- Colombia: Consumer confidence reverses trend and worsens in November

- Mexico: Industrial activity increased due to construction strength in October

The post-Fed UST rally continued in Asia hours to see strong gains at the open in European rates and equities, while dollar losses deepened to have it trade at its lowest level since H1-August. Momentum is the name of the game as the overnight session was relatively bare of global market-moving developments. The SNB held as expected, the Norges Bank surprised most with a hike but with lower rate forecasts, and Australian employment data were mixed.

The ECB and BoE are up next in the G10, both are expected to hold but the ECB may have the tougher task of fighting a rally in rates as its forecasts will show a lower inflation projection (PEPP guidance is a hawkish risk). The US release of retail sales and jobless claims data at 8.30ET is unlikely to hurt confident markets.

USTs, EGBs, and gilts bull steepening. The USD is losing ground against all currencies bar the MXN with a 0.3% loss that may reflect the Fed-Banxico link while the NOK clearly leads, 2% higher, and the JPY follows up 1%. US equity futures are up 0.2/3%, while ESX rise 0.8% and FTSE climbs 1.7%. Crude oil is up ~2%, beat by copper’s 2.5% rise but ahead of iron ore’s 0.5% gain.

The BCB did not materially surprise in yesterday’s decision, going with a well-telegraphed 50bps cut to 11.75% and reiterating guidance that this will be the pace of cuts for the “next meetings”. There was a small risk that the “next meetings” language would be revised to suggest maybe only the next two would see half-point cuts, but leaving it untouched and seeing inflation heading towards target. It seems fairly clear that no bigger cut is being considered, but they are also unsure about what may come sometime in Q2; the BCB is on track for 50bps cuts at the first three meetings of 2024.

We have Banxico and the BCRP’s rate decision in Latam today as the main events, with the BCCh’s traders’ survey and Brazilian retail sales as the morning’s data releases. As for the BCRP, our economists previewed their forecast of a 25bps cut in yesterday’s Latam Daily. Yesterday, BCRP Pres Velarde reportedly said at an event that inflation is under control, and that even core inflation is below that seen in other countries in the region, the US, and Europe; certainly sounds like someone confident that rate cuts should continue.

In the case of Banxico, there’s much more room for surprise. Recall that the previous statement had guidance turn less hawkish on the time that would be spent at peak rates, going to “for some time” from “for an extended period” previously. The minutes showed that there was only one person that seemed more clearly against this change in language, while others, notably Gov Rodriguez, were clearly on board with Q1 cuts. The risk today is that Banxico tee up a bit more clearly that February may see the first cut and not just March. The economy remains strong and that services inflation is still stuck between 5.0 and 5.5% since April, so there may not be enough evidence for them to prepare markets for this move—but in a way economic strength did not stop a dovish tinge to the Fed’s communications yesterday.

