- Colombia: Economic activity expanded more than expected in January

The UBS acquisition of Credit Suisse announced yesterday had but a short-lived positive impact on the market mood in early Asia trading, as the full write-down of CS’s Additional Tier 1 (AT1) bonds triggers market anxiety (ESTX banks were down as much as 6.5% at some point, now down ‘only’ 1.0%). Coordinated action by the Fed and major central banks to increase the frequency of USD swap line operations (from weekly to daily) would also suggest officials are concerned about the adequate functioning of markets; yet, ECB, BoE, BoJ, and SNB operations saw little demand this morning.

SPX futures are marginally higher on the day, recovering losses in the European morning while global yields bounce back from intraday lows but rates markets are still holding a decent rally on the day (US 10s down 6bps). Crude oil is down 1.5–2.0% today, while iron ore is off about 4% but copper is 0.9% higher.

The USD is mixed as London hours see it somewhat weaken, with the JPY (+0.4%), enjoying the tailwind of lower US yields, while the MXN (down 0.6%), underperforms again, feeling the pain of risk-off trading and the pull from a lower rates outlook in the US. The Fed’s policy announcement on Wednesday is currently roughly seen as a toss-up affair between a 25bps increase and a rate hold.

This morning, Chile’s central bank released Q4 GDP data that showed a greater than expected decline in year-on-year terms of 2.3% compared to the Bloomberg median and our forecast of -1.6%. The country’s economy slightly expanded vs the previous quarter, but the minor 0.1% expansion missed the 0.6% consensus forecasts (small sample), coming off a 1.1% contraction in Q3 (revised from -1.2%). With that, Chilean GDP expanded 2.4% last year, below our team’s forecast of 2.7% which they expect will be followed by a 0.8% decline in output in 2023 (prior to today’s data). The weakening Chilean economy should prompt rate reductions from the BCCh soon according to our Santiago economists, who anticipate 675bps in cuts by year-end (from 11.25% to 4.50%) starting with next month’s decision. On a better note for the CLP, Chile’s current account deficit narrowed to USD5.0bn from USD7.5bn in Q3, and with this Q4 reading representing the narrowest deficit since Q2-21.

We have a quiet day ahead in Latam from a data perspective and the global market mood should continue to drive local assets. Mexican and Colombian markets are closed today. There’s a bit more off-calendar developments to monitor in Brazil, however, where we await further details on Haddad’s fiscal framework plans amid reports that others in Lula’s cabinet are opposed to certain components. The plan will likely influence the BCB’s guidance at its rate decision on Wednesday, where a hold is widely expected.

—Juan Manuel Herrera

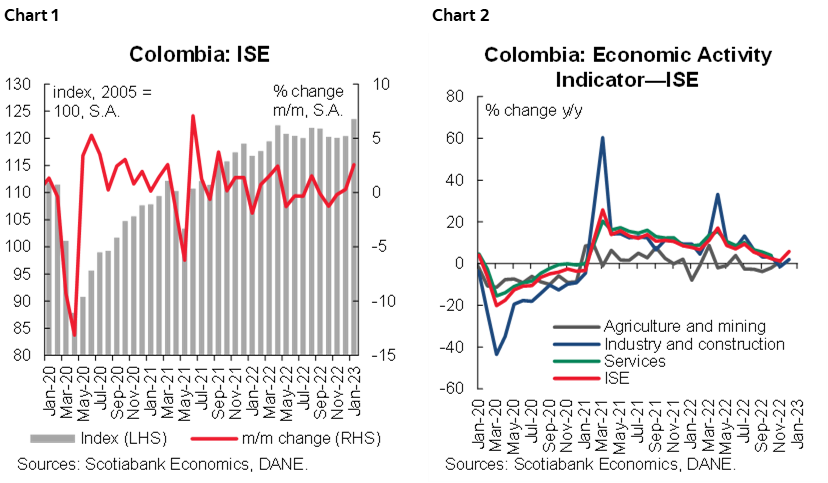

COLOMBIA: ECONOMIC ACTIVITY EXPANDED MORE THAN EXPECTED IN JANUARY

On Friday, March 17, the statistical agency (DANE) released the January 2023 Economic Activity Indicator (ISE) the main proxy for GDP, showing that economic activity in January expanded 5.85% y/y (chart 1), above the Bloomberg market consensus of 2.5% y/y. Sectors contributing to the positive annual reading in January were construction, manufacturing, trade and services. On a monthly basis, economic activity expanded 2.6% (chart 2), mainly due to better performances in the secondary and tertiary sectors.

Key Highlights:

- Primary activities (13% of the economy) expanded 0.94% y/y, showing a smaller deterioration compared to December (-2.0% y/y) but registering a contraction of 1.2% m/m. This may be explained, in the case of the agricultural sector, by the effects of the rains that continued to affect production in the midst of a coffee production that is beginning to recover, added to the persistent high prices in costs. For the mining sector, during January there was a drop in traditional exports, which could reflect lower coal production and even lags in oil production.

- The Secondary sectors (17% of the economy) increased 1.9% y/y and expanded 2.1% m/m, rebounding from -1.3% in December. Overall, manufacturing and construction showed a more positive performance. Which is a good sign for a healthier growth of the whole economy. On the construction side there is arguably more dynamism as the steel and iron industries were more dynamic, coupled with pending post-pandemic housing sales, but this may be temporary given recent data that home sales have been less dynamic. While on the manufacturing side there has been a mixed performance, but with stronger declines especially in the automotive industry, due to still high costs causing a lower demand that has reflected in a drop in housing sales in the first two months of the year of around -19%, while the housing industry has been more dynamic, with a lower demand in the second half of the year, which has been reflected in a drop in housing sales of around -19%.

- Services activities (70% of the economy) increased by 7.4% year-on-year with a monthly expansion of 1.3%. When reviewing in detail the monthly contribution, the set of activities that brings together trade, accommodation, food services and transportation presented a more positive performance increasing +3.7% breaking with the contraction trend of the last quarter of 2022, which may be explained by the recent retail sales data that expanded 2.8%, which still shows a solid household consumption that may be explained by remittances and the underground economy. Similarly, entertainment, arts, public administration, health and education continued to add to the overall performance of the sector as a whole.

The January ISE reading suggests that economic growth remains positive but at a more moderate pace. It is clear that services will continue to contribute positively to growth as households continue to moderate their consumption as a result of inflationary pressures, which is healthy for overall economic growth, coupled with a surprisingly buoyant secondary sector that may be explained to a greater extent by construction which is also healthy for growth this year, so it will be relevant to remain vigilant to metrics associated with the sector. That said, we expect 1.5% growth by 2023. In terms of interest rates, we expect a 25bps hike to 13% at the March 30 meeting, and for the bank to keep the rate at this level for a prolonged period of time due to inflation and an economy that still looks solid.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.