- Peru: BCRP keeps policy rate unchanged for second consecutive month

Equity markets traded on the back foot following yesterday’s rout in US stocks amid cracks appearing on the ‘fringes’ of the country’s banking sector (crypto and start-ups-related), with major spillovers seeming unlikely. SPX futures are tracking a 0.2% decline after the 1.9% selloff on Thursday. Crude oil is down about 0.8%, while iron ore and copper again move in opposite directions (up and down ~1% respectively).

Despite the clear risk-off mood in equities, currencies are in relatively decent shape against the USD, which is trading mixed—generally losing ground against ‘safer’ European FX while high-beta currencies somewhat underperform. The MXN depreciated to its weakest point since mid-Feb overnight, just past the mid-18s zone, but is now among the best majors, higher 0.5%—though still ~2% off yesterday’s intraday high. The MXN’s relationship with US yields (reflecting the perception of linked Fed-Banxico monetary policy) yesterday acted as a negative driver for the currency while the COP, CLP, and PEN simultaneously strengthened. Note also that Mexican inflation missed forecasts yesterday (see Latam Daily), troubling calls for a repeat 50bps hike from Banxico at month-end.

Global markets are laser-focused on the 8.30ET release of US employment data, where economists are calling a sizable decline in the number of jobs created after a blockbuster increase in January. A lot hinges on today’s data as recent strength in US economic figures prompted Fed officials, notably Chmn Powell earlier this week, to talk up the possibility of moving back to a 50bps hike later this month. As alluded to above, a strong jobs print is liable to support the MXN while weighing on the country’s debt markets on higher odds of a Banxico half-point hike.

In the Latam region, we await the BCRP’s presser at 12ET on yesterday’s rate hold (see below), while we keep an eye out on political developments in Colombia with Congress President Barreras saying yesterday that there are “more agreements than disagreements” on Petro’s health reform proposal.

Brazilian CPI published this morning slightly beat economists’ expectations, with a decline to 5.60% from 5.77% (vs the consensus median at 5.53%); prices rose by 0.84% m/m from 0.53% in January and above an estimated 0.78% pace. The BCB looks still in hold mode, but calls are rising for the start of the cutting cycle, seen at roughly toss-up odds in May but a 25bps cut is fully priced in for June amid economic weakness—and real rates are becoming more and more restrictive. Today’s minor beat is unlikely to alter this view significantly.

—Juan Manuel Herrera

PERU: BCRP KEEPS POLICY RATE UNCHANGED FOR SECOND CONSECUTIVE MONTH

The board of Peru’s central bank (BCRP) kept its key interest rate at 7.75% on Thursday, in line with the market consensus and with our forecast, confirming the pause stance for the second consecutive month after 18 months of increases. Although in its statement the BCRP kept its options open to changes in any direction in the future—specifying that this decision does not necessarily imply the end of the interest rate hike cycle—we believe that 7.75% is likely the terminal rate. Recently, the BCRP’s head of the Board, Julio Velarde, pointed out that the level of 7.75% or very close to it is enough to control inflation without causing a recession.

The statement kept its concerns about the macroeconomic effects of social unrest. This had its highest impact in January, so the BCRP estimated that GDP fell -1.4% that month. The intensity of the protests moderated in February and continued to reduce in March, which was reflected in an improvement in indicators and expectations about the economy in February—though these remain in pessimistic territory. The impact of social unrest on the economy has been material. Velarde recently indicated that they would probably revise their GDP growth forecast for this year (after it was lowered from 3.1% to 2.9% in December) in their Inflation Report this month.

In February, year-on-year inflation accumulated 21 months outside the target range, matching the previous record. Inflation stabilized in February and marked a second consecutive month of coming in below what the market expected. The BCRP, like us, expects a visible drop in inflation starting in March. Although the statement maintains the expectation of a return to the target range in Q4-2023, Velarde suggested that inflation could be slightly above 3%, and forecasted inflation of 2.4% for 2024. Our inflation forecast remains at 5.00% by end-2023.

