- Chile: 2022 GDP would have ended with an expansion of 2.7%, in line with our projection

- Colombia: Exports are losing momentum, while employment stagnated

CHILE: 2022 GDP WOULD HAVE ENDED WITH AN EXPANSION OF 2.7%, IN LINE WITH OUR PROJECTION

Remarkable resilience of economic activity in services and trade. We maintain our projection of a 1.7% drop in GDP in 2023.

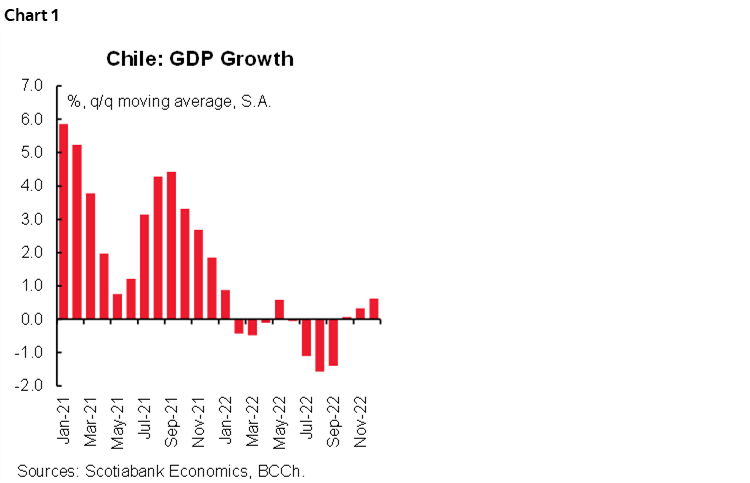

The central bank (BCCh) released today GDP for December (Imacec) which contracted 1% y/y, positively surprising our expectations and those of the consensus. In seasonally adjusted terms, the Imacec expanded 0.4% m/m mainly thanks to the good performance of the non-mining sectors (chart 1), which grew 0.5% on average, the first monthly expansion since August 2022.

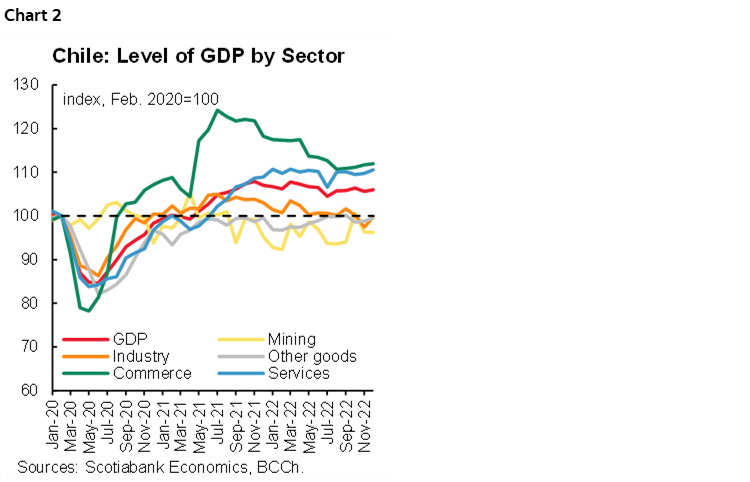

Trade and services continue to show resilience (chart 2). Trade expanded 0.2% m/m, growing for the fourth consecutive month thanks to the rebound in wholesale trade, which in recent months has been driven mainly by the sale of machinery and equipment and construction materials. Similarly, services have grown in the last two months (0.8% m/m in December) thanks to the greater dynamism of transport services, which could be associated with a recovery after the truckers’ protests in November 2022, although also due to a positive performance of business services. Both sectors would be reflecting on the margin the rebound in investment, mainly in the public sector, which showed a significant acceleration in December (86% execution, its highest execution rate since 2019) and was concentrated in housing and public works.

Preliminarily, GDP would have expanded 2.7% in 2022. For the base scenario of the central bank published a few weeks ago, which expected growth of 2.4%, this figure is positively surprising and, consequently, could explain the resistance of the monetary authority to cut the reference rate. A very negative view of the slowdown in activity in the second half of 2022 by the central bank could also be behind the insistence on keeping the reference rate at highly contractionary levels. At Scotiabank, we see that the slowdown process will be more noticeable during the first half of 2023.

Market reaction: pending the message from the Federal Reserve that it can change or ratify the course of the dollar and the rates, these activity figures fuel the appreciation of the Chilean peso and put downward pressure on expected inflation through the exchange rate channel. The battle of (higher) domestic inflation versus (lower) imported inflation will begin to intensify locally.

