- Colombia: Weaker than expected growth; BanRep survey sees final 25bps

- Peru: Social unrest impacted economic activity in December

Markets traded with a risk-neutral feel overnight on limited developments, and little follow-through to the solid close in US markets yesterday during Asian and European hours. The highlight for global markets will be the flood of US data at 8.30ET, with a focus on producer prices data as markets look to narrow their expectations for the Fed’s terminal rate. Crude oil was doing well in Asia trading before choppy price action hours to now trade only 0.3% higher, copper is up 1.2% but this is all within recent ranges and likewise for iron ore (+1%).

The clearest trend overnight was the broad weakness in the USD as lower Treasury yields (10s down 2bps, 5s down 5bps) weigh, but gains are relatively minor, limited to +0.2% at the top of the majors (JPY). The MXN is practically unchanged after trading in a very narrow range, while we await the Colombian open for a possible snap higher in the battered COP from a six-week low, after shedding 2.6% yesterday with the USD-positive tone accentuated by disappointing GDP data (see below). The CLP is up 0.8% in early dealing, correcting practically all of its decline during Wednesday’s session.

With a bare calendar in the region, our focus in Latam will be the ongoing debate in Peru’s congress on an earlier election date. President Boluarte is reportedly meeting with party leaders in an attempt to break the deadlock with only today and tomorrow to go to settle on when the vote will take place. Meanwhile, in Colombia, Petro’s plans for health care and pension reforms were met by thousands of protestors yesterday. Colombia’s finance minister (and BanRep’s) Ocampo also highlighted via official text communications that the reforms must meet the fiscal rule.

—Juan Manuel Herrera

COLOMBIA: WEAKER THAN EXPECTED GROWTH; BANREP SURVEY SEES FINAL 25BPS

GDP growth was weaker than expected and it could tilt BanRep to the dovish side

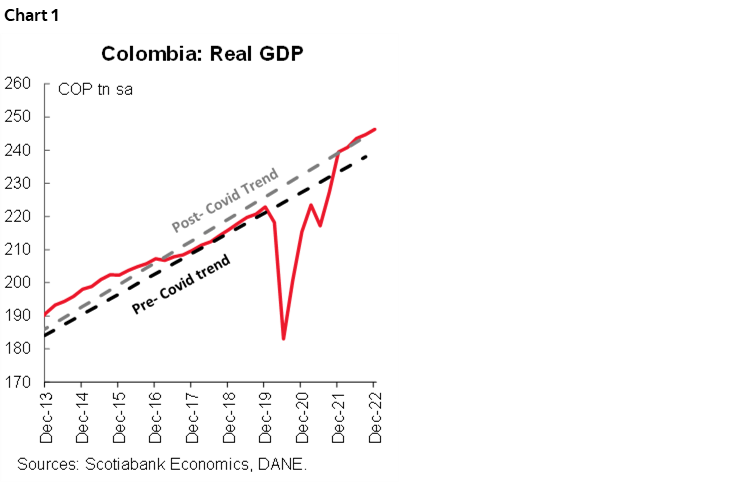

Data released on Wednesday by Colombia’s DANE show that Colombia’s real GDP grew 2.9% y/y in Q4-2022, below both the consensus’ (3.8% y/y according to Bloomberg) and our forecast of 4.0% y/y. Growth was +0.7% q/q on a seasonally adjusted basis (chart 1), with positive contributions from services-related sectors. For the year as a whole, the DANE said that the economy grew 7.5%.

Although economic activity was strong last year, the data show that private consumption has weakened at a faster pace than expected. Additionally, the stats agency significantly revised the path of 2022 GDP downwards, which implies that the speed of growth and overheated consumption is lower than initially published. The new 2022 data on economic activity will lower the positive output gap making more difficult for the hawkish side of the BanRep’s board to keep its tone. For now, we maintain our forecast of a final 25bps hike in March but now the bias is tilted towards an end of the hiking cycle at 12.75%.

Full year 2022 growth results reflect the resilience of the economy post-COVID-19, especially those sectors related to services, given that it was a year with a calendar full of mass events and the return of various typical festivities.

