- Colombia: Imports moderated for seventh consecutive month in May

The PBoC’s strong CNY fix, more support measures floated in China, and a beat in Aussie jobs carried markets overnight ahead of relatively quiet Europe and Americas calendars. Aside from a couple of outsized movers in FX markets, today’s USD mood is mixed in +/-0.2% ranges against most majors (the MXN lags, down 0.3%), while rates markets suffer losses on nothing obvious but continuing yesterday’s US hours weakness.

US equity futures are on the backfoot, especially in tech due to a Tesla profit warning and chipmaker TSMC guiding overnight a weaker than expected sales outlook and pointing to a less encouraging economic backdrop than three months ago (highlighting China). Oil prices are flat, while copper (+1.7%) and iron ore (+2.5%) get a nice lift from reports that authorities in China are looking into relaxing restrictions on home buyers and a China NDRC official saying that specific measures will be announced soon to support the private economy.

We close out the Latam data week today with Mexican retail sales for May out at 8ET and later in the day the results of the latest Citibanamex survey of economists. Tomorrow’s regional calendar is bare of data or events but next week starts with the key release of Mexican H1-Jul CPI. That print will ultimately prove much more important for markets and Banxico expectations than May retail sales that are seen little changed m/m (+0.1%) while holding roughly around the year-on-year growth pace recorded in April (at 3.5% vs 3.8%).

Colombian markets are closed today for Independence Day but that doesn’t mean we won’t monitor developments in the country. Yesterday, Mining and Energy Minister Velez resigned her post amid accusations of influence peddling and we’re on the lookout for who will replace her at the head of this key ministry. Velez had advocated for no more extraction/exploration permits in the country’s oil and gas sector, so her departure could open the door for someone more market friendly to take her seat that would provide an additional tailwind to Colombian assets. On the other hand, Pres Petro could also choose someone that shares Velez’s policy goals—but whether these can be realized remains to be seen.

In Peru, protests yesterday against the Boluarte government (that may continue in smaller numbers today) were relatively ordered and non-violent with only pockets of clashes and limited disruptions far from those seen earlier in the year after then-President Castillo’s arrest in December.

—Juan Manuel Herrera

COLOMBIA: IMPORTS MODERATED FOR SEVENTH CONSECUTIVE MONTH IN MAY

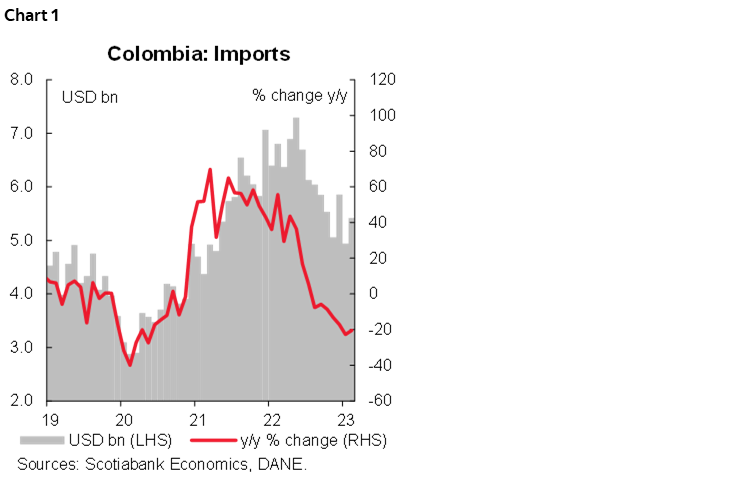

On Wednesday, July 19th, the DANE (National Administrative Department of Statistics) published the import data for May 2023, which amounted to USD 5.4 billion CIF, representing a seventh consecutive month of annual contraction with a YoY decline of 20.4% compared to May 2022 (chart 1). This decline was primarily driven by a 17.8% decrease in manufactured goods, which contributed -12.5 p.p. to the overall variation.

In May 2023, manufactured goods accounted for 72.6% of the total CIF value of imports, followed by agricultural, food, and beverage products at 15.3%, fuels, and extractive industries at 12.0%, and other sectors at 0.04%.

