- Colombia: Headline inflation surprises to the downside for the third month in a row; core inflation reluctant to decrease, however

European hours are seeing rates markets firmly bid with no obvious catalyst. This comes after a range-bound overnight session where the mood was supported by reports in Chinese media that more stimulus measures are coming. US equity futures are little changed, US , UK, and German curves are bull flattening, and commodity prices are rallying on Chinese developments, with iron ore up 2%, and copper and oil +0.3%. CNY and JPY appreciation from their late-June weakness continued overnight and is acting as a headwind for the broad USD that is weaker against nearly all majors today (MXN unch). The day ahead is quiet ahead of US CPI and the BoC’s decision tomorrow; overnight, the RBNZ is universally expected to leave its policy rate on hold at 5.50%.

On the heels of Colombia’s inflation figures released yesterday (see below) and ahead of the US’s CPI data tomorrow, Brazil’s IBGE publishes June prices data today at 8ET. The median economist projects another steep deceleration in y/y headline inflation to 3.1%—in what would be its lowest level since Aug/Sep 2020—from 3.9% with a decline of 0.1% seen on the month.

Today’s reading could be the last notable drop and/or mark the start of a plateau, ahead of a modest reacceleration in prices growth in the second half of the year. Base effects become much less favourable in H2, and month-on-month IPCA-15 prices growth that was averaging 0.0% in the six months to December 2022 has averaged 0.5% in the first half of 2023. Still, it is practically a given that the BCB will reduce rates at next month’s decision and the market is already pricing in about 40bps, so today’s print and the IPCA-15 release on the 25th will be the main determinants of whether the bank does a 25 or 50bps cut.

Chile’s central bank publishes the results to its economists survey at 8.30ET, which will likely show a similar result to yesterday’s traders survey that had the median expecting a 75bps rate cut from the BCCh at its decision on the 28th. The median respondent also saw an 8% BCCh rate at year-end (from 8.25% previously). This is 50bps above our Santiago team’s latest projection of 7.50%, but 50bps below the 8.50% in the June economists survey that will likely come in lower in today’s publication.

—Juan Manuel Herrera

COLOMBIA: HEADLINE INFLATION SURPRISES TO THE DOWNSIDE FOR THE THIRD MONTH IN A ROW; CORE INFLATION RELUCTANT TO DECREASE, HOWEVER

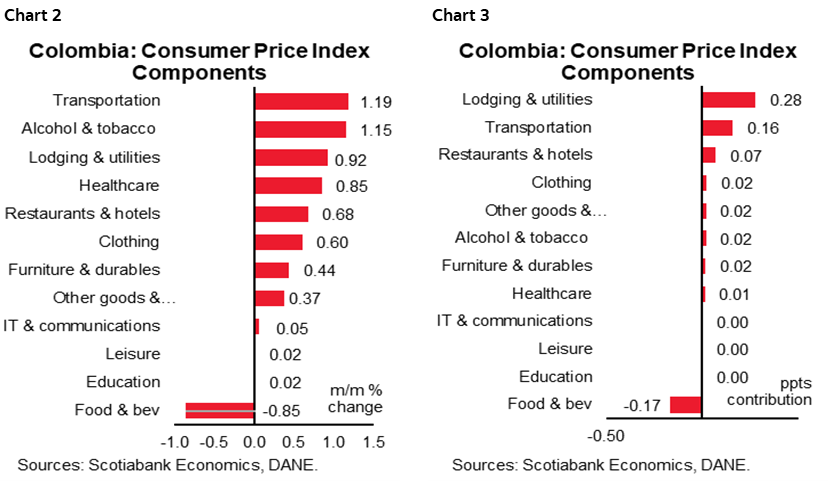

Colombia’s pace of monthly CPI inflation was 0.30% m/m in June, according to DANE data released on Monday, July 10th. The result was again below expectations of the BanRep survey (median 0.39% m/m) and below Scotiabank Economics’ projection of 0.51% m/m. In June, Housing & Utilities and Transport groups contributed the most to the upside; meanwhile, foodstuff inflation partially offset posting a new monthly contraction (-0.53% m/m); it is relevant to note that despite the current dynamic, food prices are encouraging for inflation in the short term, it will play against it next year due to lower statistical effect, which in the end could motivate more moderate downside revision to inflation expectations.

