- Colombia: Moderation in economic activity: manufacturing and retail sales decline for the second month a row

The week is coming to a close with a generally neutral to positive mood in markets after a busy period of G10 data and central bank decisions. SPX futures are a touch higher, the US curve is bear flattening but yields are coming off intraday highs, crude oil is down about 0.6% and core metals are mixed (iron ore +0.2%, copper –0.3%). The USD is stronger/weaker in a +/-0.1% band against the bulk of the major currencies where the MXN is a standout laggard, though the 0.2% drop is nothing to write home about.

The top overnight development was the expected BoJ dovish hold with unchanged guidance, and global markets will centre their attention on US U Mich inflation expectations data and scheduled central bank speakers, ahead of the US long weekend. PMI releases around the globe and rate decisions in the UK, Norway, and Switzerland, and, closer to home, in Chile, Brazil, and Mexico, are next week’s calendar highlights; those in the EM space may also await policy announcements in Hungary, Czechia, Philippines, Indonesia, Turkey, and Paraguay.

Brazilian Apr economic activity figures at 8ET are today’s Latam data headlining act, where the median economist is expecting a 2.7% y/y increase, slowing from March’s pace of 5.5% but seen increasing 0.15% m/m after an equivalent contraction in the previous month. A miss here will likely apply a lot of pressure on the BCB from government officials to cut rates next week, but we think the bank will not succumb to this and will leave its policy rate steady at 13.75%. It will likely soften its hawkish tone, however, teeing up an August start to rate reductions, as expected by the market.

Peru’s BCRP will today present its updated macroeconomic forecasts in a presentation led by Pres Velarde. At last week’s rate decision, the bank changed the wording in its statement around where it sees inflation at year-end; changing from an explicit 3% to simply saying that inflation will be close to the target range of 1–3%. We’re also interested in Velarde’s take on yesterday’s weak GDP print, which not only showed a clear impact of adverse weather but also pointed to demand-side weakness that would trend towards a need to reduce policy rates later this year.

On Peru news, the country’s Health Minister has announced her resignation amid the dengue crisis that has reportedly seen over 130k contagions and 200 casualties. Pres Boluarte also said yesterday that the matter of early elections is closed, and that she will continue to work until July 2026 in line with the constitutional mandate. We’ll watch for the public’s reaction to these statements although early election pushes in Congress look likely to continue to fail.

Finally, Mexico’s AMLO met with EU Commission Pres Von Der Leyen yesterday, agreeing to accelerate negotiations for a free trade pact. Mexico City’s head of government Claudia Sheinbaum formally leaves her post today as a step towards becoming Morena’s candidate in the 2024 presidential election.

—Juan Manuel Herrera

COLOMBIA: MODERATION IN ECONOMIC ACTIVITY: MANUFACTURING AND RETAIL SALES DECLINE FOR THE SECOND MONTH IN A ROW

On Thursday, June 15th, the DANE (National Administrative Department of Statistics) released the industry and commerce reports. Once again, manufacturing production and retail sales exhibited contractions, undershooting expectations and affirming our call for rate stability in BanRep’s June meeting.

In April 2023, the activity indicators remained in negative territory for the second consecutive month, and below market expectations in the Bloomberg survey. Retail sales declined by 6.9% year-on-year (YoY), marking the lowest figures recorded since August 2020. Similarly, the previous month’s retail sales figures in March 2023 (-7.1% YoY) also reached their nadir since August 2020. However, on a seasonally adjusted basis, retail sales (ex vehicles) exhibited a modest growth of 0.6% month-on-month (MoM) during April 2023 as compared to the previous month. On the other hand, manufacturing witnessed a YoY contraction of 6.4% for April 2023, while in seasonally adjusted terms, it experienced an MoM decline of 2.0%.

The most recent retail sales data underscores the deceleration of economic activity, primarily driven by diminished household demand, especially in the realm of durable and semi-durable goods. Concurrently, the industrial sector continues to grapple with the repercussions of escalating costs, exchange rate depreciation, and high interest rates.

