- Colombia: April unemployment rate was higher than expected, reaching 10.7%

- Peru: May inflation could be the last close to 8% y/y

The release of a surprising increase in China’s private manufacturing PMI and the passage of the US debt ceiling bill gave overnight markets a bit of a hand to take SPX futures 0.2% higher on the day and lifting US yields from yesterday’s lows to see the curve bear flatten. Crude oil is flat, weighed by a large build-up in inventories reported by the API and reports that OPEC+ won’t announce another supply cut this weekend, as it underperforms the Chinese data-led gains in iron ore and copper of ~3.5% and 2.5%, respectively.

The USD has fluctuated between gains and losses against the majors, but more clearly losing ground in European trading, though here the MXN is missing out to trade unchanged at writing against gains in the CAD, AUD, and EUR, among others.

Yesterday, Banxico officials provided their opinion on monetary policy and the outlook with the release of the bank’s quarterly inflation report. GDP growth for 2023 was upgraded to a 2.3% expansion from 1.6% previously on the back of a solid Q1 print, but this came at the expense of a lower 2024 projection, now at 1.6% from 1.8%.

Gov Rodriguez indicated that at least the next two meetings will see an unchanged policy rate, comments echoed by DG Espinosa who also noted that there’s not enough evidence on whether ‘nearshoring’ is a clear trend. DG Heath also said that he doesn’t believe that rate differentials are behind the strength in the MXN, and that when Banxico rate cuts come these would likely take place around the time of Fed policy easing—so capital flows should not be materially impacted then. We’ve already got a lot of colour from Banxico officials yesterday, and there’s little doubt that the bank will stick to its current guidance, so we may not get too much new news from today’s minutes out at 11ET aside from more fleshed out individual views. The release of Banxico’s economists survey results at the same time will lay out the split among economists on the timing of the first rate cut.

At 8ET, Brazil publishes Q1 GDP data that the median economist expects will show a 3.1% y/y and 1.2% q/q rise in output, in a strong performance after the economy contracted 0.2% q/q to close out 2022. Thirty minutes later we get Chilean monthly GDP which should show another year-on-year contraction. Still, the 0.5% decline seen by the median is significantly smaller than the large 2.1% drop in March. Our team in Santiago projects a larger 1.2% y/y contraction on the back of a 0.7% m/m retracement in April, which they say “could be the first negative surprise in economic activity in relation to the BCCh’s baseline scenario.”

The top release of the day will be Peruvian inflation at 11ET, covered by our Peru economists below. We project a 7.9% y/y increase from 8% in April (in line with the consensus median) that could mark the last reading close to the 8% mark ahead of sharper decelerations in June and July.

We also await Boric’s annual address to Chilean congress at 11ET.

—Juan Manuel Herrera

COLOMBIA: APRIL UNEMPLOYMENT RATE WAS HIGHER THAN EXPECTED, REACHING 10.7%

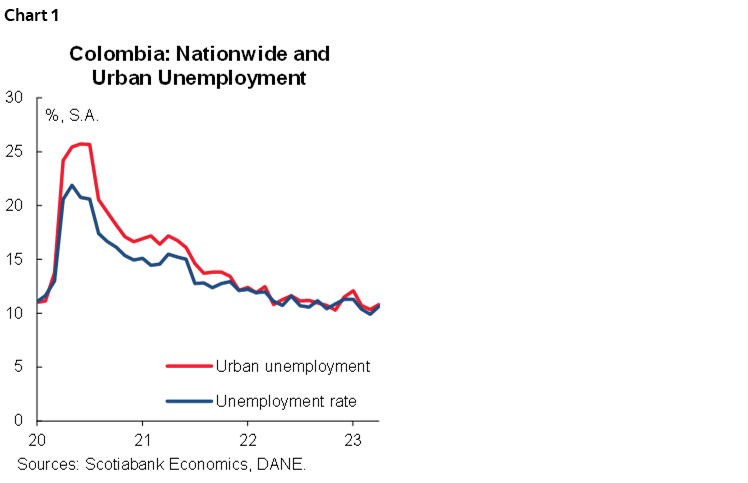

Employment data released on Wednesday showed the nationwide unemployment rate at 10.7%, and urban unemployment at 11.1% in April 2023, above our forecast of 10.0% for the national and 10.3% for the urban unemployment rates. On a seasonally adjusted basis, unemployment is up in both readings, nationwide it went up to 10.6% y/y in April from 9.9% in March, while in urban areas, it increased from 10.3% y/y to 10.8% y/y (chart 1). On the other hand, the labour force continues to increase on a y/y basis. The participation rate was 64.6% in April vs. 63.6% in the same month of 2022, levels up for the April 2019 figure of 64.2%.