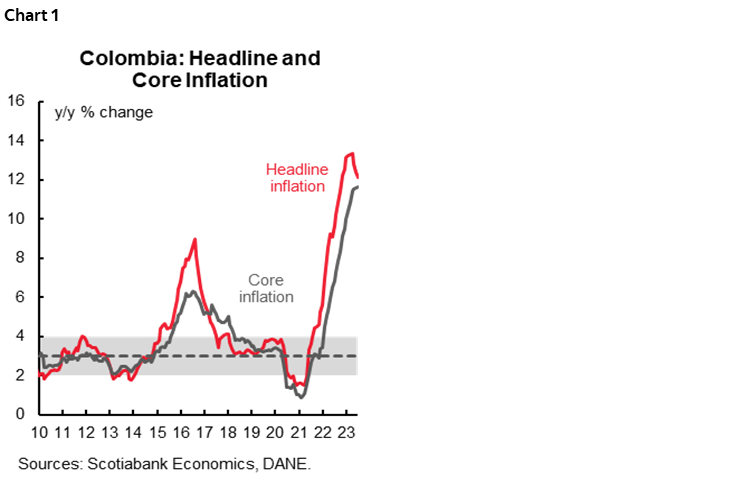

Year-on-year headline inflation decreased for the third month, from 12.36 % in May to 12.13% in June (chart 1), the lowest since October 2022. However, it is relevant to note that the inflation correction is losing steam compared with what was observed in the previous two months. In our opinion, inflation will continue slowing down in the forthcoming months but at a more moderate pace. On the other side, core inflation proved to be more reluctant to decrease; ex-food inflation stood at 11.62% y/y, increasing from the previous month’s figure of 11.59% y/y, while ex-food and regulated inflation was 10.51% y/y, also rising from the last register to 10.47% y/y. Despite the downward headline surprise, inflation remains well above BanRep’s target (3%), while core metrics remain hovering at high levels. The previous dynamic affirms our expectation that BanRep won’t consider rate cuts before the last quarter of 2023. Our official call is to start rate cuts in October; however, if inflation, and especially core inflation, hasn’t decreased further by this time, the central bank could delay the discussion for an easing cycle.

Looking at the balance of risks, food inflation is expected to continue contributing to the headline inflation decrease; however, gasoline price increases and the risk of an El Niño weather phenomenon are headwinds and will continue preventing the central bank from talking about rate cuts in the near future. Only if core inflation starts to look down significantly can BanRep think of starting an early easing cycle. Although we do not see that happening soon due to still indexations effects, especially in rental fees, we cannot discard that economic activity surprised to the downside making inflation inertia disappear. Looking at June’s numbers in detail, food inflation was the only group that showed monthly contractions (charts 2 and 3).

The highlights are:

- The lodging and utility group was the main contributor to the upside to monthly inflation; however, this time, it was to a lesser extent. The group posted a +1.08% m/m and +15 bps contribution, which is lower than the previous month’s contribution of 28bps. Rent fees continued increasing, however, at a slower pace than last month (+61% m/m in June vs. 0.92% m/m average in the previous three months), showing that indexation effects are moderating their impact as the year passes, although are still present. Utility fees were broadly unchanged (0.08% m/m), thanks to a new reduction on gas fees (-1.78% m/m), which in turn reflects the lower exchange rate effect. We also noted that inflation of other utilities such as water (+0.31% m/m) and electricity (+0.50% m/m) are posting more moderate increases.

- The second most significant contributor to headline inflation was the transportation group, showing a 1.06% m/m figure and a contribution of 0.14 ppts to overall inflation. Gasoline prices (+4.60% m/m), contributed 13 bps in the monthly inflation due to the 600 pesos increase; we expect the government to continue increasing gasoline prices at a 600 pesos pace until the end of the year, however, by this time, the big question is if the government will decide to increase diesel prices, which is a material risk to the upside due to the potential secondary effects on other key items in the CPI basket.

- Transportation group is also showing an interesting dynamic derived from the FX appreciation and weaker demand: vehicle inflation was 0.16% m/m, the slowest rate of increase since mid-2021. We also observed this effect in other tradable goods, especially durables, that are posting negative inflation.

- On the other side, foodstuff inflation posted a new significant contraction (-0.53% m/m). In June, 26 food items out of the 59 references in the basket reported a m/m reduction, increasing from the 21 out of 59 registered in May. The negative contributions came from plantains (-6.15% m/m), potatoes (-5.39% m/m), and vegetables and legumes (-3.44% m/m). On the upside, chicken (+1.24% m/m), tomatoes (+11.21%m/m), and oranges (+12.86% m/m) offset the downward trend. Food inflation could continue decreasing in the forthcoming months, however, at a slower pace.

- Inflation by main groups: out of the 189 CPI items, 45 posted negative m/m inflation (~24% of the total basket). Goods inflation increased from 14.05% m/m to 14.26% m/m, signaling that upside pressures from gasoline prices are finding difficulties in being offset and other items. Services inflation decreased timidly to 9.04% y/y vs. the previous 9.06% y/y in May, reflecting still indexation effects observed in some labour intensive items.

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.