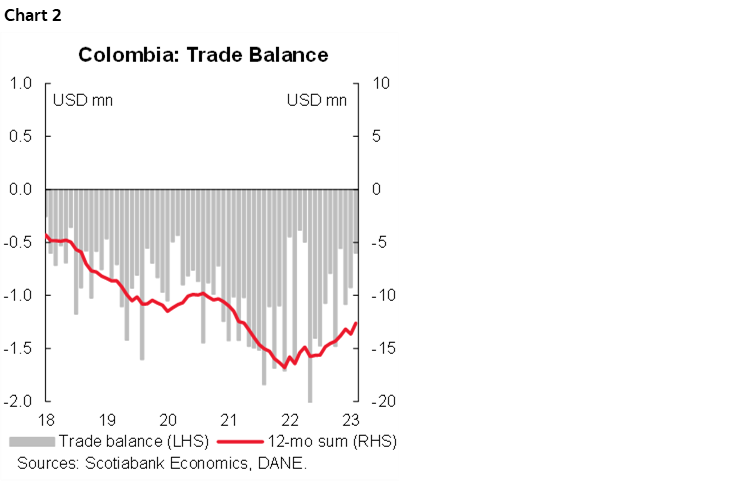

Regarding Colombia’s trade balance, a deficit of USD 599.2 million FOB was recorded in May 2023 (chart 2), compared to a deficit of USD 1.6 billion FOB last year. Therefore, the trade deficit decreased by 35.1% on a month-on-month basis (a deficit of USD 923.3 million FOB in April 2023).

The import data for May aligns with the gradual moderation of economic activity, inflation moderation, and the appreciation of the exchange rate, reaffirming our estimation that BanRep will maintain a stable monetary policy interest rate in the upcoming July meeting.

Regarding product groups, imports of manufactured goods in May 2023 amounted to USD 3.9 billion CIF, representing a year-on-year decrease of 17.8%. The second largest import group was fuels and extractive industries, with imports amounting to USD 651.0 million CIF, experiencing a contraction of 36.4% YoY. Within this group, petroleum, petroleum derivatives, and related products contributed the most to the decline (-36.3%), accounting for -31.5 percentage points of the total group’s variation. The third largest import group was agricultural, food, and beverage products, with imports amounting to USD 830.2 million CIF, representing a decrease of 13.4% YoY in May 2023.

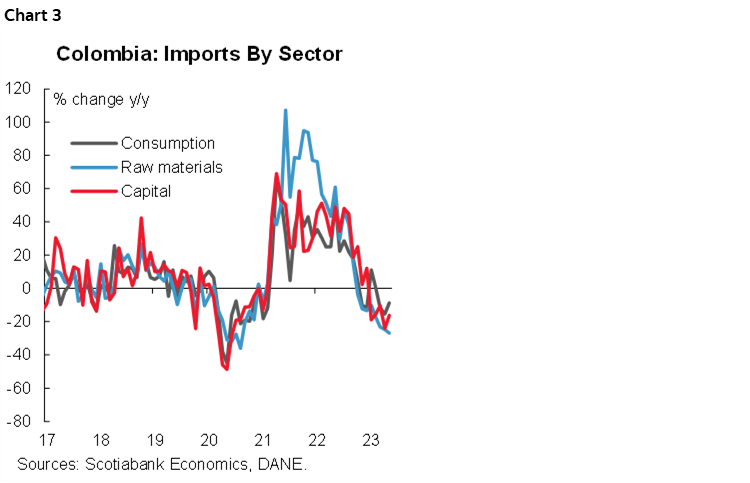

From the perspective of imports by economic use or destination, all three major groups remained in negative territory (chart 3):

- Imports of consumer goods amounted to USD 1.2 billion CIF, contracting by 8.7% YoY in May 2023. Non-durable consumer goods decreased by 8.0% YoY, driven by declines in beverages (-26% YoY), clothing and textiles (-25.2% YoY), food products (-19.4% YoY), and other goods (-10.2% YoY). As for durable consumer goods, they declined by 9.5% YoY, mainly due to decreases in weapons and military equipment (-98.9% YoY), domestic appliances (-34% YoY), furniture and household equipment (-13.9% YoY), and domestic utensils (-9.2% YoY). However, vehicle imports experienced an annual growth of 7.7% YoY in May 2023.

- Imports of raw materials and intermediate goods amounted to USD 2.6 billion CIF, representing a decrease of 26.9% YoY in May 2023. Notably, there was a 36.9% YoY decline in imports of fuels, lubricants, and convex products. This was followed by a 25.6% YoY contraction in raw materials and intermediate goods for the industry (excluding construction), and a 9.1% YoY decrease in raw materials and intermediate goods for agriculture.

- Imports of capital goods reached a value of USD 1.6 billion, experiencing a contraction of 16.2% YoY in May 2023. This decline was driven by decreases in transportation equipment (-21.5% YoY), capital goods for the industry (-14.6% YoY), and construction materials (-10%). On the other hand, imports of capital goods for the industry grew by 15.4% YoY in May 2023.

The May imports balance and trade deficit reflect the gradual adjustment process underway in the Colombian economy, aligning with the recent results for economic activity in May. Therefore, considering the appreciation of the exchange rate, inflation reduction, improved consumer confidence data, and the moderation of inflation expectations, Scotiabank Economics expected that the Central Bank will maintain stable interest rates at least until the fourth quarter of 2023.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.