On the demand side, private consumption moderated to grow 4.3% y/y in Q4 and contracted -0.2% vs. the previous quarter. Investment had a timid impulse to the inter quarterly dynamics of +0.2%, especially in housing investment since construction is picking up steam reflecting solid house sales in recent months.

Looking ahead to 2023, activity is expected to decelerate significantly to more sustainable levels explained by a continued slowdown in private consumption, as investment picks up. On the supply side, a mixed performance is expected, with leisure activities continuing to moderate and commerce activities becoming less dynamic, while agriculture could still face challenges amid climatic abnormalities. Construction is expected to contribute to value added, especially civil works ahead of regional elections. Therefore, we estimate growth of 1.5% in 2023 with a downward bias given in light of higher rates and inflation that is likely to remain higher for longer.

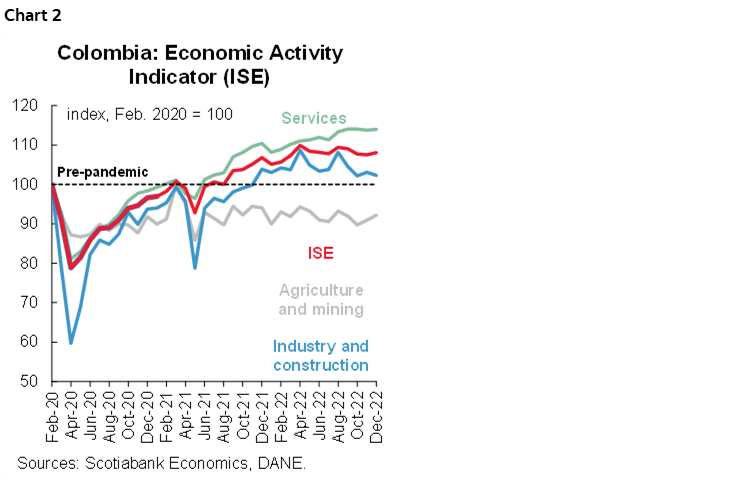

According to the monthly indicator (ISE, chart 2), economic activity showed a still positive but less strong expansion of 1.3% y/y in December (0.6% m/m, sa). The highest y/y gains came from leisure (25.2% y/y), financial and insurance (10.5%) information and communications (+7.2% y/y), professional activities (2.9% y/y) while on the negative side we have commerce (-1.0% y/y), manufacturing (0.2% y/y), construction (-5.0% y/y) and agriculture (-3.7% y/y). In seasonally adjusted monthly terms, the negative balance was driven by leisure activities (-2.0% m/m sa), commerce (-1.1% m/m sa), construction (-3.1% m/m sa) and agriculture (-0.2% m/m sa).

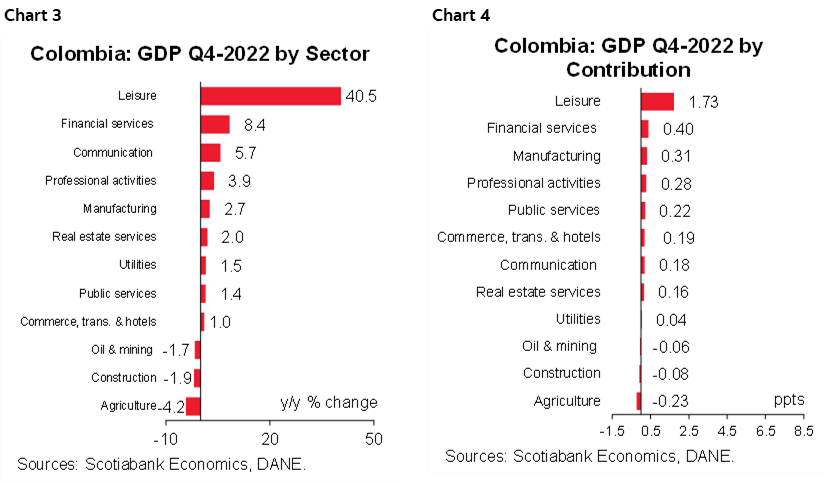

Regarding the GDP Q4-2022 performance from the supply side we highlight:

- The sectors that contributed the most in the fourth quarter were leisure-related activities (+1.3ppts), financial and insurance activities (+0.4ppts) and manufacturing (+0.3ppts), accounting for about 70% of the growth.

