- Colombia: S&P affirms Colombia’s rating thanks to pragmatic and predictable economic policies that are expected to continue

The overnight trading mood was shaped by PMI data in Europe that showed an improvement in the Eurozone’s economic backdrop (which nevertheless remains frail) while UK growth problems deepen. The USD is broadly stronger with the exception of the JPY that is clawing back some of yesterday’s losses, while crude oil records a slight 0.3% gain in contrast to a comparable decline in US equity futures—in spite of lower global yields, led by the UK. Copper and iron ore prices are practically unchanged on the day,

Mexican H1-Jan CPI data released this morning beat economists’ forecasts with a notable pick-up in core prices on a bi-weekly basis that should keep Banxico in a hiking mood. Compared to H2-Dec, core prices rose 0.44% against the median submission of 0.32% (and no economist above 0.40%, from 0.19%) while the overall basket saw a 0.46% gain (vs 0.39% consensus, from 0.10%). In year-ago terms, inflation in Mexico has also accelerated over the past three bi-weekly releases (today at 7.94% from 7.86%) and core inflation is showing no signs of letting up as it remains around 8.3-8.5% since H1-Sep (today at 8.45% from 8.34%).

We don’t think today’s print will pull Banxico away from a 25bps hike at its upcoming policy announcement on February 9 (to instead chose a half-point hike), but persistently high core inflation does keep additional hikes on the table towards our forecast of an 11% terminal rate. The MXN barely reacted to the print, and is holding on to a 0.2% decline on the day in line with the dollar tone, as markets remain somewhat skeptical that Banxico has much more left in the chamber.

—Juan Manuel Herrera

COLOMBIA: S&P AFFIRMS COLOMBIA’S RATING THANKS TO PRAGMATIC AND PREDICTABLE ECONOMIC POLICIES THAT ARE EXPECTED TO CONTINUE

S&P affirmed Colombia’s credit rating at BB+ and its outlook as “Stable”. S&P expects continuity in fiscal and monetary pro-growth policies, compatible with fiscal consolidation and the stabilization of the country’s debt ratio at under 60% of GDP.

Macro picture:

- S&P highlighted that Colombia had maintained stable democratic and political institutions. The ratings agency also stressed that the inflation targeting regime and flexible exchange rate are key buffers against external shocks.

- On the negative side, S&P said Colombia has low fiscal flexibility. In fact, it highlighted that despite the approval of the fiscal reform, the government would face a shortfall in revenues in 2024 due to lower growth and commodity prices.

- The current account deficit is also an issue in Colombia’s investment position. S&P said Colombia had limited success in expanding non-traditional exports. S&P forecast net external debt to represent 140% of current account receipts in the medium term.

- S&P highlighted growth resilience; they expect Colombia to grow 8% in 2022 and 1% in 2023. They said that higher than expected growth, coupled with a more diverse external sector and a contained growth of the general government debt, could conduct a rating upgrade in a 12–24 month horizon.

Our take:

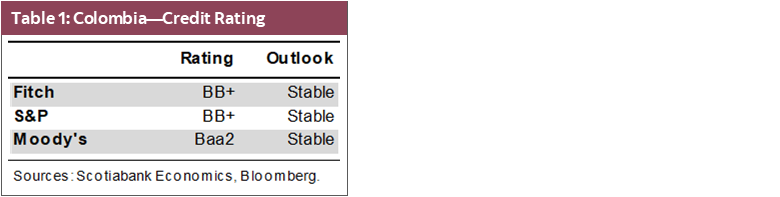

S&P’s assessment of Colombia's economy coincides with Fitch’s announcement in December (table 1). Both agencies highlighted that strong political and economic institutions grant continuity in pro-growth policies and fiscal responsibility. That said, Colombia’s weak points remain the external deficit and debt burden. We don’t expect a ratings or outlook change soon; that said, Colombian assets will continue to reflect a premium due to the country’s non-investment grade status.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.