- Colombia: Confidence improved a bit in February

- Peru: Rain, rain, go away!

Financial sector risks continue to generate volatility in broad markets, with large moves higher in US rates markets helping the USD to gains versus most major currencies. Crude oil and copper, down about 2.5% and 1% respectively, are being weighed by the higher yields backdrop while iron ore trades unchanged to slightly higher. Meanwhile, US equity futures are better bid (+0.5%) while European bourses trade mixed.

Global markets will continue to monitor more bank failure risks today, but the relative quietude after the weekend’s developments has increased the focus on this morning’s US CPI print, where a miss or a beat could tilt the needle in favour of a Fed pause or hike at next Wednesday’s decision. The Latam day ahead is very quiet with no notable data or events on the calendar.

The MXN is correcting a fraction of yesterday’s slide to outperform its major peers thanks to a 0.7% gain, coming on the heels of its first close above its 50-day MA since late-2022. A continued repricing of Fed hike expectations (with implied rate bets at 18bps showing a preference for a 25bps hike rather than a hold) and a relaxation of market angst could pull the USDMXN back towards the 18.50 support zone—but markets are unlikely to fully unwind the peso’s losses from the high 17s just last Thursday. The Cetes rally yesterday (6m down ~15bps) is likely to be trimmed today in line with the moves in the US.

—Juan Manuel Herrera

COLOMBIA: CONFIDENCE IMPROVED A BIT IN FEBRUARY

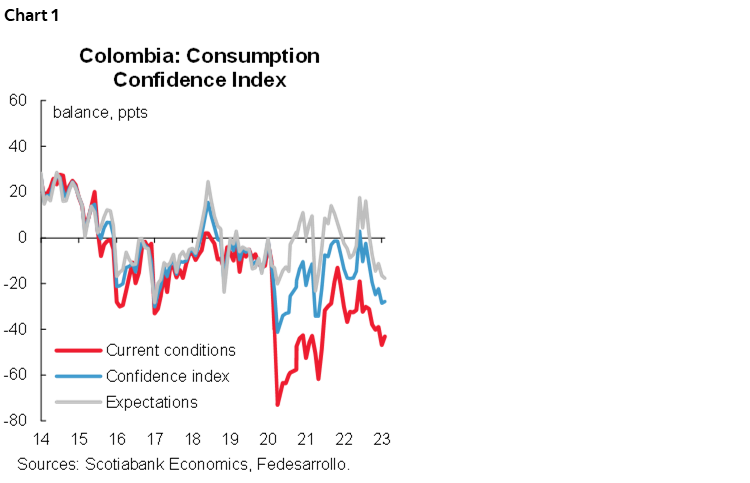

Colombia's Consumer Confidence Index (CCI) for February came in at -27.8 ppts, showing an improvement of 0.8ppts. This slightly better dynamic is mainly due to an improvement in current conditions, which increased by 3.7ppts to -43.1ppts, which was partially offset by the future expectations component that declined by 1.2ppts from -16.5 to -17.7ppts (chart 1).

The expectations index worsened and continued to weigh on a more negative perception of the country's economic and household conditions during the year. However, the willingness to buy homes increased 2.7ppts from the previous month (-51% to -48.3%), and the willingness to buy vehicles showed a slight improvement from the previous month, increasing 0.2 ppts ( -66.5 to -66.3ppts), maybe due to a slightly lower exchange rate seen during the year.

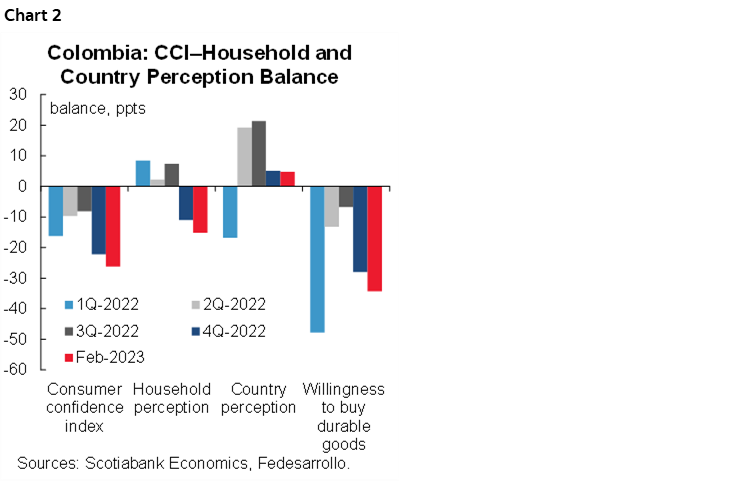

Likewise, the willingness to buy durable goods increased by 5.4 ppts versus the previous month, from -59.3 to -53.9 ppts, while the slightly less negative balance is probably still explained by persistent price pressures, as inflation continues its upward trend but at more moderate rates (chart 2).