- The balance of sectors was mixed (charts 3 and 4), since services-related sectors continued outpacing the performance of goods production-related sectors. The largest expansions came from leisure (40.5% y/y), financial and insurance activities (+8.4% y/y), communication (5.7% y/y) professional activities (+3.9% y/y), commerce (1.0% y/y) and manufacturing (+2.0% y/y). The weakest performance during the quarter came from agriculture (-4.2% y/y), mining (-1.7% y/y) and construction (-1.9% y/y) explained by climatic effects on agricultural crops and, on the construction side, infrastructure projects are dragging to the performance in the sector.

- It is worth mentioning that in the case of commerce there was a y/y revision, especially in Q3, which was revised upwards from 8.1% y/y to 11.4% y/y, which according to the DANE is explained by the incorporation of a new survey that incorporates information from micro enterprises.

- The consolidation of normality and which allows more massive events are reflected in the positive dynamism of the service-related sectors. On a seasonally adjusted basis, leisure activity showed a strong rebound (+7.5% q/q sa), however, on the downside, the agricultural sector (-1.3 q/q sa) was strongly affected by the strong rainy season and high inputs’ prices. Commerce also had a negative balance (-1.5 q/q sa) explained by lower household demand given the strong inflationary pressures.

- The construction sector showed weaker balance in its dynamics in quarter-on-quarter terms of -2.5%, which may be explained by higher cost pressures, increases in interest rates and uncertainty about the continuation of some of the housing subsidies, added to the fact that the civil works component has not performed as dynamically so far this year.

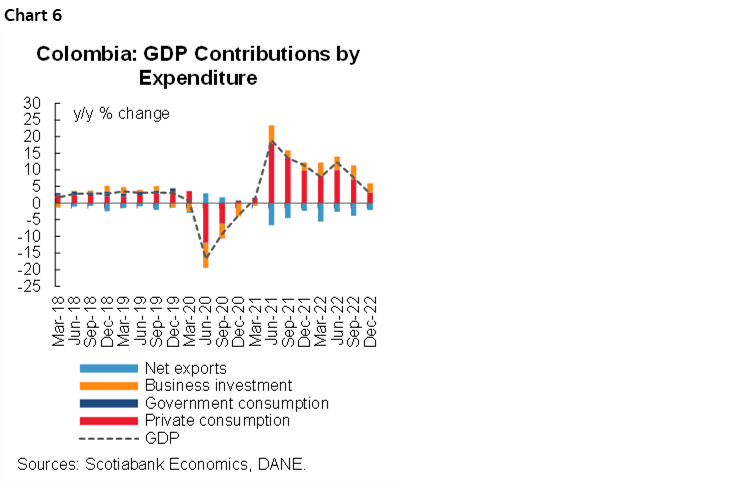

Expenditure side GDP Q4-2022:

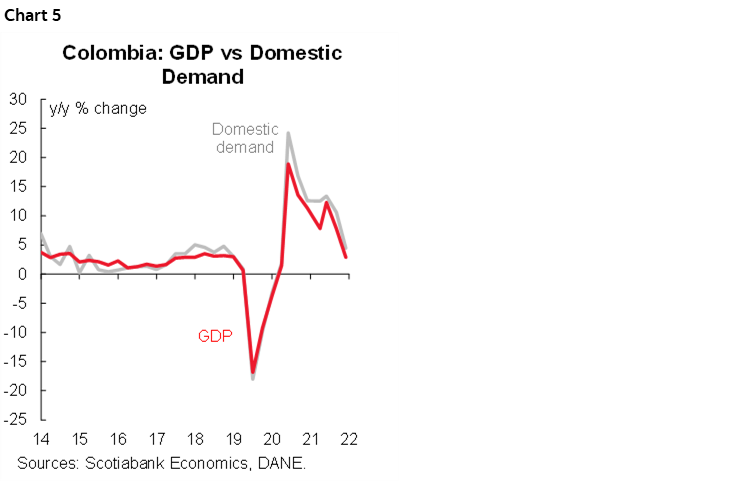

Domestic demand increased by 4.5% y/y in Q4-2022 (chart 5), representing the slowest expansion of the year, which helped to reduce a touch the real external deficit. Sequentially, domestic demand contracted by -1.6% q/q sa. Moreover, it is worth noting that the data for Q1 and Q2 were revised downwards, while that for Q3 were revised upwards from 9.8% to 10.6% y/y, for full year growth of 10%. In relation to investment, although it did not show a contraction, its quarter-on-quarter expansion was muted (+2.0%), although in year-on-year terms in the last quarter it increased 10.3% y/y.

