- Colombia: Medium term fiscal framework: A weaker economic outlook points to a higher deficit in 2023 and 2024

Asia markets traded with a slight risk-off drift in the aftermath of the Fed’s hawkish hold yesterday, with European trading deepening the risk-averse feel in rates and equity markets. China’s central bank lowered its medium-term lending facility rate by 10bps, but this was widely expected and was not a significant risk tailwind overnight. SPX futures are down 0.4%, US yields are 4/5bps higher in the 2–10s space, crude oil is up 1%, outperforming iron ore’s 0.7% gain and copper’s 0.3% decline. The USD is broadly stronger, with the MXN among the worst performers, down 0.3% (but it’s only a scratch at these levels).

We have a decent collection of data today in Latam and the US to keep markets busy, further to the reaction to the ECB’s policy decision at 8.15ET (25bps hike expected).

In Peru, an acceleration in GDP is expected in April data out at 11ET, but the expansion may now prove disappointing versus what our economists had expected until recent comments from Fin Min Contreras. As our team wrote in Friday’s Latam Weekly: “Our high hopes for a more normal figure, with growth rate between 1.3% to 2.0% y/y, have been shot down by comments made by Finance Minister Carlos Contreras that GDP growth would likely be around 0.7% y/y in April.” The median submission to Bloomberg looks well off the mark in relation to those comments, expecting a 1.7% y.y gain. May unemployment rate data out at the same time is expected to show a decline to 6.8% from 7.1% according to our economists (vs 7% median).

Colombia’s DANE will release industrial/manufacturing production and retail sales data at 11ET that are expected to show continuing economic weakness. However, the market will likely focus on yesterday’s Medium Term Fiscal Framework presentation (see below) for moves in local markets. BanRep also publishes today the results to its economists survey.

In Brazil, April services activity figures out at 8ET came in weaker than expected, but with a nice positive revision to March, though signs of economic weakness would firm up pricing for an August rate cut (currently between 25 and 30bps). It will be political and fiscal developments that may be more interesting to follow. Yesterday, S&P revised the country’s outlook to positive from stable (leaving it at BB-, i.e. not IG) owing to the country’s new fiscal framework plans that ultimately have not been as loose as feared—while we wait for the final policy to take shape. Tax news (state sales tax reform and payroll tax cuts extension) are also worth watching.

Finally, Banxico’s report on regional economies out at 14ET could shed some light on the varying performance of the various regions and how each has possibly benefited, or not, from near/friendshoring.

—Juan Manuel Herrera

COLOMBIA: MEDIUM TERM FISCAL FRAMEWORK: A WEAKER ECONOMIC OUTLOOK POINTS TO A HIGHER DEFICIT IN 2023 AND 2024

On Wednesday, June 14th, the Ministry of Finance (MoF) released the Medium-Term Fiscal Framework (MTFF), Colombia's most relevant fiscal-policy publication. It provides the clearest insights into the government's thinking about the country's economy in the long run and current fiscal results. In fact, it gives a general perspective on the most important factors influencing the main fiscal goals and their sustainability over a ten-year framework.

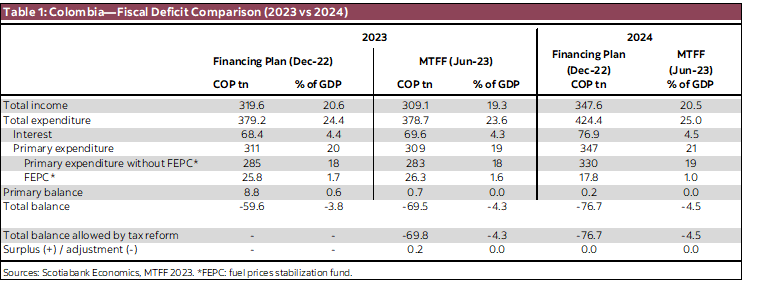

The MTFF-2023 revealed a more cautious approach from an economic perspective, which will increase the fiscal deficit in 2023 and 2024. The Min Fin expects weaker fiscal income than the projection in the financing plan released in December 2022 (table 1).

This weaker economic context involves a lower tax collection from trade activity (lower imports) and more moderate oil prices. The fiscal deficit for 2023 is now estimated at 4.3% of GDP, increasing from the initial estimate of 3.8% of GDP, which means that Colombia will no longer achieve a primary surplus of 0.6% and instead will be neutral in that regard posting a 0% of the primary balance.

