- Brazil: BCB leaves Selic rate at 13.75%, as was anticipated

- Colombia: Imports continued easing in April

Overnight hours were quiet in thin volumes in Asia with China/Taiwan/HK out on holidays and no data or headlines of note aside from some dovish comments by a BoJ official. Markets began trading with a more risk-averse feel in the lead-up to the European open and ahead of rate decisions in Switzerland and Norway (25 and 50bps hikes, respectively). SPX futures are down 0.2%, the USD is mixed in 0.1/2% ranges against all majors with NOK up 1.5% a key exception. Oil is down 1.3%, lagging the core commodities as copper and iron ore trade higher by 0.9% and 0.8%, respectively, as the China emotions rollercoaster continues. Rates markets are bear steepening, and mostly continued this trend through the rate decisions this morning.

While global markets focus on the BoE’s decision at 7ET (and its aftermath), US jobless claims data at 8.30ET, and another appearance in Congress by the Fed’s Powell at 15ET, the Latam calendar presents H1-Jun Mexican inflation data at 8ET ahead of Banxico’s policy announcement at 15ET. This follow’s the BCB’s as-expected unchanged rate decision yesterday, which somewhat surprised in that the board led by Campos Neto chose to not give an indication that rate reductions are coming soon as markets expect in August (see more below). On brand, Lula said this morning that the BCB’s head is playing against the country’s economy.

Mexico’s rate hold should be no surprise, nor should it deliver material changes to guidance. Banxico officials just started the pause stage of the cycle when they left the overnight rate steady at 11.25% in May. Since then, hawkish meeting minutes and officials saying that policy will remain the same for at least two meetings, if not three or even four for some within the board, means today's announcement meeting is merely procedural as the bank observes data to pick the best time for the first rate cut (in September, November, or even December). H1-Jun CPI data are seen showing another deceleration in headline and core inflation, but it’s much too early for the central bank to sound optimistic as core prices growth remains above 7% y/y.

Meanwhile, Colombia’s FInMin and BanRep board member Bonilla again showed his support for rate cuts to begin fairly soon, saying yesterday that the bank could “easily” take off 200bps by year-end, and in September “analyse whether interest rates start to come down”.

—Juan Manuel Herrera

BRAZIL: BCB LEAVES SELIC RATE AT 13.75%, AS EXPECTED

The BCB left the Selic rate unchanged, as was expected. It’s worth noting that its base scenario sees IPCA inflation converging to 5.0% by the end of 2023 and to 3.4% by the end of 2024, which is within what the central bank considers its policy horizon. Many market players anticipate this may have been the last COPOM before the board kicks off its easing cycle, which is consistent with the priced in scenario on DI rates which are discounting around 25bps of cuts in August 2023 and almost pricing in 100% probability of a 50bps cut in September 2021. The committee maintained two sided risks to its inflation outlook, highlighting sticky global inflation and uncertainty over the ongoing fiscal discussions in Congress to the upside. We would add that the droughts hitting parts of the Americas add some risks to prices of tradable food related commodities.

However, we think the base case is that the BCB will kick off its easing cycle cautiously (25bps) in its August meeting. We don’t think that a start of the easing is a given, as the BCB’s communique continued to reinforce that patience will be necessary to hit its inflation target, but if the fiscal discussions in Congress yield fruit, we think it will materialize.

—Eduardo Suárez

COLOMBIA: IMPORTS CONTINUED EASING IN APRIL

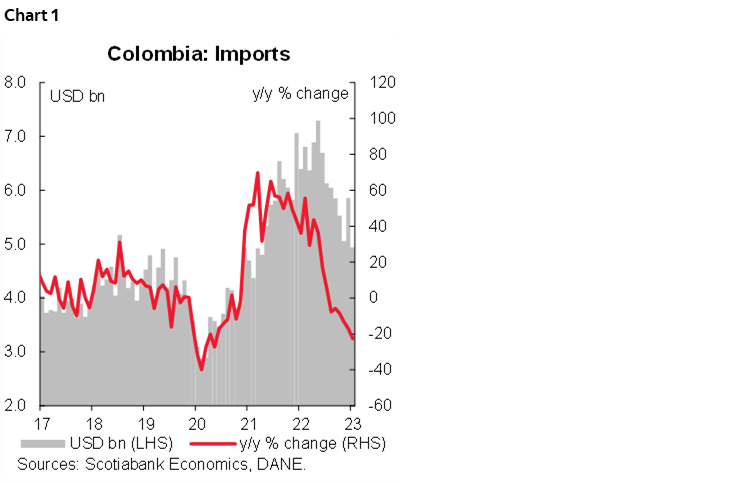

On Wednesday, June 21st, the National Administrative Department of Statistics (DANE) released the import data for April 2023, which amounted to USD 4,942.6 million CIF, a year-on-year decrease of 22.7% and the lowest level since July 2021 (chart 1). This result was driven by a decline in the manufacturing component, which contracted by 22.7% YoY in April 2023, accounting for 72.8% of the total value of imports.