- Private consumption (+2.2% y/y) continued to contribute positively to growth, although at a slower pace of +3.2ppts (chart 6). In seasonally adjusted quarterly terms, private consumption registered a contraction of -0.2% q/q sa that can be explained by inflationary pressures and more expensive credit. The biggest drop came from public consumption (-5.1% y/y) and presented a q/q variation of -5.1%, showing much lower execution of government resources given the beginning of the transition of the new government. It is worth noting that total consumption, which aggregates household and government consumption, was revised downwards in the first half of the year, while in Q3 it was higher than previously published passing from 6.7% to 8.3% y/y growth.

- Investment expanded 10.3% y/y and contributed 2.0ppts to total growth and, although the inter quarterly expansion was weaker than in Q3 (2.0% q/q vs 5.6%), it still shows a recovery path from 2021. Having said that, investment has been affected by reduced dynamism in housing and other buildings construction. And to a less strong momentum in civil works. In the full 2022 it grew 11.8%. We expect that in 2023 it will gain some momentum and contribute to growth despite some headwinds for the sector which remain in high input costs and high rates.

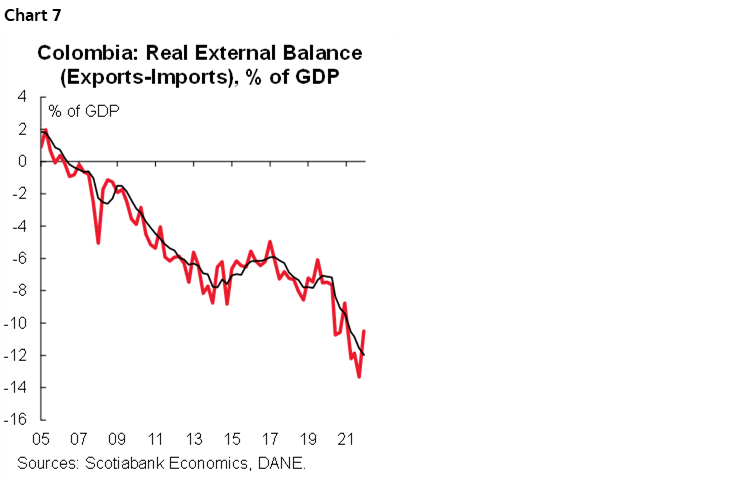

- The real external deficit in Q4-2022 accounted for 10.3% of GDP (chart 7). Exports (+1.9% y/y) grew at a slower pace than imports (+10.0% y/y), showing the impact of lower primary activities given lower production despite high external prices, while imports were less dynamic which could contribute to a less negative external deficit.

All in all, Q4-2022 GDP came in below expectations. From a sectoral perspective, the balance was mixed, with services still leading growth alongside a still strong manufacturing sector. However, agriculture and mining lagged. On the demand side, the slowing was mainly explained by private consumption and a moderate dynamism of investment, especially in the construction sector.

Softer than expected economic activity in 2022 and stickier inflationary pressures for this year, combined with inflation expectations that remain well above the central bank’s target, constitute a challenging scenario for BanRep. However, weaker economic data can tilt BanRep to the dovish side. For now, our expectation is that at the March 31 meeting BanRep will raise its policy rate by 25bps to 13% and keep it there for an extended period of time.

