- Colombia: Retail sales and manufacturing showed a better-than-expected performance at the beginning of 2023

Markets are trading in a more upbeat mood as Credit Suisse comes back from the brink after it announced it’s borrowing as much as CHF50bn from the SNB via a liquidity facility as well as planning to buy back up to CHF3bn of CHF and EUR-denominated debt. This came on the heels of a joint statement by the SNB and FINMA last night stating that “the SNB will provide liquidity to the globally active bank if necessary.”

The USD is mixed against the major currencies though softer on a DXY basis as the EUR, CHF, JPY, and CAD all gain ground. Again the MXN is starting the day on the backfoot, lagging its peers with a 0.5% loss, and is trading around its weakest levels on Tuesday and Wednesday’s in the low-19s.

US S&P500 futures are flat to slightly weaker, erasing some optimism that followed CS’s announcement, and as markets head with some uncertainty into the ECB’s difficult to call decision at 9.15ET (rates markets are slightly biased towards a 50bps increase). Crude oil and copper are up about 1% as they pare some of the large losses of the past few days, while iron ore in Singapore falls 2% (in a somewhat lagged reaction).

Events in Latam may pose little challenge to headlines surrounding the global banking system and the ECB’s decision as the main driver of market sentiment in the region.

Colombia’s Petro is expected to present today his labour reform bill to Congress at 15.30ET. If past submissions in other reform areas are any indication, the president will likely come down from ‘extreme’ proposals as a first point of negotiation from where his position will likely weaken to something more amenable to lawmakers.

In Mexico, the country’s 2023 banking convention kicks off this afternoon with speeches from Banxico Gov Rodriguez Ceja and Fin Min Ramirez de la O, amidst a highly uncertain global environment for the financial industry. It’s tough to call at the moment what Banxico may do next, but the Fed’s decision next week as well as H1-Mar inflation data and (the somewhat stale) January IGAE release will likely help us refine our expectations—currently seeing a 25bps hike in late-month.

—Juan Manuel Herrera

COLOMBIA: RETAIL SALES AND MANUFACTURING SHOWED A BETTER-THAN-EXPECTED PERFORMANCE AT THE BEGINNING OF 2023

On Wednesday, March 15, the National Statistics Institute (DANE) published its monthly surveys of economic activity for January. Manufacturing production and sales showed a positive performance versus expectations. Meanwhile, service-related sectors continued to perform positively, but lost some momentum.

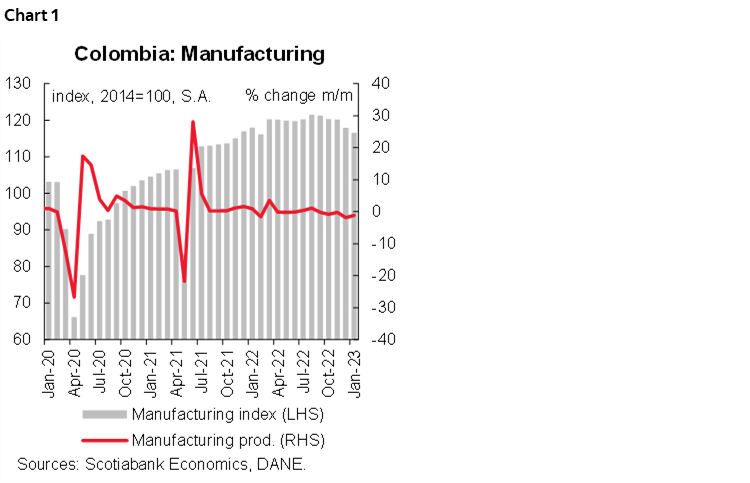

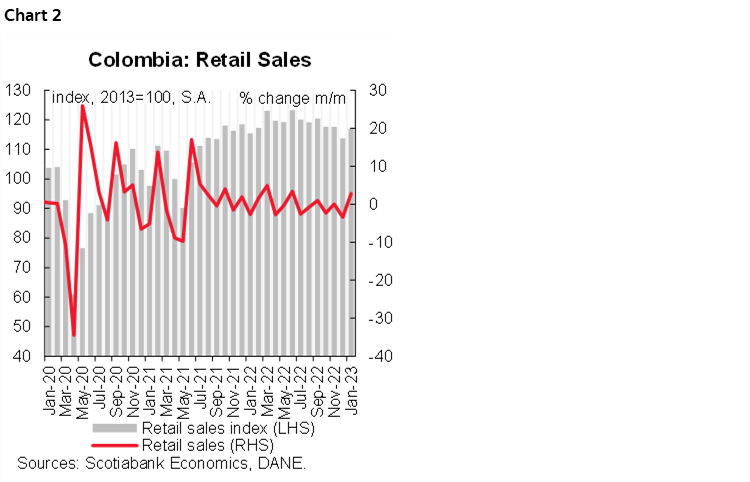

Economic activity indicators for January came in better than expected. Retail sales expanded by 1.2% y/y (vs. -1.5% expected), while retail sales excluding vehicles and gasoline grew by 4.2% m/m, interrupting three months in a row of contractions. In the case of manufacturing, the expansion was 0.2% y/y (vs expected 0%), showing a contraction of 1.12% in monthly terms.

