- Peru: BCRP holds key rate for the sixth consecutive time and was cautious about future steps; Chilly May in Peru data out tomorrow

Final trading hours in Asia ahead of the Japanese long weekend had the dollar and rates markets trimming, or consolidating, some of the moves seen over the week after a mostly uneventful overnight session that spilled over into quiet European trading. The USD is mixed to stronger against the major currencies, where the MXN is one of the worst performers, down 0.3%, but still well on track to close below the 17 pesos mark this week.

US equity futures are a bit weaker (-0.1% in SPX), as is crude oil down 0.3% (though holding the bulk of gains on Libya oil field risks) and copper -0.7% that contrast with a strong 4.6% jump in iron ore that owes to comments by a PBoC official that ‘tailored’ real estate support is coming. This comes ahead of Chinese Q2 GDP data due for publication on Monday, projected at 7.1% (from 4.5% in Q1), that will likely play a key role in the performance of Latam assets early next week.

The G-10 day ahead presents as main events the release of US trade price indices and the U Mich survey which can deliver an unexpected beat/miss in inflation expectations, and a speech by Fed dove Goolsbee as the last scheduled speaker prior to the start of the pre-meeting communications blackout period starting tomorrow.

In Latam, we have retail sales data from Brazil and Colombia to monitor, at 8ET and 11ET, respectively, with the latter’s accompanied by manufacturing/industrial production figures. The collection of today’s Colombian data should give us a decent idea of where next week’s May economic activity print will come in and deepening economics weakness could augur an earlier start to rate cuts by BanRep which meets on the final day of the month (no change expected).

Peru’s BCRP has a presser at 13ET to discuss yesterday’s decision to leave its reference rate unchanged at 7.75% that maybe left a bit to be desired in terms of highlighting economic weakness. Below, our Lima team gives their view on the bank’s announcement as well as preview tomorrow’s release of GDP and unemployment rate data for May and June, respectively.

—Juan Manuel Herrera

PERU: BCRP HOLDS KEY RATE FOR THE SIXTH CONSECUTIVE TIME AND WAS CAUTIOUS ABOUT FUTURE STEPS

The board of Peru’s Central Bank (BCRP) kept its reference interest rate unchanged at 7.75% this Thursday, in a decision widely expected by the market consensus and by us, for the sixth consecutive time. As usual, the BCRP kept its options open for future changes in monetary policy, although its statement reflected caution regarding the next steps.

The BCRP specified in its statement that it expects inflation to reach the target range (between 1% and 3%) at the beginning of next year, which suggests that the BCRP would maintain its interest rate at the terminal level for longer. The statement reflects signs of caution, noting that although the transitory effects on inflation due to supply restrictions on some foods began to dissipate in June, it emphasized that there are risks associated with climatic factors (mainly El Niño Phenomenon).

We expected more regarding the economic weakness. The BCRP indicated that the leading indicators and expectations about the economy deteriorated in June, remaining in a pessimistic zone. There was no more discussion of the economic backdrop. We hoped that in the statement they showed concern about the weak economic performance that accumulated six months to May. This could have given a signal that the BCRP would be open to a possible advance in the interest rate cut cycle. The reading of inflation and its expectations for July will be key to confirming the rate of decline in inflation. Inflation expectations for 12 months fell from 4.2% to 3.8%, according to the latest BCRP survey, a visible decrease, although still above the target range (between 1% and 3%). The survey also showed that 24-month forward inflation expectations were lowered from 3.1% to 2.9%, reflecting that the consensus still sees that the return of inflation to the target range could take time. Inflation remains outside the target range for 25 months, a record sequence that reflects the intensity of the recent supply shock. In June, more than 60% of the prices of the consumer basket posted increases, a proportion that has been maintained throughout the year.

The monitoring of key prices that we carry out suggests some recovery in prices in July, mainly food (including poultry prices), to which seasonal factors are added. The comparison base effect will still be important, but to a lesser degree than in previous months. With this, we believe that year-on-year inflation in July is likely to be closer to 6%. Other important inflation indicators continued to show a clear downward trend. Wholesale inflation continued to fall, going from 1.6% y/y to 0.5% y/y in June, suggesting less cost pressure in the future, in line with lower imported inflation (which went from 2.8% y/y to 0.6% y/y in June) and a greater appreciation of the PEN (close to 3% y/y). Our inflation forecast remains at 5.00% by end-2023.