Economist consensus suggests that inflation peaked in January with final 25bps BanRep hike expected

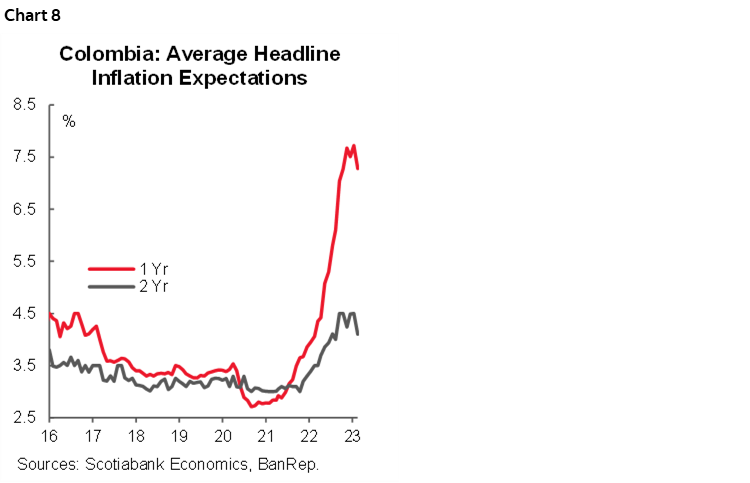

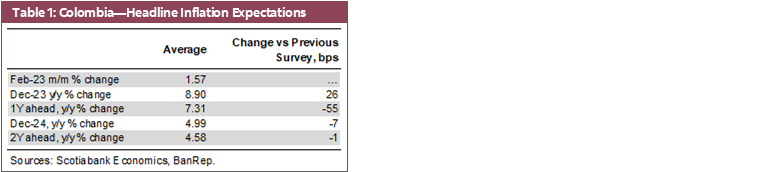

On Tuesday, February 14, BanRep released its monthly survey of economic expectations. Inflation expectations (IE) for the end of 2023 increased by 0.26ppts, as analysts incorporate January’s upside surprise. Now, expectations for Dec-2023 are at 8.90% y/y. However, the good news is that finally inflation expectations one- and two-years-ahead moderated (chart 8). For end-2024, expectations stand at 4.99% y/y, still above the central bank target, but 0.07ppts below the previous survey.

Monthly inflation for February is expected at 1.57% m/m, which is lower than the monthly inflation observed in February of 2022 (1.63% m/m), which would result in annual headline inflation to fall by 0.06ppts. At Scotiabank Economics, we expect 1.78% m/m; by year-end, we project 9.23%, followed by 4.92% at end-2024—lower than out previous call of 5.03%.

In accordance with inflation expectations, the market consensus expects a final 25bps hike in the monetary policy rate to 13% as the terminal rate. Scotiabank Economics Colombia is aligned with the expectation, and we additionally expect a rate-stability period until inflation returns to single digits (October, in our estimation). By the end of the year, market consensus sits at 11% compared to our call of 12%.

- Short-term inflation expectations. For February, the consensus is 1.57% m/m, which places annual inflation at 13.19% year-on-year (from 13.25% in January); it would at least point to a stabilization of headline inflation, interrupting the consecutive increases seen since April 2021. The response dispersion in the survey remains high, with the lowest at 0.78% m/m and the highest at 2.10% m/m. Scotiabank Economics expects monthly inflation for February to be +1.78% m/m and 13.41% y/y. In February, education fees will lead prices increases, but indexation effects and still high food inflation will also contribute to higher prices.

- Medium-term inflation expectations showed a mixed, but constructive, picture. Inflation expectations rose to 8.90% y/y for December 2023, 0.026ppts above last month’s survey (table 1), showing the inertia that indexation effects are generating in inflation. However, the positive news is IE for one-year ahead stood at 7.31% y/y (below last month’s reading of 7.86% y/y); while the 2-year outlook fell by 1bps to 4.58% y/y. The relative stability of long run inflation expectations would contribute to the BanRep’s board to slow down further the hiking cycle.