Retail sales are demonstrating some resilience in domestic demand, probably reflecting still the strong positive shock of households’ income due to historically high remittances and the underground economy. In the case of the industrial sector, the data reflects the impact of higher costs, FX depreciation, high interest rates, and bottlenecks in some industries.

These indicators don’t change our expectation for BanRep; we expect a 25 bps hike in the March 30 meeting to take the rate to 13%. In our opinion, despite today’s data looking more robust than expected, some coincident data is showing that the formal part of the economy is slowing down rapidly, especially credit. On the other side, inflation is transitioning through a ceiling. Both fundamentals will probably keep BanRep’s board in a data dependent mode, but we continue favouring rate stability after the March move.

Manufacturing production

Manufacturing production increased by 0.2% y/y (above the market consensus of 0.0% y/y), showing a monthly contraction of -1.12% m/m (chart 1), less sharp than the contraction recorded in December 2022. January's results continue to confirm the slowdown trend that began at the close of last year amid effects that have been persistent such as input costs, lower demand and business confidence, and uncertainty about the performance of the global economy.

On a y/y basis, the best-performing sectors were petroleum refining, oil, and fuels (+16.9% y/y), soap and perfume manufacturing (+16.5% y/y), and beverages (+5.6% y/y). On the negative side, sectors that reduced activity were chemical products (-24.9% y/y), sugar and sugar cane processing (-27% y/y), and pharma products (-13.9% y/y). In general, we observe other relevant industries showing y/y contractions, which signals the effect of weaker demand, which is the case of the vehicles sector. On the positive side, evidence of an improved performance in manufacturing for some construction-related activities may be a positive sign for the economy's growth.

Employment growth came in at 1.4% y/y. On a m/m basis, employment slowed and registered a contraction of 0.30%. Which may be a sign of deterioration in the formal sector.

Retail

Retail sales showed a positive balance gaining 1.2% y/y in January, above the Bloomberg survey (-1.5% y/y) (chart 2), while employment presented a better performance at 4.7% y/y vs. 4.2% in the previous month. On a seasonally adjusted basis, retail sales (excluding other vehicles) showed an expansion of 2.8% m/m evidence that households maintain a decent level of consumption.

On an annual basis, the retail sales performance is explained by a better performance in books and stationery (+15.5% y/y) footwear (+14%y/y) alcoholic beverages (+12.8% y/y), audio and video equipment (+10.1% y/y), clothes (+10.1% y/y), spare parts for vehicles (+8.4%y/y). While the items that presented negative variations were pharmaceutical products (-17.1% y/y), household cleaning products (-10.3% y/y), household appliances and furniture (-3.4% y/y), vehicles and motorcycles (-7.3% y/y). Either way, households are starting to show a change in the consumption dynamics, reducing the consumption of leisure-related items for consumer staple goods.

Services & Hotels

In January 2023, most service-related activities showed a still positive but moderate expansion, with the most robust growth in film and television program activities (+40.5 y/y) while telecommunications activities had the weakest growth (+1.9 y/y). In terms of employment, the activities with the largest variations were advertising (+7.4% y/y) and computer systems (+6.9% y/y).

In the hotel sector, revenues showed an expansion of 9.5% y/y, higher than that observed in the previous month (8.6% y/y). Employment growth stood at 14.9% from 18.9% in the previous month. Hotel occupancy was lower at 53.7% vs 56.4% compared to the previous month. Business travel continued to show a lower trajectory than the previous month, accounting for 15.7% of total occupancy. Business travel accounted for 34.5%, down slightly from the previous month.

January activity data showed a better performance than expected, but still with moderations in annual growth. In the case of retail sales, informal sources of income maintain a decent consumption. While in manufacturing, there was a more significant deterioration in some industries, such as automotive. We expect the moderation trend to continue thanks to a less dynamic private consumption, as we expect to see inflation still high for most of the year and amid the effect of the hiking cycle. Under this scenario, we affirm our expectation that at its March 30 meeting, BanRep will raise the rate by 25 bps to 13%.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.