- Peru: BCRP preview: fourth consecutive cut; it’s raining! yay!

Markets traded range-bound through most of the overnight session (and most of the post-Europe US session) on narrow global drivers while we wait for the Fed’s policy decision at 14ET with only US PPI at 8.30ET ahead of it. A larger than expected decline in UK GDP shook up markets and prompted a slight bid to rates. Chinese credit/money supply data released overnight also disappointed but the reaction in markets has been minimal.

USTs and EGBs are bull flattening (US 10s are back to pre-CPI levels) while gilts bull steepen on the data. The USD is stronger again all majors where the NZD is the top loser on kiwi banks revising their views on inflation. Other high-beta FX are mixed in between the majors’ rankings with the MXN off about 0.2% while the ZAR and NOK lag. European bourses are up about 0.3% in line with a 0.2% rise in US equity futures. Crude oil’s slide kept going to sub-$68/bbl in WTI before coming back to unchanged at writing in Brent and WTI. Iron ore and copper are hurting 2.0% and 0.8%, respectively, on a disappointing wishy-washy outcome of the China’s annual economic work conference yesterday.

Today’s main event in Latam will be the BCB’s decision at 16.30ET, where a 50bps cut is widely expected. Ahead of the decision, services volumes data for October are expected to show a slight month-on-month contraction for a third straight negative month that reinforces the half-point pace of cuts by the BCB. November inflation data published yesterday came in very marginally below expectations. Markets believe the central bank will cut by 50bps at each of today’s and the next two meetings with a roughly 60% chance that they do so at another meeting. The risk in today’s decision is that the BCB changes its wording on the 50bps pace being appropriate “in the next meetings”.

—Juan Manuel Herrera

BCRP PREVIEW: FOURTH CONSECUTIVE CUT

We expect the BCRP to continue its interest rate cutting cycle in Thursday’s decision. This would be the fourth consecutive cut of 25bps, taking the reference rate to 6.75%. The first December indicators for inflation suggest that it could drop from 3.6% in November to a range between 3.1% and 3.2%, below our current forecast of 3.6%. This new forecast is in line with what the authorities expected. Food prices have been reversing the supply shocks of previous months, to which is added a lower impact of El Niño, whose temperature metrics have seemingly faded during the latest readings. Likewise, the weakness of the economy would put pressure on a new decrease in core inflation, which would go from 3.1% to 2.9%, with which we see a probable return to the target range after 24 months.

Our forecast remains under a moderate/strong Niño scenario, the dominant probability until now, although we will evaluate a change of weak/moderate scenario if the reduction in the temperature anomalies that we have been observing until now is confirmed. We see a new revision to our forecast for 2024 as likely in coming weeks. The MoF estimated that inflation will reach 3.1% at year-end, approaching the BCRP’s target range. The BCRP estimates that inflation will return to the target range as of April 2024. In a recent conference, Minister of Finance Alex Contreras considered that if inflation returns to the target range, it is likely that monetary policy will adopt a more expansionary stance. 12-month inflation expectations fell from 3.33% to 3.15% in the latest survey, so if the rate is cut by an additional 25bps this Thursday, the real interest rate would go from 3.7% to 3.6%, still well above the neutral level of 2%. Our 2024 forecast considers a cut of 200bps in the key rate to 4.75%.

—Mario Guerrero

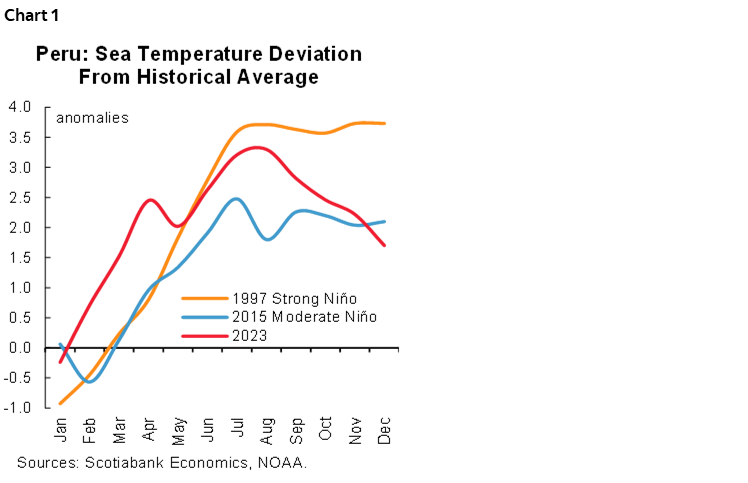

PERU: IT’S RAINING! YAY!!!

One may wonder why we are happy that it’s raining. Aren’t rains a sign of the arrival of El Niño? It’s all about location. El Niño brings with it torrential rains along the northern and central coast, but produces drought in the southern Andes. In fact, the type of drought that we had been experiencing since April this year. But the torrential rains so far this December have been taking place precisely in the heretofore drought-ridden southern Andes. And these rains are indicative of normal weather, not El Niño.

So, what happened to El Niño? Sea temperatures, as registered by NOAA (the U.S. National Oceanic and Atmospheric Administration) have fallen precipitously (if you can excuse the pun) since September, with the decline accelerating in early December. This is especially true for Peru’s coastal sea where temperatures are now just inside the normal historical range for non-Niño years (typically defined as 1.5 degrees above or below the historical norm). This is the first time that this has happened since March (chart 1).

El Niño’s temper tantrum during most of 2023 appears to be transitioning into a state of docility. Let’s hope this lasts. The persistent decline in sea temperatures and the rains in the southern highlands, effectively interrupting the drought there, are two potent signs that it may.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.