Looking at the details for the month of February:

- The current conditions index came in at -43.1 from January's figure of -46.8 ppts. Households remain vigilant as inflation continues to surprise to the upside and shows no signs of stabilizing, maintaining negative sentiment on the willingness to purchase goods.

- The expectations index decreased to -17.7 ppts in February from -16.5 ppts in February (chart 1, again). Household expectations about the economic future were the only positive component of the CCI. In fact, the index remained in positive territory but weakened (5.9 to 2.9 ppts). In contrast, the evolution of expectations for the country's economy showed a further deterioration that contributed to the negative ICC balance, at -20.4ppt from -16.5ppt.

- Signs of moderating activity, with private consumption continuing to moderate, increasing expectations of much lower growth in 2023, may affect perceptions in the coming months. Therefore, consumer credit is likely to continue to decelerate, despite rate moderations by the country's banks, as it is necessary for the economy to return to healthier growth.

- Consumer confidence by cities increased in two out of five cities in the sample. Bogota and Barranquilla had increases. In Cali, confidence worsened from -19.4 to -28.8 ppts. In Medellin it decreased from -30 to -41.6 ppts 18.5 ppts and in Bucaramanga it decreased from -16.2 to -24.5 ppts.

- Confidence improved at the middle income level. At the high income level, confidence worsened from -40.3 to -51.9 ppts. The perception of low-income families fell and worsened from -27.8 to -28.9 ppts. This behavior can be explained by the intense pressures on prices, given the continuity of the effects of indexation and food prices, which remain under upward pressure, added to a greater financial burden on households due to the levels at which the cost of consumer credit was, and by the moderation in growth which causes uncertainty in the future of the economy.

In February, consumer confidence showed still depressed sentiment among households, although the deterioration stopped. Having said that, it remains on the negative side of the balance as consumers' expectations about the economic future remain negative; households continue to be affected by the effects of rising inflation and the perception of a slowdown in economic activity. This is a relevant sign that private consumption is moderating, however, we will have to evaluate how the moderation in the cost of credit consumption announced by several banks influences and how it affects the scenario of the monetary policy tightening cycle. For now, we maintain our expectation that at the March 30 meeting, the Bank will increase its policy rate by 25bps to 13.00% and hold there for a long time.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

PERU: RAIN, RAIN, GO AWAY!

It’s raining, it’s pouring in northern and central Peru. Just as we were hoping that after three months of on-again-off-again protests, March would finally be a more normal month, a highly unusual “cyclone-type phenomenon” has appeared off the coast of norther Peru to dampen our spirits. The cyclone has been named Yaku, which is quite symbolic, being that Yaku is the Quechua word for water, tonnes of which are being dropped, generating floods and malaise. Local weather authorities have stated that rainfall in some parts of the north surpassed historic records for a 24-hour period.

Peru is accustomed to huge summer rains linked to El Niño. But the current cyclone assailing the coast is, according to local weather authorities, something that has not occurred in forty years. One has to wonder what’s in store next for the country, a snowstorm in the Amazon, maybe?

The government has responded to Yaku by imposing a State of Emergency in 13 of the country’s 24 regions. The start of the public school year in Lima, scheduled for March 13, has been officially postponed for a week, until March 20, in what we hope is more the result of an overabundance of caution, than of the real degree of threat that the rains represent. Private schools should mostly remain open.

The government has also announced that it would increase the 2023 budget by PEN4bn (0.4% of GDP), which would be nearly half of a PEN8.2bn budget expansion program that is already in the works and should be submitted to Congress for approval soon.

Our understanding is that, although the cyclone is independent from El Niño, they have in common that they are linked to warm ocean temperatures. The cyclone itself is likely to wane relatively soon (it is reportedly slowly moving southwest, pulling away from the coast, but affecting new regions along its way), but the warm ocean water that contributed to generating the cyclone is likely to continue prompting rains. These, according to weather authorities, could last until May, although not at the same intensity as now.

It is too early to gauge the impact that the flooding is having on the economy. In the past, only very strong El Niño episodes have had a significant impact on the economy, mostly in terms of growth, but also impacting inflation at times. There are reports of some crops in the north being under threat to some extent, but in general it is not yet evident that the current weather situation will have a magnitude of impact similar to a strong Niño. The BCRP, has voiced its concern that the rains could impact inflation to some degree. We do not expect this impact to be significant enough to reverse the decline in yearly inflation that we expect to occur in March, and we have not changed our view that the BCRP will maintain the reference rate at its current level of 7.75% at their April meeting. Even so, there is one thing that is sure, and that is that we can no longer view March as a month in which the economy has returned to normality.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.