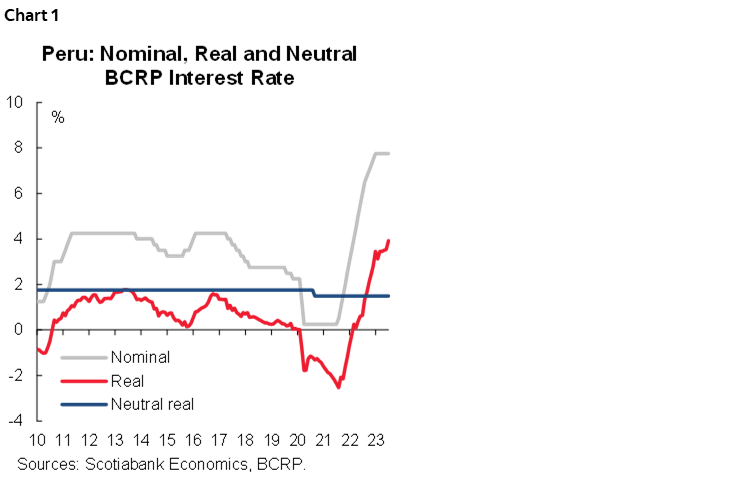

We also maintain our expectation that the BCRP will keep the reference rate at 7.75% until Q3-23, lowering it to 7.25% in Q4-23 and will continue to relax it to a level close to 5.25% by the end-2024. The real interest rate rose from 3.5% to 3.9% (chart 1), well above the neutral level (1.50%) for eleven consecutive months, which means an even more restricted monetary stance, after having remained around 3.5% for the last six months.

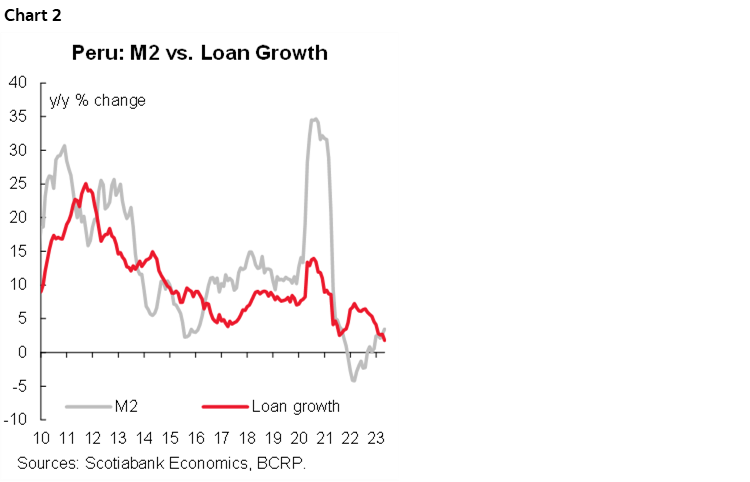

Liquidity growth in soles (M2, chart 2) continued to recover and went from 2.7% to 3.5% in May, remaining in positive territory for the ninth consecutive month, while credit expansion weakened and went from 2.7% to 1.8% in May, in line with the weakness of the economy. The BCRP statement also confirmed that the outlook for global economic activity points to moderation, although global risks remain due to restrictive monetary policy in advanced economies and ongoing global conflicts.

—Mario Guerrero

CHILLY MAY IN PERU DATA OUT TOMORROW

On Saturday, July 15th, the official GDP growth figure for May will be released. The number will not be pretty and is more likely to fall on the negative side of nil, than on the plus side. This is where we would be tempted to insert an emoji with a sad tear, if only our editors would allow it. [editor’s note: we’ll allow it] ; (

May was a month in which severe El Niño weather had a strong impact, perhaps its greatest this year. Fishing GDP, the figure for which has already been released, was down 71% y/y in May. This alone should shave 0.4 percentage points off aggregate GDP growth directly, and another 0.6 percentage points indirectly (through fishmeal processing), for a total of nearly one percentage point.

Agriculture GDP growth has also officially been reported this week to be -8.3% y/y. This represents half a percentage point of lower aggregate GDP point growth.

