- Colombia: May exports maintain downtrend amid commodity prices moderation

- Mexico: Dynamism in consumption remains while construction investment lags

After the release of the Fed’s meeting minutes yesterday, it’s the BCCh’s, Banxico’s, and BanRep’s turn to publish the account to their June monetary policy decisions. The recap of deliberations by US officials did not surprise significantly, but did have a slightly more hawkish feel that ultimately weighed on overnight markets.

A risk averse mood has global rates and US equity futures weaker (-0.5% in SPX contracts), but the USD (BBDXY flat, MXN down 0.4%) and commodities are mixed (oil and iron ore about +0.5%, copper –0.9%). International markets await a deluge of US data, starting at 8.15ET with ADP jobs, followed by jobless claims, international trade, JOLTS vacancies, and ISM services figures—and looking ahead to tomorrow’s nonfarm employment release.

Policymakers at each of the BCCh, Banxico, and BanRep left rates on hold last month and, at least for two of them, their debates likely centred on how long settings should remain at current levels.

After a cumulative 1,150bps in hikes since October 2021, BanRep voted unanimously in favour of a pause for the first time in the cycle, so there may not have been an in-depth discussion of rate cuts timing at this meeting, but the conditions needed for these to take place may have been laid out.

The BCCh meeting definitely had the most active back-and-forth, simply evidenced by the fact that two of five board members (Garcia and Griffith-Jones) voted for a 50bps reduction then; a July rate cut seems highly certain and trending towards a 50bps size (markets are eyeing 75bps). Tomorrow’s inflation print and economist/traders surveys out next week should lock in expectations for the July 28 meeting. On the data front today, Chile’s May wages release could show the first single-digits y/y increase since last July (with base effects helping).

Banxico’s decision was perhaps the least uneventful of the three but it will help to know where each official stands on how many months/meetings the pause could last. To that point, if some are worried about what the Fed does and whether to take that into consideration then yesterday’s hawkish FOMC minutes would push the first Banxico rate cut until 2024.

—Juan Manuel Herrera

COLOMBIA: MAY EXPORTS MAINTAIN DOWNTREND AMID COMMODITY PRICES MODERATION

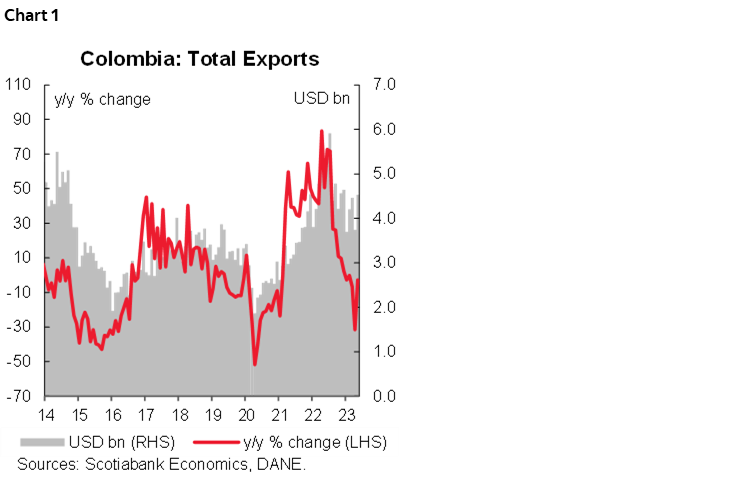

The National Administrative Department of Statistics (DANE) released the export information on Wednesday, July 5th. Monthly exports, as of May 2023, amounted to US$4,531.2 million FOB, showing a year-on-year decrease of 2.8% (chart 1). This marks the fifth consecutive month of YoY negative growth, albeit with a slight improvement compared to the sharp decline recorded in April 2023 (-31.5% YoY).

