:

- At January’s meeting, the board hiked by 75bps, below the market’s pricing and the economists' consensus. It was in a split vote, two members voted for 25bps, and the rest (five members) voted for a 75bps hike.

- In the minutes, the majority group said that a 75bps hike sends a message of compromise against inflation expectations and contributes to COP strengthening. The moderate group expressed stronger concerns about the economic activity slowdown, adding that the stickiness of inflation at high levels is due to supply shocks that are reducing.

- Inflation hasn’t reached a peak, however. January and February data confirms that inflation is transitioning towards a ceiling of ~13.3%. Statistical base effects are high and from our perspective it’s very difficult to see significantly higher inflation during the year.

- The good news regarding inflation comes from inflation expectations. In the past two expectations surveys from the central bank one-year-ahead inflation expectations have decreased to now sit at 7.21%, while two years ahead is at 4.01%.

- On the economic activity side, the ISE index showed an upside surprise in January, expanding by 5.9% y/y (above expectations of 2.5%), reflecting high regional public spending in regions, which is common before local elections. However, the private side of the economy is slowing faster, credit expansion decelerated from 18% y/y to 15%, while other indicators such as vehicle purchases are contracting.

- Despite volatility in international markets, Colombian assets have been resilient. The COP has appreciated by 4% since mid-month, while the COLTES market is reflecting better liquidity and price action. Both components reduce pressure on the central bank.

We affirm our expectation of a 25bps hike that leaves the policy rate at 13%; however, a split vote tilted towards the dovish side could take place. In terms of market effect, we think that a 25bps hike is a consensus, but sending a signal of potential future stability would affirm the steepening mode in the curve as well as calm in the currency.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.