Thus, through these two sectors, fishing and agriculture, weather can be said to have accounted for 1.5 percentage points of lower growth in May.

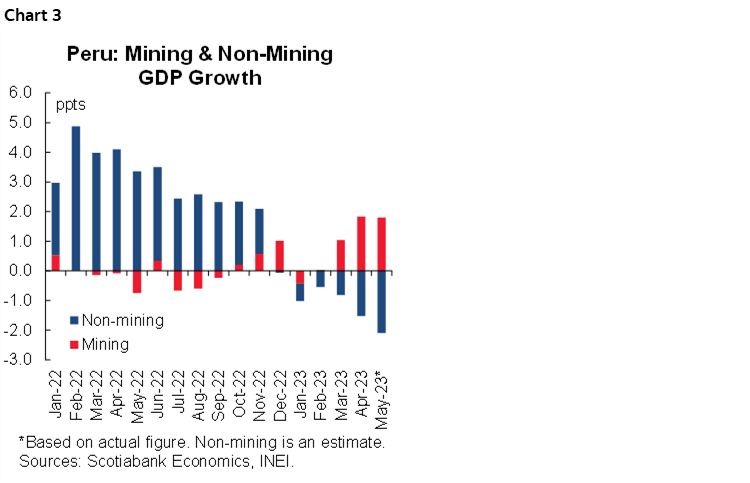

Thankfully, mining is unaffected by severe weather and is outperforming expectations. Mining GDP has been up a strong 21% y/y in May (chart 3). This represents a 1.8 percentage point addition to aggregate GDP growth. At face value, mining would fully compensate for severe weather and then some. The problem is that strong mining growth throughout 2023 has been expected from the start and is factored into our forecasts, whereas the impact of severe weather has surpassed expectations by a good margin.

Aside from natural resource sectors affected by severe weather, the other reason behind the risk that we see negative GDP growth in May is extremely cold domestic demand. This is something that we had already pointed out in April, when GDP growth was a low 0.3% y/y. We expect May figures to reaffirm this impression of dormant demand. In particular, construction growth is likely to be negative yet again, as well as industrial manufacturing. Both, but especially the latter, are linked to domestic demand.

The moral of the story is that weather is wreaking havoc on an economy already beset by weak demand.

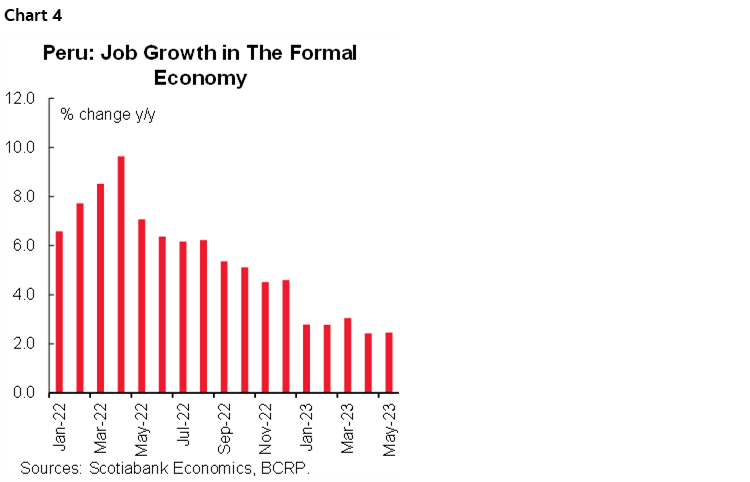

One mild potential plus going forward is that the job market has been holding up even in these chilly times (chart 4). Formal employment rose 2.5% y/y in May. Formal employment in the private sector did even better, up 4.2% y/y. Private sector jobs growth took place mainly in retail, the broad services sector, agriculture and mining. Meanwhile, jobs were lost in construction and fishing. Jobs growth has been positive now for well over two years. So, one may wonder why is domestic demand struggling? The problem lies in worker income, which has not risen in line with inflation. Total salaries (jobs times salary increase) in the formal sector rose 5.9% y/y. Given 4.2% jobs growth, this would mean under 2% nominal salary increase y/y, well below yearly inflation, which was 7.9% in May.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.