—Juan Manuel Herrera

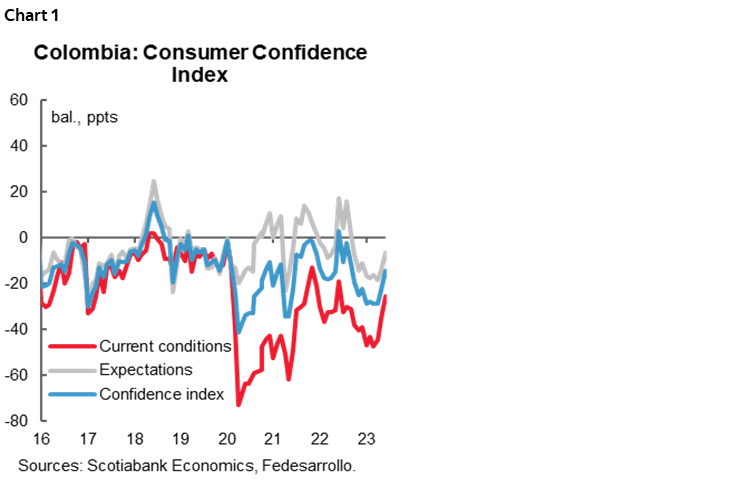

COLOMBIA: CONSUMER CONFIDENCE REVERSES TREND AND WORSENS IN NOVEMBER

The Consumer Confidence Index (CCI) stood at -20.9% in November; a drop of 6.9 percentage points compared to October (-14.0%). The drop is largely explained by a 12.2 percentage point decrease in the Consumer Expectations Index. Meanwhile, the Economic Conditions Index increased by 1.2 percentage points (chart 1). The survey covers the period following the regional elections and reflects a deterioration in the perception of the country’s economic conditions over a 12-month period.

The November data show a change in trend compared to the previous month, since in October the indicator presented a positive performance in its two main components. The Consumer Confidence Index (CCI) registered the lowest level since May (-22.8%), explained by a drop in the Consumer Expectations Index of 12.2 ppts, which dropped to -15.75%. Within this component, it is important to highlight the deterioration of 18.9 ppts in consumers’ expectations about the economic situation of their households in a 12-month time horizon, followed by a drop of 11.3 ppts in the economic expectations of the country in general in a 12-month time horizon. This change in households’ perception could be influenced by the outcome of the regional elections coupled with the Q3-2023 economic growth results, which were published in November showing a contraction of 0.3% YoY.

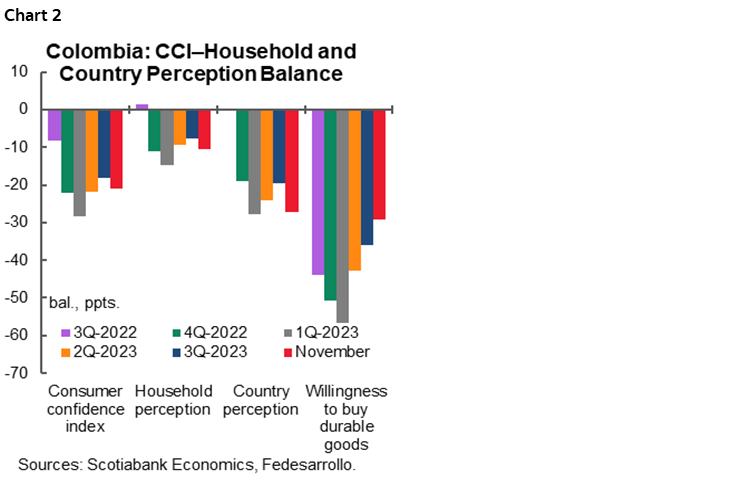

Incentives by commercial establishments, especially the Black Friday event, and the showroom Auto event may have influenced consumers’ willingness to buy durable goods, added to the fact that some consumers have the habit of bringing forward their Christmas shopping. Compared to the previous month, the willingness to buy vehicles increased by 8.3 ppts to -57.3%, the willingness to buy housing increased by 7.3 ppts to -38.5%, and the willingness to buy durable goods increased by 4.7 ppts to -29.1%. This dynamic could continue considering that inflation continued its deceleration path reaching 10.15% YoY in November, showing a better dynamic in goods inflation which decreased to 8.45% YoY from 9.51% in October. The last interest rate decision of the year will be held on December 19th, and although analysts’ expectations are divided, all agree that next year the easing cycle will begin, which will ease the financial burden on households, allowing them to resume a better consumption dynamic.

Looking at the November details:

- The Economic Conditions Index stood at -28.7%, increasing 1.2 percentage points from the previous month. The ECI component showed a deterioration in households’ perception of current economic conditions, while the willingness to buy contributed to the increase in the overall component. The fall in the prices of durable goods, added to events that encouraged consumption in November, contributed to consumers’ increased willingness to buy (chart 2).

