- Colombia: April exports fell 31.5% y/y mainly due to lower commodity prices

Overnight markets traded on limited information, with a USD-positive, risk-offish bias in early European trading interrupting the Asian markets lull, to then be unwound sharply over the past three hours or so to turn the USD on its head, weaker against all major currencies. We’re keeping a close eye on moves in the Chinese yuan, as broad moves in the USD in recent days have coincided with pivotal levels in the USDCNH cross. Overnight the yuan rallied after weakening past 7.14, slowly losing to that level after weak exports data.

To be fair, crude oil prices are also on a tear since around the U-turn in the USD started and are now about $2.50 above yesterday’s lows and up ~1% on the day. Other commodities also look well supported, iron ore is up 1.5% and copper has gained 0.8% (the weaker USD may be helping). Rates markets are chopping around, but bear flattening on net through overnight trading, while US equity futures follow moves in other markets, but in somewhat contained ranges, to sit roughly unchanged on the day.

We have Latam inflation data today. Finally, after two somewhat uneventful days in the region, but also from a global standpoint. This ignores the political intrigue in Colombia, of course, where leaked audios of discussions between (now former) government officials have left President Petro’s reforms effort on tenterhooks. Protests around the country are expected today in support of the government’s reforms and the president, but broader public backing of the administration continues to weaken and ‘market-unfriendly’ legislative pushes now look more unlikely. The Partido de la U (which recently left Petro’s legislative alliance) has called for the government to delay its social reforms past the current session which ends on June 20.

Turning back to today’s data, Brazil’s inflation rate for May is seen marginally above 4% by the median economist in data released at 8ET, falling from 4.18% in April. The slowing will partly come on the back of a (roughly) halving in m/m price gains from 0.61% to 0.33% expected. Yesterday’s IGP-DI data (which combines producer, consumer, and construction prices) showed a steep decline in inflation in May, to –5.4% from –2.6% y/y in April, and added to expectations that the BCB will cut rates very soon—though not yet in June, with the first full cut of 25bps almost priced in for the August decision. In related news, Brazil’s senate economic affairs committee is set to vote on June 20 on two nominees to the BCB, namely Galipolo as monetary policy director (who sounds supportive of starting rate cuts soon).

Much later in the day, at 19ET, Colombia’s DANE will release its own prices data. Our Bogota economists are eyeing a 12.6% y/y pace of headline prices growth (in line with the Bloomberg median), down from 12.82% in April, with some downside risks owing to food prices; core inflation is forecast little changed in the mid-11s (very high). Inflation has peaked, so BanRep will be happy that readings come in lower each time and will thus hold its policy rate unchanged this month, but they’re certainly not ready to clearly tee up lower rates later in the year given double-digit prints—though FinMin and BanRep board member Bonilla has shown his preference for this.

Global markets don’t have any major US data to look ahead to, but we have an important event at 10ET with the Bank of Canada’s policy decision that looks too close to call between another rate hold or the first 25bps increase since January; our official forecast is for a 25bps hike. Chile’s president Boric is attending the first session of the constitutional council today as work kicks off towards a new text.