This result was mainly driven by a 9.1% YoY decrease in external sales of Fuels and products from extractive industries, followed by a 3.1% YoY contraction in Agricultural, Food, and Beverage products in May. On the other hand, the Manufacturing sector and other sectors recorded annual growth rates of 6.3% YoY and 26.2% YoY, respectively. Additionally, in May, Fuel and products from extractive industries accounted for 49.7% of the total FOB value of exports, followed by Manufactured Goods at 20.9%, Agricultural, Food, and Beverage products at 22.0%, and Other sectors at 7.3%.

This latest result continues to highlight the moderation in commodity prices compared to the previous year, particularly in oil and coal exports. Consequently, this could pose a hurdle for dollar-denominated exports, potentially slowing down the reduction of the external deficit.

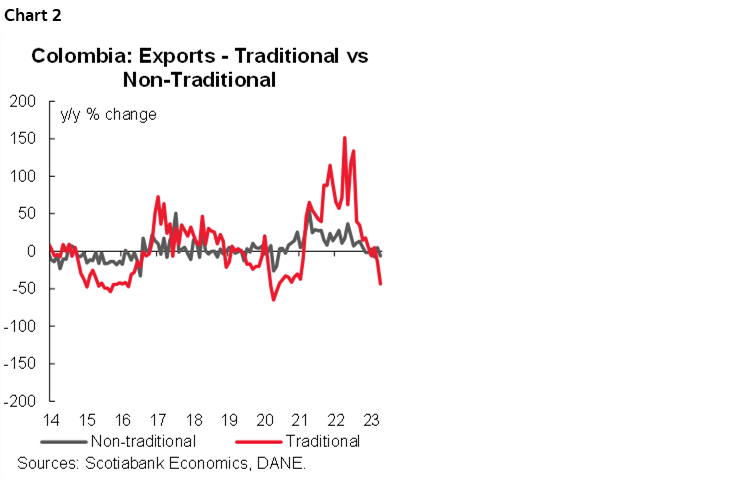

- Traditional exports (related to coffee, oil, and mining—chart 2) contracted by 10.2% YoY in May 2023 (USD 2.5 billion FOB). This performance is primarily explained by lower international prices, while volumes showed positive variations compared to the same period in 2022 (8.6 million metric tons and an annual growth of 56.3% YoY in May 2023).

- Among the components of traditional exports, the largest decline was observed in oil and its derivatives, which dropped by 34.1% YoY in May (USD 1.2 billion FOB), followed by coffee with a contraction of 7.9% YoY (USD 242 million FOB). In terms of volumes, oil exports showed a 6.9% YoY growth (2.8 million metric tons), while coffee exports increased by 12.2% YoY (46 thousand metric tons) in May. Coal and ferronickel exports exhibited positive annual variations in both value and volume. Coal exports reached 5.7 million metric tons in May (+104.2% YoY) with a value of USD 915 million FOB (+69.6% YoY), while ferronickel exports amounted to 17 thousand metric tons (+69.5% YoY) valued at USD 80 million FOB (+0.5% YoY).

- Non-traditional exports, on the other hand, recorded an annual growth of 7.7% in May, totaling USD 2.1 million FOB.

Finally, given the ongoing deceleration of the Colombian economy, the appreciation of the exchange rate, and the decline in imports, the outlook for exports is expected to continue presenting challenges in the coming months. The reduction in global demand and lower commodity prices could adversely affect the revenues generated by traditional exports such as oil and coffee. Furthermore, the appreciation of the national currency may hamper the competitiveness of Colombian products in international markets.

Therefore, under this scenario, the pace of reducing the current account deficit may lose momentum in the coming months, despite the latest import data, which already shows declines exceeding 20% for April.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