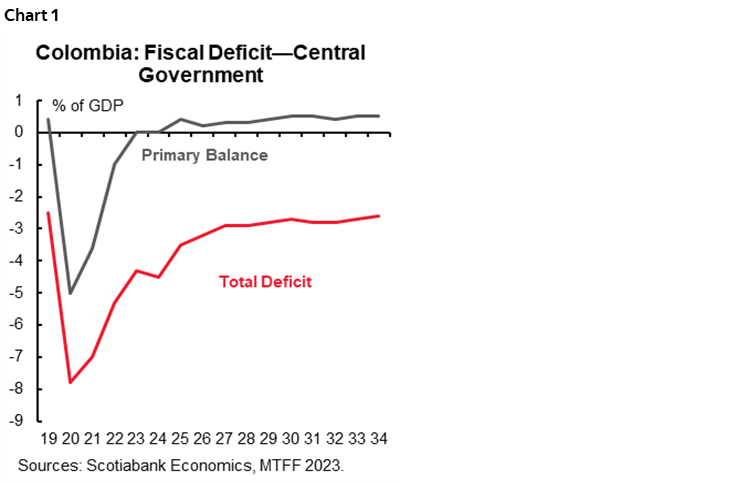

The previous change in the fiscal deficit target for 2023 has been anticipated since the discussion of budget addition; that said, the big surprise came from the fiscal deficit estimation for 2024, which now points to a deficit of 4.5% of GDP, increasing versus 2023 and increasing versus the most recent guidance in the MTFF-2022 of 2% of GDP (chart 1)

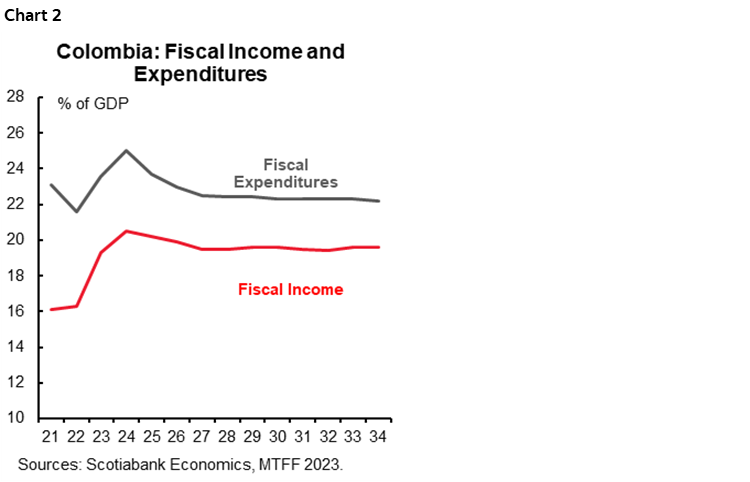

Deterioration in deficit perspectives is motivated from a weaker economic perspective since economic growth is expected to decelerate from 1.8% in 2023 to 1.5% in 2024 and higher fiscal spending, which is expected to represent 25% of GDP (chart 2) vs. the estimation in the MTFF-2022 of 21.5% of GDP.

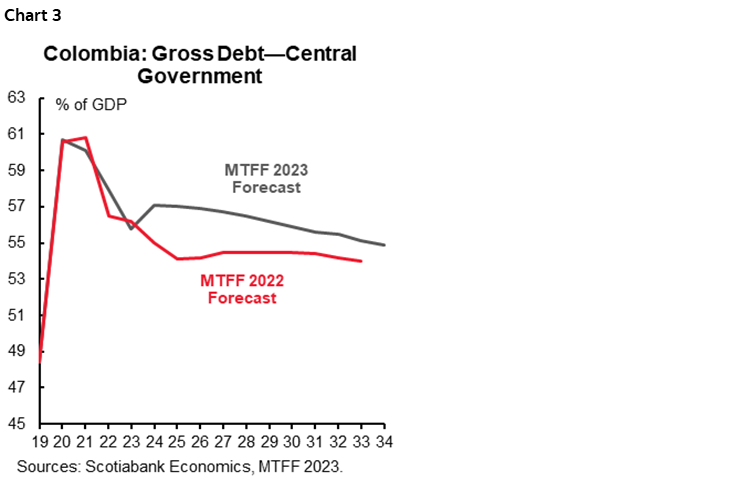

All in all, debt to GDP is expected to close at 55.8% of GDP in 2023, closer to the longer anchor of the fiscal rule. However, in 2024, debt will jump to 57.1% of GDP (chart 3).

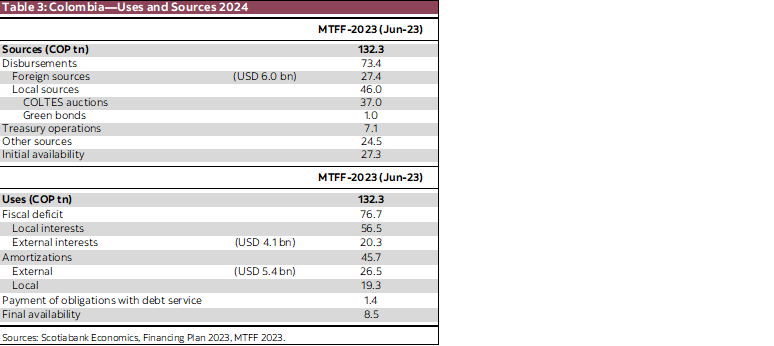

The previous dynamic means more financing needs in 2023 and 2024. COLTES issuances in 2023 are expected to increase by around COP 7 tn due to the pre-financing of the 2024 obligation, while the excess deficit of 2023 will be financed using foreign sources. Ahead of 2024, issuances in the COLTES market are projected to increase to COP 37 tn (+COP 10 tn higher than in 2023, ~2% of GDP).