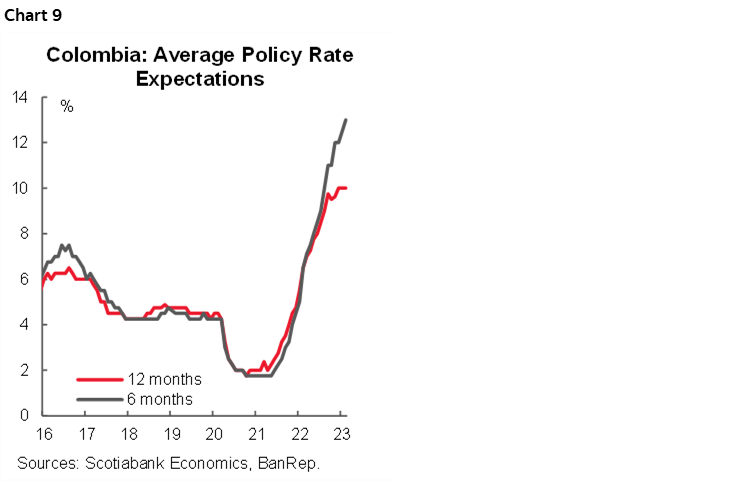

- Policy rate. The median of the expectations (chart 9) points to a 25bps rate hike at the March 31st meeting to leave the rate at 13% (from the current 12.75%); Scotiabank Economics shares the same view. For now, it is expected to be the last move of the central bank before starting a pause which, according to the market consensus, would last until September, when the start of gradual cuts is anticipated, to reach 11% by the end of 2023.

- FX. USDCOP projections for the end of 2023 average 4,717. By December 2024, respondents think, on average, that the peso will sit at USDCOP4,584 pesos. USDCOP for the end of February is expected around 4,757 pesos.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

PERU: SOCIAL UNREST IMPACTED ECONOMIC ACTIVITY IN DECEMBER

Peru’s GDP posted its lowest monthly expansion rate in 2022 (0.9% y/y) in December, below the 1.2% expected by the market consensus, with growth impacted by the start of social protests after the vacancy of ex-president Pedro Castillo and the inauguration of President Dina Boluarte. The INEI revised data from previous months higher, resulting in a 1.7% expansion in GDP in Q4-22 and 2.7% during the year 2022, close to our forecast (2.6%).

For January, we anticipate that the social unrest will have had a greater impact than in December, not only because of their radicalization but also because the road blockades extended from the southern region to other parts of the country, and therefore we estimate that GDP did not grow (0%). The most affected sectors were likely hotels and restaurants, transportation, construction and financial services.

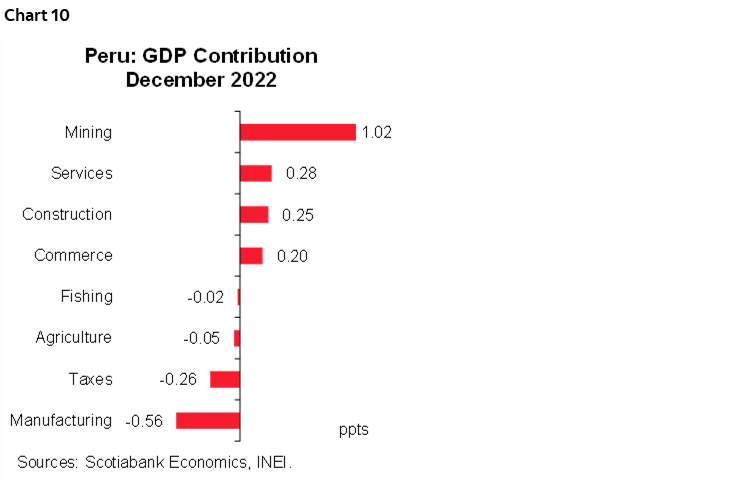

The positive GDP evolution in December was supported by the growth of the mining and hydrocarbons sector (+9.3%), which contributed 1ppt to the result of the month (chart 10). In particular, higher copper output (+19.2%)—driven by the start of production of the Quellaveco project—and iron (+99.4%)—which benefited from a low comparison base due to a strike of Shoungang in December 2021. Likewise, the expansion of the construction sector (+3.0%) contributed to the dynamism of public investment from regional and local governments—particularly in sanitation works, roads, health, and education infrastructure—in their last month before the change of government at the regional level.

On the other side, the sectors linked to internal demand exhibited a significant slowdown, particularly non-primary manufacturing (-8.1%), which posted its largest monthly drop since August 2020. This behavior was partly explained by the social unrest that affected the normal operation of agro-export industries in Ica, the dairy industry in Arequipa, and the beverage industries in the southern region, among others. Likewise, lower external demand was observed in the case of the textile and clothing industry.

—Pablo Nano

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.