—Juan Manuel Herrera

COLOMBIA: APRIL EXPORTS FELL 31.5% Y/Y MAINLY DUE TO LOWER COMMODITY PRICES

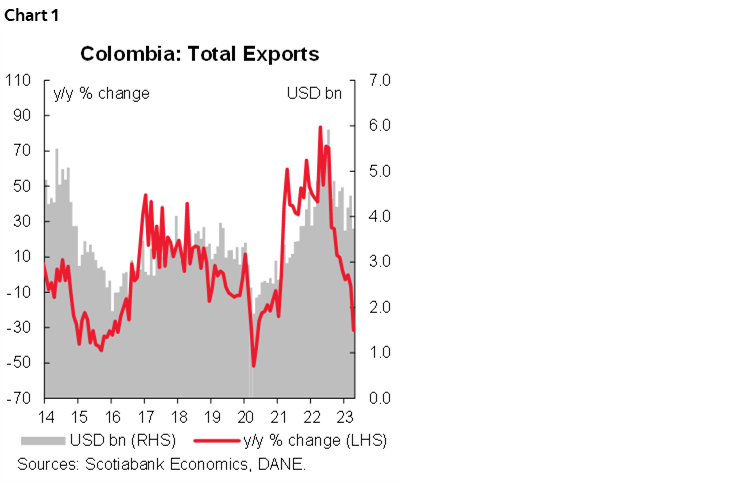

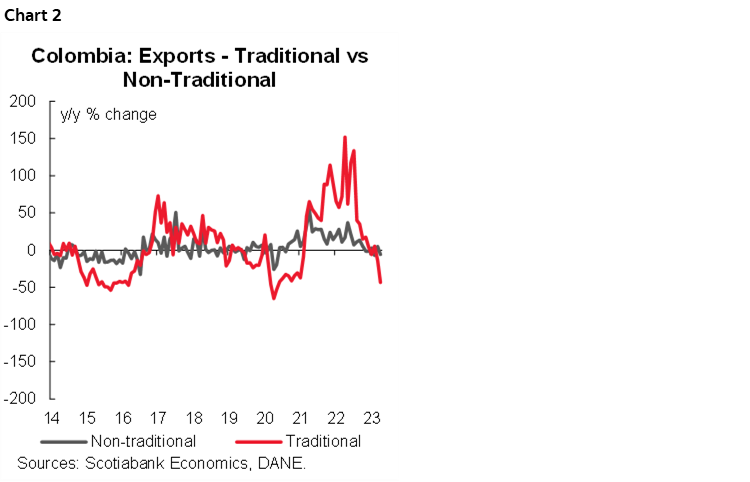

DANE released the export data on Tuesday, June 6. Monthly exports for April stood at USD 3.74 bn, a contraction of 31.5 % y/y (chart 1), the lowest level since September 2021 and posting the fourth annual contraction in a row. Traditional exports (related to mining and coffee) drag the global export figure (-43.66% y/y), standing at USD 2.08 bn, which is USD 0.5 bn lower than the average observed in the previous six months. Meanwhile, non-traditional exports stood at USD 1.65 bn (-6,1% y/y), closer to the six-month average of USD 1.70 bn.

The weak result on exports reflected the context of lower commodity prices compared with one year ago, especially for mining-related exports such as oil and coal. Previous data is showing that trade deficit correction could lose steam in the forthcoming month. The high statistical base of commodity prices is a headwind for exports in dollar terms, that now could partially offset the effect of lower imports in the reduction of the external deficit.

- Traditional exports contracted by 43.66 % y/y in April (chart 2). In April the weak performance was a combination of lower exported volume and lower prices, however, the former was the main effect. By components, coffee exports contracted 35.44%, explained by a more moderate volume (-20% y/y) but also by weaker international prices. Oil exports fell 34% y/y, mainly due to a ~20% contraction in oil prices, since volume contraction was only 4.03%. In the case of coal, the 59.1 % y/y contraction was mainly due to volume contraction. On the other hand, ferronickel sales showed a contraction of 57.3 % y/y, which is also a result of lower volumes.

- Non-traditional exports contracted by 6.1% y/y. Manufacturing exports contracted by 1.5% y/y. Sales of other manufacturing products (-18.2% y/y) and chemical-related products (-1.4%) contributed the most to the contraction. On the other side, agricultural products such as palm oil (-35% y/y), flowers (-22.3% y/y), and bananas (-34.5% y/y), moderated the performance of all the groups. However, non-traditional exports remain close to historical highs.

All in all, exports reflect the headwind from lower commodity prices, especially on oil exports, which could prevent the trade deficit from further strong corrections. Either way, the current account deficit in 2023 is expected to be significantly lower versus 2022, which is a positive fundamental for the COP. The central bank estimates a current account deficit of USD 14.69 bn (4.1% of GDP), and a USD 12.65 bn deficit only on the trade balance of goods and services.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.