- Mexico: Headline inflation sub 6%, cuts must wait a while amid high core

- Peru: BCRP holds key rate for 5th consecutive time and changes view regarding inflation returning to target range by year-end

We’re heading into the weekend with only some second-tier Mexican data left for release, a BCRP presser, and global markets having little in the calendar to trade on aside from Canadian employment data at 8.30ET. It was a quiet Asia session, handing over generally narrow ranges in currency, rates, commodity, and equity futures markets to European traders that just couldn’t let the trading calm continue. Still, even the moves in Europe dealing are modest.

The USD is caught in 0.1/2% gains and losses against all major FX, with the clear exception of two: the top performing NOK on stronger than expected inflation, and the worst performing JPY that extended overnight weakness on dovish BoJ leaks. The MXN is flat but on track for another weekly gain (15 out of 23 weeks so far in 2023). US yields are about 3/4bps higher across the curve, SPX futures are showing a 0.2% drop, WTI is about 0.4% firmer (recovering a decent chunk of yesterday’s losses on Iran-US nuclear deal rumours), iron ore is 2% higher, and copper is little changed.

Mexico releases April industrial production data at 8ET, with the median economist expecting a 1.3% y/y increase after a 1.6% gain in March, but the data will be of no consequence for Mexican rates markets that are likely content with where they sit after yesterday’s inflation data (see below). For those following ‘nearshoring’ developments, or merely the encouraging outlook for Mexico’s manufacturing sector, a key Japanese automaker announced yesterday that it will invest an extra USD330mn in its plant in the state of Guanajuato.

It will be headlines and flows that drive markets today. At 13ET, the BCRP has its post-decision press conference where we’ll be looking for colour on why they’ve changed the language around expectations for where inflation will sit at year-end (see below). Colombia’s Pres Petro is in Cuba today for peace talks with the ELN, but this is unlikely to influence local rates and currency markets that have benefitted from weakening social reform prospects and the recent lower than forecast inflation print. On a related note, we point you to our Santiago team’s Chile inflation flash here.

—Juan Manuel Herrera

MEXICO: HEADLINE INFLATION SUB 6%, CUTS MUST WAIT A WHILE AMID HIGH CORE

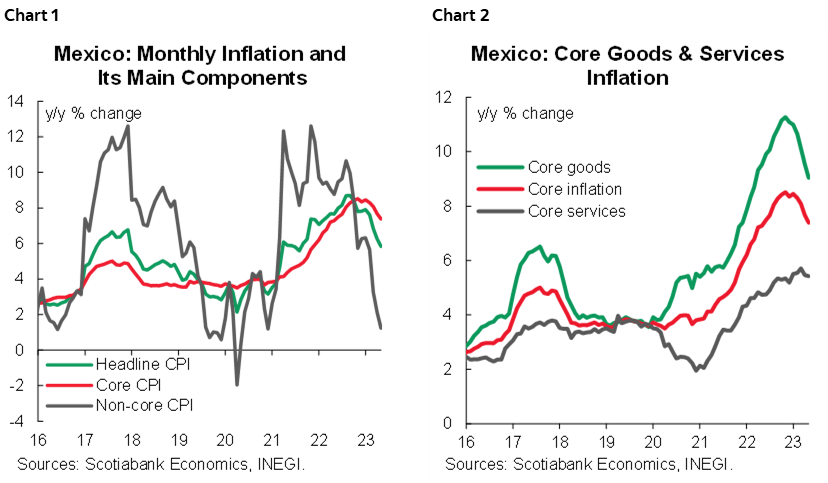

In March, inflation eased slightly more than expected to 5.84% y/y from 6.25% previously (vs 5.90% consensus), reaching its lowest point since August 2022. Core inflation also slowed to 7.37% from 7.67%, practically in line with the median seeing 7.38%.

Services inflation slightly moderated to 5.43% (5.46% prior), owing to a slowing in non-housing/education services prices (7.01% vs 7.10%). Core goods inflation also slowed, to 9.04% (9.54% prior). Non-core maintains a downtrend going from 2.12% to 1.24% y/y, with agriculture moderating to 4.95% (6.13% prior) and energy dropping to -1.83% (-1.08% prior).

In its monthly comparison, headline inflation fell to -0.22% m/m from -0.02% previously (-0.16% consensus), and core inflation went to 0.32% m/m from 0.39% previously (0.33% consensus). Lastly, non-core inflation fell to -1.88% m/m from -1.25% (charts 1 and 2).

After this print, we expect inflation to continue its downtrend, although will remain elevated by the end of the year (exceeding Banxico's target by 3ppts), with core inflation also remaining above the headline trend. On monetary policy implications, analysts expect the first rate cut to be in December of this year according to the latest Citibanamex Survey. Also, analysts project inflation at 5.01% y/y at the end of 2023, and 4.02% at the end of 2024, in contrast to Banxico's forecasts, that see inflation converging to the 3.0% target by Q4-24.