In the scenario that the terminal rate has already been reached, our focus is on how long it can stay at this level. Twelve-month inflation expectations are key. In February, these returned to the previous level, going from 4.6% to 4.3%, still well above the target range (between 1% and 3%). March inflation is expected to be seasonally high (due to short-term and seasonal factors, such as education), but well below March 2022 inflation (1.48% m/m), so we see the possibility that year-on-year inflation will fall from 8.6% to below 8%.

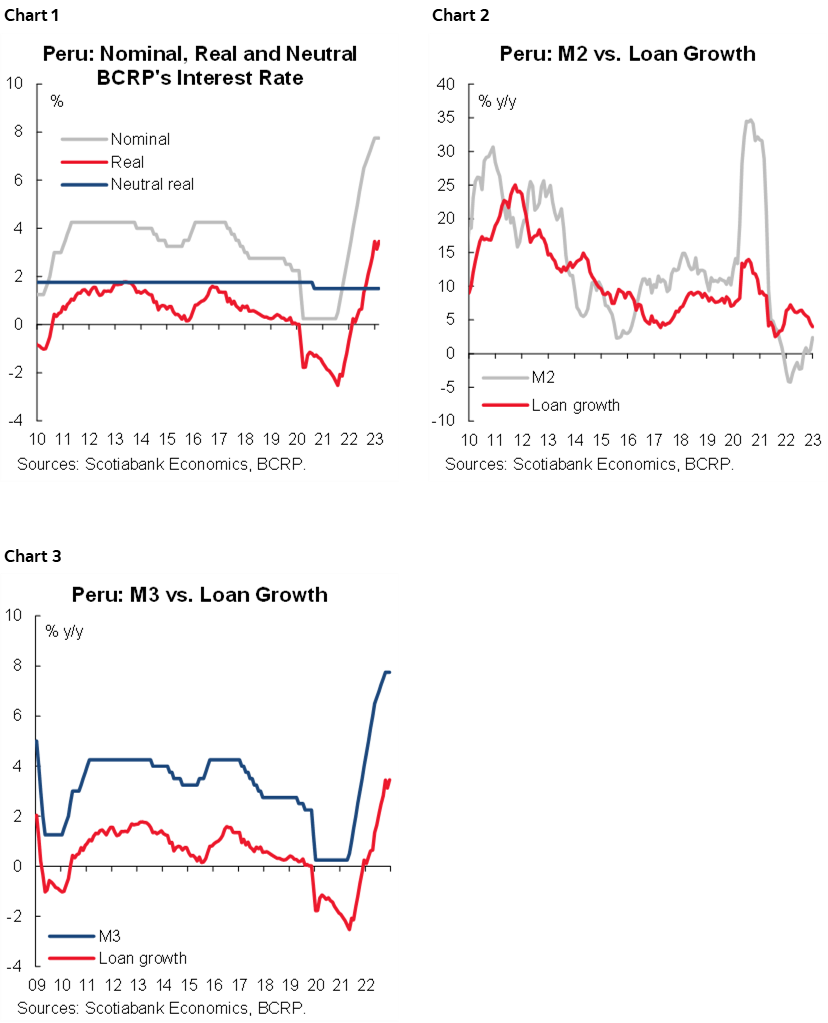

The decision to hold the policy rate could also have considered that the monetary policy stance is already tight enough to deepen economic weakness. The real interest rate rose from 3.13% to 3.46% (chart 1), above its neutral level (1.50%) for the seventh consecutive month. Liquidity growth in soles (M2, chart 2) accelerated from 0.5% to 2.4% in January, remaining in positive territory for the fifth consecutive month, while, on the contrary, credit expansion slowed down for fifth consecutive month, going from 4.5% in December to 4.0% in January (chart 3). The BCRP statement indicated that prospects for global economic activity have shown a slight improvement, although global risk remains due to restrictive monetary policy in advanced economies, the impact of inflation on consumption (purchasing power), and ongoing global conflicts.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.