MEXICO: DYNAMISM IN CONSUMPTION REMAINS WHILE CONSTRUCTION INVESTMENT LAGS

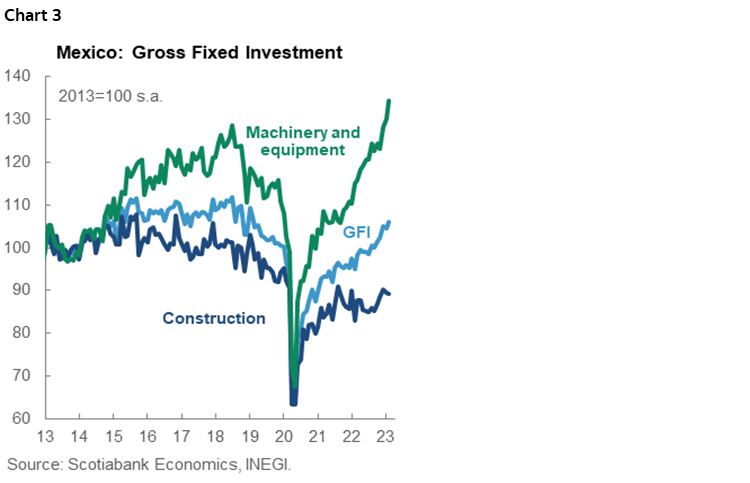

In April, gross fixed investment slowed on an annual basis, going from 9.0% to 6.1% y/y. Machinery and equipment moderated to 13.3% (16.0% previous) with 26 consecutive annual increases, the national subcomponent decelerate to 13.9% (17.2% previous), the imported one to 13.0% (15.3% previous) (chart 3). Construction stopped to 0.1% (2.8% previous), the residential subcomponent fell -10.7% (0.4% previous), despite non-residential construction rising at 10.6% (5.1% previous). In the seasonally adjusted monthly comparison, gross fixed investment fell -0.3% m/m (0.5% previous), as construction fell -2.1% (0.6% previous) and machinery and equipment increased to 2.3% (0.5% previous). Despite the somewhat big annual advances observed since Q1, investment remains close to levels observed in 2013. In this sense, the construction component has been especially weak, which remains below pre-pandemic levels and we do not expect a major recovery in the short term, despite optimism around the nearshoring.

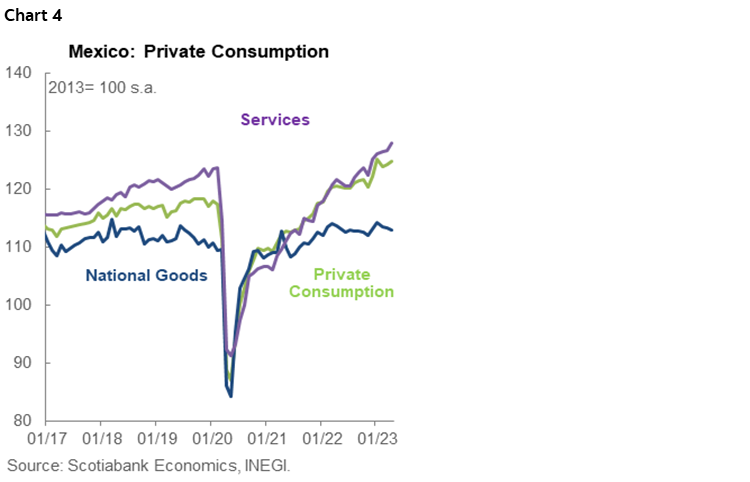

In April, private consumption moderated its pace in real annual terms, from 3.3% to 2.5% y/y (chart 4). Domestic goods fell -2.3% (-0.5% previous), imported goods slowed to 7.7% (10.2% previous), and domestic services increased to 5.6% (5.0% previous). In its seasonally adjusted monthly comparison, private consumption increased 0.5% m/m (0.3% previous), derived from the fact that services rose 1.0% (0.2% previous), as imported goods moderated 2.8% (3.7% previous), and national goods fell -0.4% (-0.1% previous). Despite the moderation in overall private consumption, the market anticipates that services will continue to be the driving force behind consumption growth, supported by a strong labour market and still solid remittances, this trend has been consistent throughout the year and is expected to persist in the coming months. Given the weight of consumption in the economy (around 70% of GDP), the positive outlook of this indicator supports upward revisions in GDP, which at this time the forecasts at 2.26% for 2023 in the Banxico survey.

—Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.