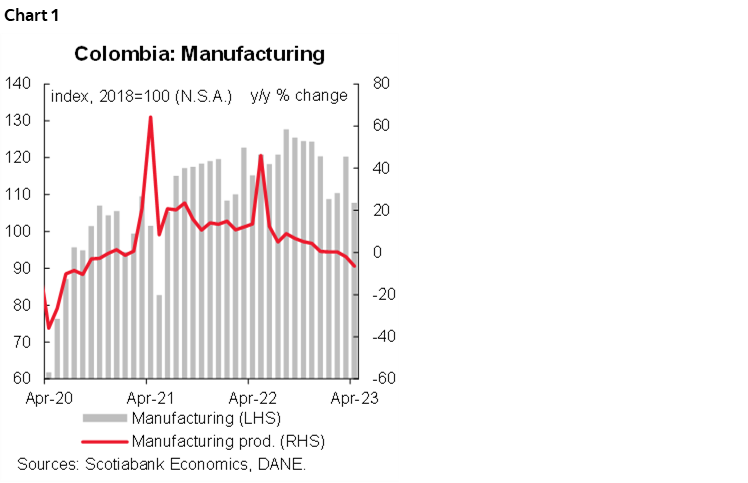

Manufacturing production

Manufacturing production contracted by 6.4% on an annual basis (chart 1), marking the lowest figures observed since August 2020 and falling short of analysts’ expectations (-3.1% YoY). In seasonally adjusted terms, a 2.0% MoM decline was registered for April 2023 reflecting the lowest figures recorded since May 2021. These outcomes reinforce the narrative of economic moderation within the country’s production, amid persistent effects, such as, elevated input costs during the initial months of 2023, subdued domestic demand, diminished business confidence, and the spectre of a global economic slowdown.

On a year-on-year basis, the sectors exhibiting better performance included glass manufacturing (12.7% YoY), electrical appliances and equipment manufacturing (11.2% YoY), and coke, petroleum refining, and fuel blending (8.6% YoY). Conversely, the sectors that faced substantial declines encompassed precious metal industries (-37.0% YoY), vehicle manufacturing (-29.9% YoY), textile products (-28.7% YoY), transportation equipment manufacturing (-21.1% YoY), and travel goods manufacturing (-21.0% YoY). Meanwhile, other significant industries experienced year-on-year contractions, particularly those associated with durable and semi-durable goods, such as travel goods manufacturing (-21.0% YoY), garment manufacturing (-12.1% YoY), footwear manufacturing (-6.8% YoY), and furniture and mattress manufacturing (-3.7% YoY).

Retail sales

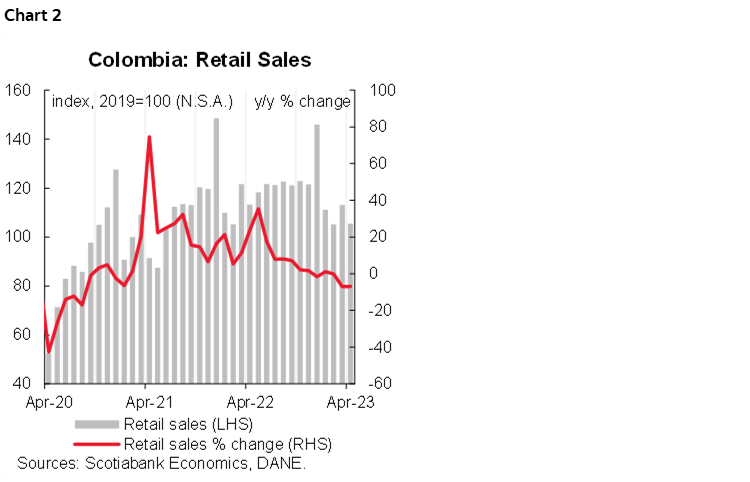

In line with the manufacturing sector data, retail sales also registered a decline for the second consecutive month, amounting to -6.9% YoY (chart 2), thereby reaching levels not witnessed since August 2020 and falling short of Bloomberg analysts’ projections (-5.6% YoY). In comparison to the preceding month, retail sales exhibited a modest variation of 0.6% MoM on a seasonally adjusted basis during April 2023. Consequently, these records attest to the moderated consumption patterns among households over the past year, remaining nearly stagnant about the previous month.

The dynamics of retail sales on a year-on-year basis in April 2023 were primarily influenced by a moderation in the sales of vehicles and motorcycles, contracting by 26.2% YoY, as well as other vehicles (-21.6% YoY) and hardware and paint products (-17.3% YoY). Conversely, non-alcoholic beverages and television sets demonstrated positive annual variations in April 2023, recording growth rates of 14.6% YoY and 9.9% YoY, respectively. However, other items, including household appliances, home cleaning products, and garments, continued to witness contractions, affirming the diminished demand for durable and semi-durable goods among households. These patterns are aligned with reduced disposable income, high interest rates, double-digit inflation rates, and limited credit availability.

Concluding remarks

The April 2023 activity data unequivocally unveils a more pronounced economic deceleration. Both retail sales and manufacturing sectors reveal a discernible moderation in the demand for durable and semi-durable goods. Our GDP growth projection for the second quarter of the year is 0.4% y/y, and 1.8% for 2023.

We estimate that this moderation trend will persist, which leads us to believe that this signal, coupled with the most recent inflation data, will be taken into consideration by the Central Bank (BanRep) to pause the tightening cycle. We anticipate that the BanRep Board will maintain the policy rate at 13.25% during this month’s meeting until the last quarter of 2023 when discussions regarding a potential rate reduction may commence.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.