- The expectations index stood at -15.7%, a deterioration of 12.2 ppts vs. October. Households’ perception of their current economic situation showed a deterioration of 5.9 ppts vs. the previous month erasing the previous month’s increase. The expectation about economic conditions in a 12-month frontier deteriorated by 18.9 ppts to -35%, this being the lowest level since May 2023. Similarly, the expectation about the country’s economy on a 12-month frontier fell to -19.2%, down 11.3 ppts from the previous month.

- By cities, the Consumer Confidence Index deteriorated the most in Bogota, going from -9.4% in October to -21% in November. Following the negative behavior was Medellin, which recorded a drop of -4.7 ppts to -33.6%, being the city with the lowest ICC. Meanwhile, Barranquilla was the city with the highest increase, going from -24.3% to 16.1%.

- By socioeconomic levels, all presented a drop in the indicator. Confidence in the middle-income group registered a fall of 11.9 ppts to -24.2%, followed by the low-income group which registered a balance of -50.6%, dropping 6.8 ppts, finally the low-income group presented a decrease of 2.2 ppts to -14.6%.

—Jackeline Piraján & Daniela Silva

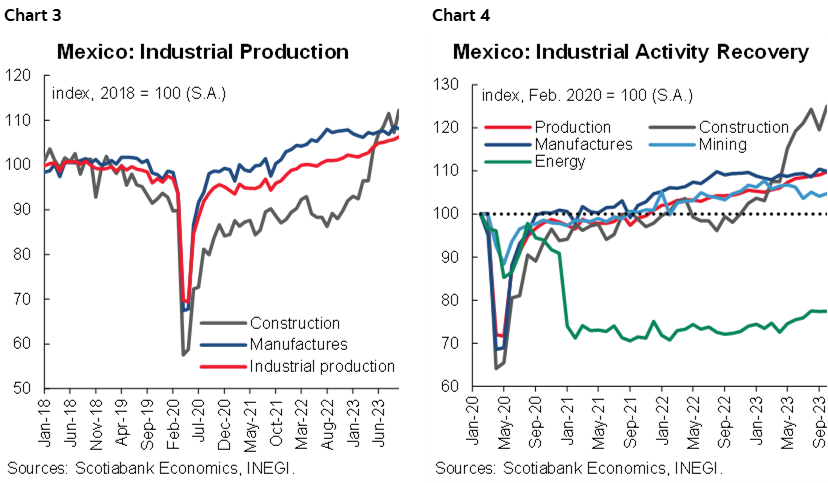

MEXICO: INDUSTRIAL ACTIVITY INCREASED DUE TO CONSTRUCTION STRENGTH IN OCTOBER

In October, industrial activity rose to 5.5% y/y from 4.0% previously (chart 3), construction rose 27.7% (18.8% previously), utilities slowed down to 6.9% (7.0% previously), see chart 4, manufacturing increased 1.1% (0.9% previously) and mining slowed 0.1% (0.5% previously), see chart 4 again. In the monthly comparison, the index increased 0.6% m/m from 0.2% previously, with seasonally adjusted monthly data. Construction showed a significant rebound of 4.7% m/m from -3.8%, and manufacturing dropped -0.4% (1.7% previously). On the other hand, in the cumulative period from January to October there is a real annual increase of 3.9%.

Construction has soared in the last 12 consecutive months, with the largest increase in August 2023, when it rose 30.5% y/y. On a cumulative basis, it has grown 15.1% YTD, and we hope that this component will continue to grow, at a slightly slower pace, supported by civil engineering and to a lesser extent building and specialized work (chart 3 again).

As for manufacturing, these have been registering annual changes of much smaller magnitude if we compare them with construction, since in the cumulative they barely have an increase of 1.5% YTD, due to the lower rate in their components (12 of the 21 are negative), with the deepest falls in textiles, clothing, wood and furniture, among others. Therefore, we expect that manufacturing is set to end the year with slow progress (chart 3 again).

—Miguel Saldaña & Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.