Fiscal perspectives point to an interruption in the convergence process to the long-term level of debt to GDP ratio of 55%. Despite having achieved the approval of an ambitious fiscal reform, expected spending is increasing at a higher pace. Previous development is a headwind to achieving a better credit rating in the medium term, which probably will maintain a higher risk premium in COLTES. We think markets can absorb new issuances. However, fiscal perspectives could result in a curve with higher slope since issuances are more concentrated in the long-end tenors.

Either way, in forthcoming months, the peak in inflation and the potential pause in BanRep’s hiking cycle could contribute to maintaining value in the COLTES market. As mentioned before, the fiscal picture probably will affect the slope of the curve but not significantly the level.

On the positive side, we see macro projections in the MTFF-2023 are more conservative, which probably would prevent sudden changes in fiscal plans in forthcoming publications. Questions that are still in the air is the related to the fiscal cost of social reforms. On the other side, a thing to pay attention to is the budget execution. In 2023, COP 30 tn (~2.8% of GDP) wasn’t executed, while in the YTD of 2023, budget execution, excluding interest payments, is at its lowest level since 2001 ( ~21% of execution).

Minister Bonilla highlighted that MTFF-2023 is complying with the fiscal rule mandate. However, it is important to wait for the Autonomous Fiscal Rule Committee statement to see their opinion about the previous plan.

Further details about today’s publication.

Macro assumptions:

- Economic growth was revised to the downside in 2024. In 2023 the composition of the GDP points to a lower trade balance, which plays against the tax income from imports (table 2).

- Oil prices projection is more conservative. However, oil production is expected to increase.

Fiscal deficit :

- The fiscal deficit target increased on the Government’s horizon. A more modest perspective of economic growth and a path of high spending is leading those forecasts to the upside.

- Debt to GDP in 2023 is expected to decrease from 57.9% in 2022 to 55.8%, however, it will rebound in 2024 to 57.1 of GDP, still close to the anchor defined in the fiscal rule, but interrupting the reduction trajectory. Something which could maintain Colombia with low possibilities of gaining the investment grade in the medium term.

Oil stabilization fund:

- Minister Bonilla said that in six months, the increases in gasoline prices would be done; either way, diesel prices remain below the fair value, and the stabilization fund for oil prices will have a deficit of COP 17.8 tn (lower versus the 2022 deficit of COP 36.7 tn).

Financing Plan 2023:

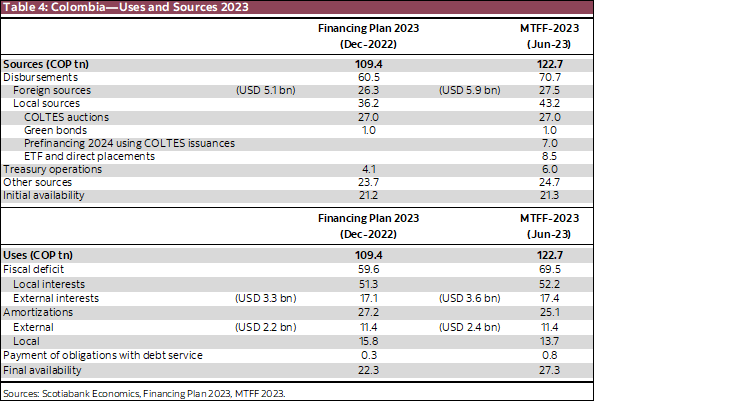

- Comparison between projections from the Fiscal Plan 2023 (December 2022) and MTFF 2023 (today).

- The expected fiscal deficit in 2023 increased by COP 10 tn. Financing will come from higher external indebtedness (+ COP 3.2 tn / +USD 820 million vs. Financing Plan projection). Liability management operations (+ COP 1.9 tn), COP +1 tn from other sources, and around COP 4 tn from domestic sources, which will be related to the disbursements associated with the COLTES ETF (table 3).

- In 2023, COLTES auctions are expected to increase by COP 7 tn as a pre-financing operation for 2024. That said, issuances won’t stop at COP 27 tn, instead will reach COP 34 tn, which is the usual number the market has managed with in the past, and it could lead to the end of auctions between October/November 2023.

Financing Plan for 2024:

- The MoF estimates fiscal income of around 20.5% of GDP, which is above the 19.3% of GDP in 2023 (table 4).

- On the other side, fiscal expenditures are expected to represent 25% of GDP, above the 2023 expectation of 23.6% of GDP.

- The primary balance is expected at 0.0% of GDP (chart 1 again), while the total deficit will increase to 4.5%, which is still in compliance with the fiscal rule, according to the Ministry calculations. However, our take is less constructive since the government is interrupting the convergence towards a lower debt level.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.