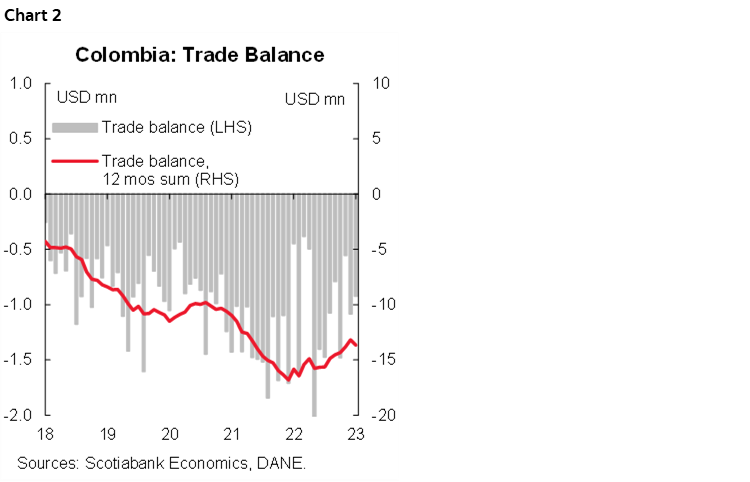

Meanwhile, Colombia’s trade balance recorded a trade deficit of USD 923.3 million FOB in April 2023, compared to a deficit of USD 446.5 million FOB in April 2022 (chart 2). The trade deficit decreased by 14.7% MoM (a deficit of USD 1,082.4 million in March 2023).

Thus, the import results align with the latest economic activity (ISE) and industry data, which reflect the economic slowdown, particularly in the manufacturing component. With these results, coupled with the recent appreciation of the exchange rate, which contributes to reducing the dollar terms deficit, we reaffirm that the Central Bank will consider halting the interest rate hike cycle at this month’s meeting.

Regarding product groups, manufacturing experienced a YoY contraction of 22.7% and accounted for the highest share of total exports at 72.8%. Agricultural, food, and beverage imports contracted by 9.5% annually, representing 17.6% of imports. Imports of fuels and extractive industries declined by -38.8% YoY in April 2023, accounting for 9.5% of the total import value in April 2023.

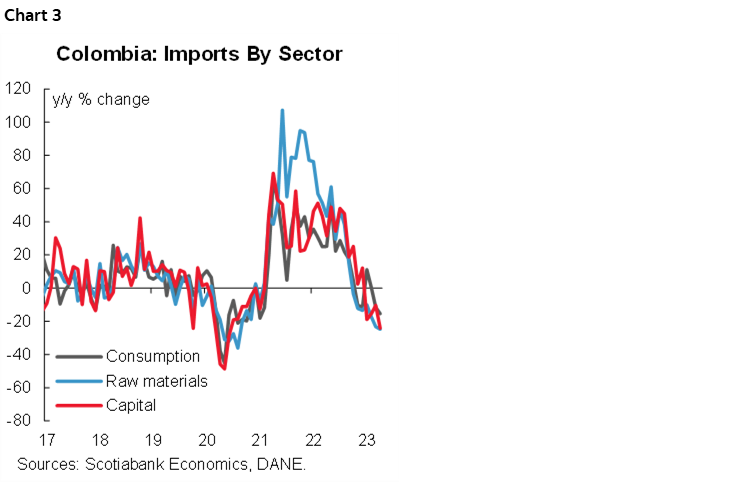

From the perspective of imports by economic use or destination, the three major groups continued to show negative performance (chart 3):

- Imports of consumer goods contracted by 15.4% YoY, amounting to USD 4,942.6 million CIF. Non-durable consumer goods declined by 7.0% YoY, while durable consumer goods showed a greater moderation, registering a negative annual variation of -25.7% in April 2023. Among the components, beverages (-41.6% Y/Y), clothing and textiles (-18.8% y/y), and tobacco (-17.4% y/y) were the non-durable consumer goods that contracted the most. In terms of durable goods, military weapons, and equipment (-38.3% y/y) and vehicles (-35.8% y/y) experienced the highest declines in April 2023 compared to the same period the previous year.

- Raw material imports amounted to USD 2,558.6 million, representing a YoY decrease of 24.7%. Within these imports, fuels, lubricants, and related products contracted by 41.4% annually, followed by raw materials for the industry with a -24.0% y/y and raw materials for the industry with a -16.8% y/y compared to the same month of 2022.

- Imports of capital goods experienced an annual contraction of 24.0% and reached a total of USD 1,313.2 million in April 2023. While capital goods for the industry and transportation equipment contracted by -25.4% and -32.0% annually, respectively, capital goods for agriculture and construction materials recorded annual growth rates of 46.0% and 8.5%, respectively.

The import balance and trade deficit during April are the result of an economic slowdown and aligned to the recent economic indicators that showed a moderation in economic and productive activity in April, particularly in the industry, manufacturing, and trade sectors, due to lower domestic demand. Additionally, inflation, after several months, peaked in May, and inflation expectations moderated for the second consecutive month over a 1 to 2-year horizon.

All these elements allow us to conclude and reinforce our call to maintain interest rates stability at 13.25% in the upcoming Central Bank meeting. This will serve as a prelude to considering possible rate cuts starting in the last quarter of 2023, to reach 12.25% by the end of the year.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.