—Aníbal Alarcón

COLOMBIA: EXPORTS ARE LOSING MOMENTUM, WHILE EMPLOYMENT STAGNATED

Exports in 2022 expanded by 38% y/y; however, in December, they registered the first contraction in 22 months

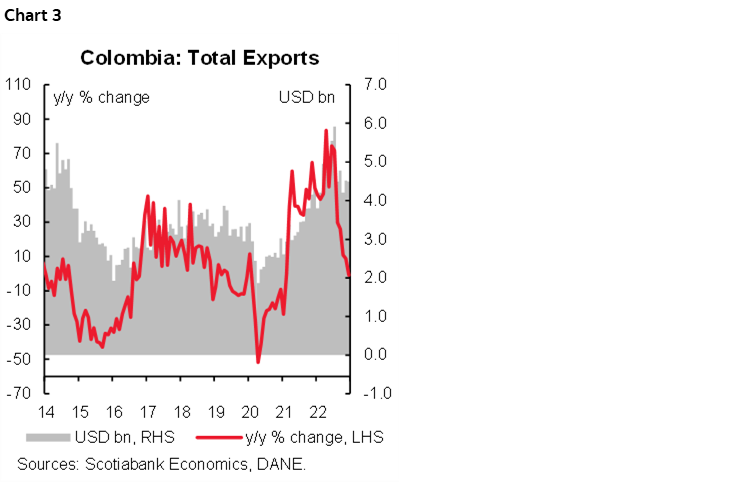

DANE released exports data on Tuesday, January 31; monthly exports for December stood at USD4.50bn, a contraction of -1% y/y (chart 3), below the previous month’s figure of USD4.52bn, and interrupting 22 months in a row of annual expansions. Traditional exports (related to mining and coffee) are dragging the overall export figure. Meanwhile, non-traditional exports continued hovering around historically high levels (~USD1.78bn).

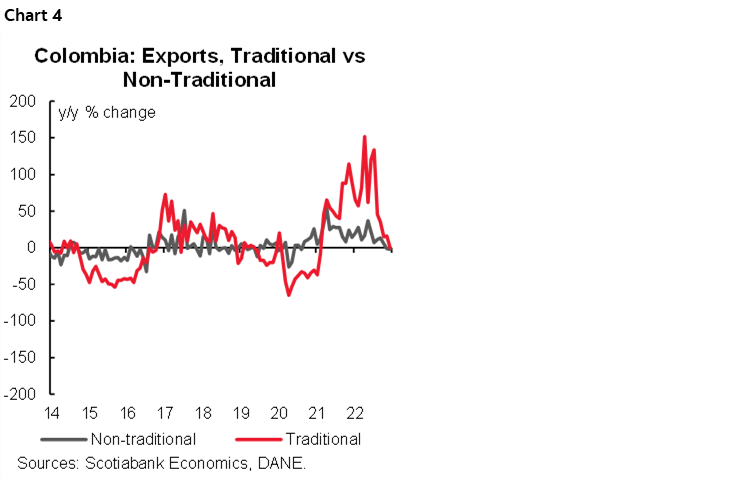

- Traditional exports contracted by -2.1% y/y in December (chart 4), posting the second annual contraction in a row. It is worth noting that commodity prices in December 2022 were not substantially superior to those observed in December 2021, which makes the overall export picture less favourable. On the other side, exported volumes of oil and coal weigh against them.

By components, coffee exports contracted by 7.28%, explained by a more moderate domestic production but also due to weaker international prices. Oil fell by 15.75% y/y, amid a 15.71% contraction in volumes, while ferronickel sales showed a contraction of 1.50% y/y, showing mostly a negative effect from international prices. In this month, coal export rebounded by 27.04% due to a price effect; on the other side, we have a concerning picture in terms of exported volumes with a 16.6% y/y contraction that would obey the difficulties in some producer regions which are facing production disruptions due to the atypical rainy season.

- Non-traditional exports contracted by 0.3% y/y (chart 4 again), the first contraction since February of 2021; however they remained hovering around historical record highs (~USD2.72bn). Manufacturing exports contracted by 2.2% y/y as a result of weaker activity in chemical products ( -12.8% y/y), a negative behaviour that was partially offset by the rebound of sales of some agricultural products such as bananas (+55.5% y/y) and sugar (+42.0% y/y).

All in all, exports concluded 2022 with a 38.0% expansion but pointing out that the positive trend is reaching a ceiling. Traditional exports will no longer face a positive shock from international prices, while in the case of non-traditional exports, further increases are challenging to build. The previous is aligned with an expectation of a wider current account deficit in 2022. Currently, the central bank projects a 6.3% of GDP deficit. Ahead of 2023, we don’t expect a substantial reduction on the export side, and in that case, the current account deficit is expected to be driven mainly by a decline in imports, reflecting the scenario of weaker economic activity.