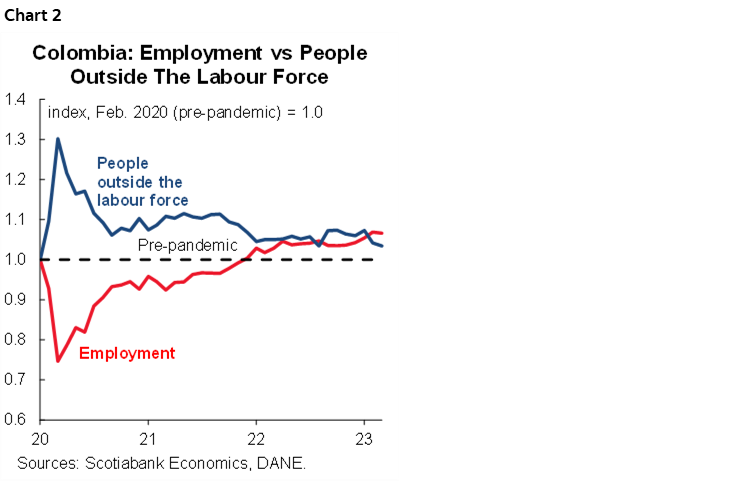

There was an increase in the number of people employed in April compared to Apr 2022 (+785 thousand employed), mainly in the male population in the main cities. However, the people employed compared to the last month registered a fall (-52 thousand employed). In April, the number of people outside the labour force decreased from Apr 2022 (-212 thousand y/y), changing the dynamic observed up to February 2023, when inactivity showed the biggest change since the beginning of 2021 (chart 2).

On a y/y basis, jobs increased by 785 thousand in April 2023. Five sectors accounted for 92.9% of job creation: hotels and restaurants (+196 k), agriculture (+184 k), manufacturing (+162 k), public administration, education, health (+118 k), and construction (+68 k). The previous picture also shows that the employment recovery is concentrated in urban areas (46.6% of job creation). However, the commerce and vehicle repair sector registered a negative variation compared to April 2022 (-58 k).

Regarding the employed population according to occupational position, in April 2023, self-employment and private employee were the occupational positions that contributed the most positively to the variation of the employed in the national total, with +405 k employed and +227 k employed, respectively.

In April 2023, the gender gap slightly deteriorated compared to the previous April. The female unemployment rate was 13.9%, below the 14.2% observed in April 2022, while male unemployment fell from 8.9% in Apr 2022 to 8.4% in Apr 2023. That said, the gap between female and male unemployment increased to 5.6 ppts from 5.3 ppts since Apr 2022.

Regarding labour quality, most of the job creation was concentrated in the formal sector in April (+830 k vs April 2022), allowing an improvement in the informality ratio from 58.0% in April 2022 to 55.8% in April 2023, the most significant improvement was in urban areas passing from 44.4% to 41.0%.

In summary, the labour market is showing a slowdown dynamic; however, employment increase remains concentrated in services-related sectors and agriculture-related sectors, which offset the weakening in other sectors like commerce that reflects more materially the economic slowdown.

Previous results support the hypothesis of stability in the policy rate for the next June 30 meeting. Having said that, we do not believe that the Board will close the door to new hikes if necessary. One way to do the former is not having a unanimous decision. Additionally, the next inflation report will be the most important indicator to define a skew on BanRep’s potential decision.

—Sergio Olarte, Santiago Moreno, & Jackeline Piraján

PERU: MAY INFLATION COULD BE THE LAST CLOSE TO 8% Y/Y

We expect inflation in May to be close to 0.30% m/m, lower than that of April (0.56% m/m) and that of May 2022 (0.38% m/m), with which the year-on-year rate would move away slightly from almost 8% posted in April.

According to the monitoring of key prices that we carry out, we see a moderation in poultry prices—affected in recent months by the effects of avian flu—in the prices of perishable foods and lower prices of local fuels, in line with the decline in the oil’s international price. Core inflation would be around 0.2% m/m, with which the annual pace would show a more visible decline, going from 5.7% to 5.2% y/y.

May could be the last month with high year-on-year inflation (close to 8%), since starting in June we anticipate a more visible decline in the downward inflation trajectory, closer to 7%, as a result of a high statistical base of comparison (June 2022 inflation was unusually high: 1.19% m/m compared to the average for the months of June of the last 20 years: 0.17%) and due to the fading of the avian flu effects on poultry prices (with a significant weighting in the consumption basket). The BCRP has remained in monetary pause mode for the last four months and we expect it to continue in that stance until inflation does not decline with greater conviction.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.