—Miguel Saldaña & Brian Pérez

PERU: BCRP HOLDS KEY RATE FOR 5TH CONSECUTIVE TIME AND CHANGES VIEW REGARDING INFLATION RETURN TO TARGET RANGE BY YEAR END

The board of Peru’s Central Bank (BCRP) kept its key interest rate unchanged at 7.75% this Thursday, in a decision widely expected by the market consensus and by us, for the fifth consecutive month. In its statement, it reiterated that it keeps its options open to changes in any direction in the future, specifying that this decision does not necessarily imply the end of the interest rate hiking cycle.

Year-on-year inflation fell slightly in May, in line with what was expected by the market, although it remains outside the target range for 24 months, a record sequence. Monthly inflation reached 0.32% m/m, more than double the May month average of the last 20 years (0.14%). So far, no visible drop in inflation has materialized, as we and the authorities expected. In May, more than 65% of the prices of the consumer basket posted increases, a proportion that has been maintained so far this year.

However, for June we expect a more visible decrease in inflation, with the possibility that the monthly data may even be below the June month average of the last 20 years (0.17%), since we see a significant correction in poultry prices, which would reflect the fading effects of the bird flu, to which would be added lower prices of local fuels. In its statement, the BCRP no longer mentioned the effects of the rains caused by Cyclone Yaku. With this, we believe that year-on-year inflation in June is likely to be below 7%. The BCRP expects food prices to drop for the remainder of the year, which would help lower inflation.

Although the advance guidance in the statement does not yet give clear signs of how long the policy rate will remain at its current level, the BCRP would be cautious in rushing to start easing policy after the government declared an emergency due to the imminent risk of the El Niño global phenomenon, which would bring uncertainty about prices, as has happened in the past. Twelve-month inflation expectations have fallen from 4.25% to 4.21%, a decrease still without conviction, remaining well above the target range (between 1% and 3%). 24-month inflation expectations were raised from 2.89% to 3.13%, reflecting that the consensus still sees that the return of inflation to the target range could take longer.

Recently, the BCRP governor pointed out that inflation will reach the target later than expected because inflation has been slowly declining. This view was reflected in a new wording in the BCRP’s statement, noting that it now expects inflation to be close to the target range at the year-end, so the return to the target range in Q4-23 is no longer as explicit. This could lead one to think that the BCRP would keep its interest rate at the terminal level for longer.

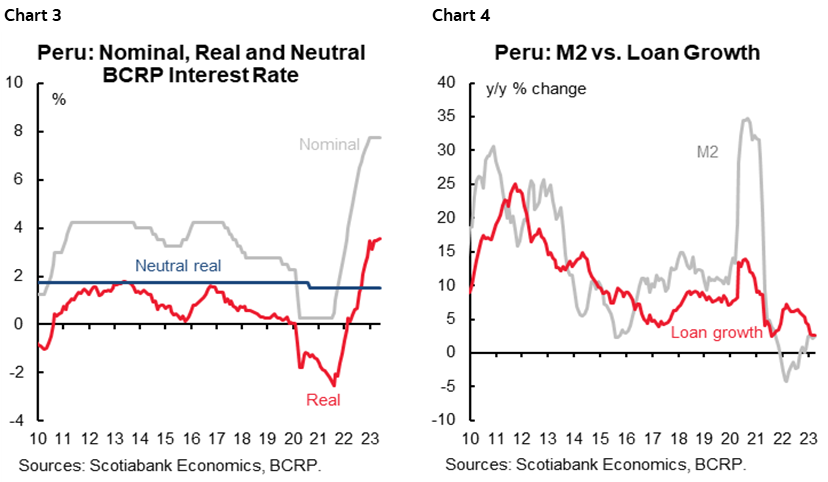

Other important inflation indicators show a clear downward trend. Wholesale inflation continues to fall and is now at 1.6%, the level it was at the 2020-end when the producer prices index began to alert us that inflation would increase. It now tells us that headline inflation should start to come down. The PEN appreciation (close to 2% y/y) would also help curb inflation in the future. Our inflation forecast remains at 5.00% by end-2023. We also maintain our expectation that the BCRP will keep the reference rate at 7.75% through Q3-23, lower it to 7.25% in Q4, and continue easing until a level near 5.25% by end-2024. The real interest rate held steady at 3.5% (chart 3), staying above its neutral level (1.50%) for the tenth consecutive month. Liquidity growth in soles (M2, chart 4) recovered and went from 2.1% to 2.4% in April, remaining in positive territory for the eighth consecutive month, while credit expansion stabilized around 2.7% in April. Business expectations improved in May in relation to April but remain in a pessimistic zone. The economic indicators have not been recovering as expected. The BCRP statement also confirmed that the outlook for global economic activity points to moderation, although global risks remain due to restrictive monetary policy in advanced economies and ongoing global conflicts.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.