The labour market in Colombia is pointing to a stagnation in job creation while the labour force is increasing

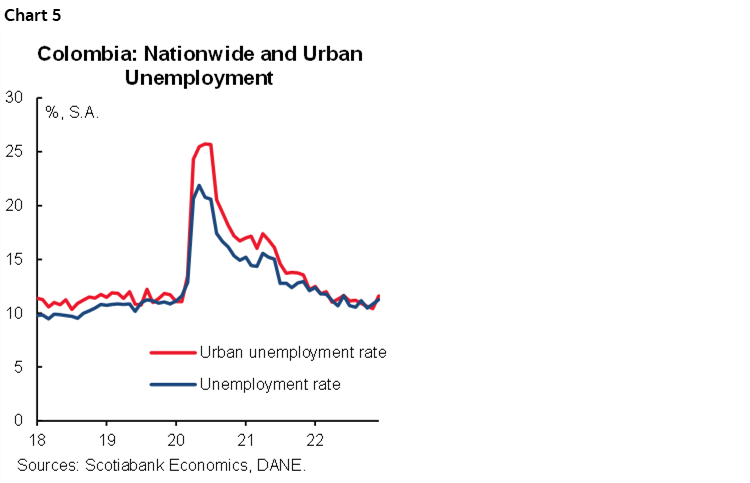

Employment data for December, released on Tuesday, January 31, shows that employment creation stagnates in a context in which people are returning to the labour force. The unemployment rate stood at 10.3% in December of 2022, above our expectation of 9.0%. Urban unemployment stood at 10.8%, above Bloomberg’s consensus of 9.6% and our expected 9.4%. In seasonally adjusted terms, unemployment increased in both references, nationwide it increased from 10.8% sa in November to 11.3% in December, while in urban areas, it increased from 10.4% sa to 11.6% sa (chart 5). All in all, the nationwide unemployment rate in 2022 stood at 11.2%, decreasing from the 2021 figure of 13.8%. On the other side, the labour force increased, and the participation rate was 63.6% on average vs the 61.5% registered in 2021 but still below the 2019 figure of 65.7%.

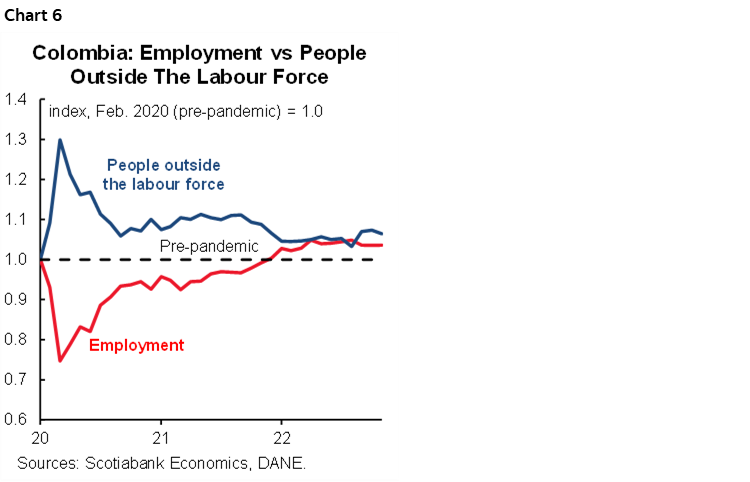

It is worth noting that at the beginning of 2022, Colombia reached pre-pandemic employment levels; however, employment creation had stagnated by the end of the year. In December, employment was just 3.6% above pre-pandemic. On the other side, people are returning to the labour market; in fact, by the end of 2021, people outside of the labour market were 8.8% above pre-pandemic, while by the end of 2022, they were 6.4% above pre-pandemic, which is pointing to a more tight labour market (chart 6).

In y/y terms, jobs increased by 973 thousand in December 2022; three sectors accounted for 67% of job creation: manufacturing (+249 thousand); public administration, health & education (+207 thousand), and leisure-related activities (+195 thousand). On the negative side, commerce (-121 thousand) and agriculture (-92 thousand) showed the most relevant contractions in employment. In the case of agriculture, high input costs and adverse climatic conditions are reducing activity in the sectors. However, the most concerning picture comes from the commerce sector since it could signal a deceleration in economic activity, especially in the services part of the economy, which has been the more dynamic sector in the last two years.

A positive thing to highlight is that gender gaps were reduced during the year. In 2022, the female unemployment rate was 14.3%, lower than 17.5% in 2021. Meanwhile, male unemployment stood at 9.9% in 2022, dropping from 13.5% in 2021. That said, the gap between female and male unemployment narrowed from 6.2 to 5.3ppts. In the case of urban areas, the gain was slightly below since the gap went down from 3.7 to 3.2ppts, and female unemployment stood at 9.9%, decreasing from 13.1%. The previous dynamic is attributed to the fact that in-person activities allowed the female population to return to the labour market and find a job, especially in services-related activities.

In the labour quality front, informality decreased during 2022. By December 2022, nationwide informality reached 57.6%, declining by 1.7ppts compared with December 2021. The informality rate in urban areas stood at 42.8%, while for rural areas, it was 84.2%, still showing an unequal picture.

Summing up, the labour market showed a better performance during 2022, closing employment gaps compared with the pre-pandemic. However, in recent months the employment creation is struggling to match the increase in the labour force, which impedes the unemployment rate from improving.

Despite that, domestic demand during 2022 remained strong, probably showing an effect of a reduction in household savings and the impact of alternative income such as remittances. For 2023, the labour market is expected to be tight as labour force participation is expected to increase further in a context in which the business sector is facing a more challenging environment.

All in all, the unexpected increase in the unemployment rate contributes to signaling the end of BanRep’s hiking cycle. Our call is of a final 25bps hike to 13.0% at the March meeting.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.